Improve Your Credit Score Fast

Three years ago, my credit score was 583. I know that because I checked it one evening after being denied for an apartment rental, and the number hit me like a punch to the stomach. The landlord looked at me with that polite but firm expression that said “sorry, but no,” and I spent the drive home wondering how three digits could have so much power over my life.

A 583 credit score meant I couldn’t rent the apartment I wanted. It meant sky-high interest rates on everything. It meant higher insurance premiums. It meant my cell phone provider wanted a $400 deposit for a basic plan. It meant I was paying a hidden tax on being financially behind — a tax that made everything in my life more expensive.

Today, my credit score is 761. I didn’t hire a credit repair company. I didn’t use any weird loopholes. I followed seven specific steps consistently, and my score climbed steadily over time. Some of these steps gave me a noticeable jump within 30 days. Others took a few months. But together, they transformed my credit profile.

This guide walks you through the same seven steps. Whether your score is 500 or 680, these strategies will move the needle. Some will show results in weeks. Others build the foundation for a score that keeps climbing for years.

Understanding Your Credit Score: The Basics You Need to Know

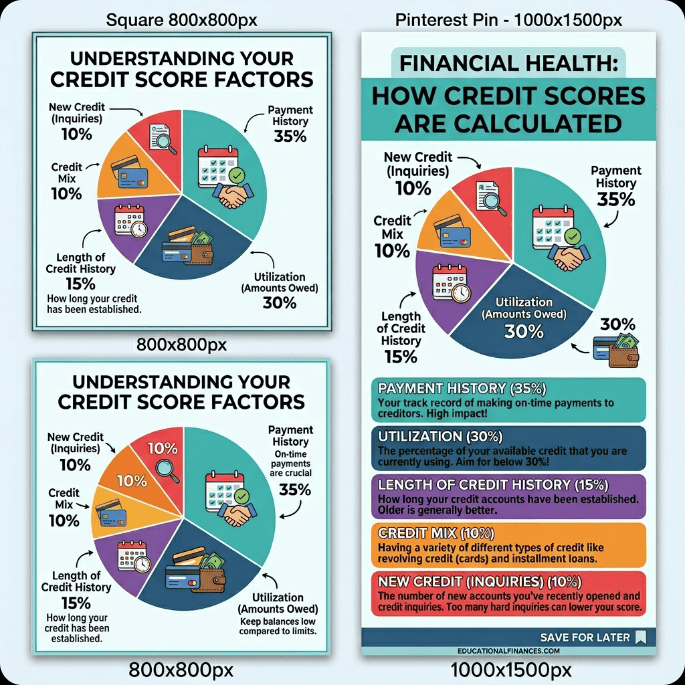

Before we fix your score, you need to understand what you’re actually fixing. Your credit score isn’t random — it’s calculated from five specific factors, and each one has a different weight.

Payment History — 35% of your score. This is the single biggest factor. Do you pay your bills on time? Every time? Late payments, missed payments, and collections destroy your score faster than anything else.

Credit Utilization — 30% of your score. This measures how much of your available credit you’re actually using. If you have a credit card with a $5,000 limit and you’re carrying a $4,000 balance, your utilization is 80%. That’s terrible. Lenders see high utilization as a sign that you’re financially stretched.

Length of Credit History — 15% of your score. How long have your accounts been open? Older accounts boost your score because they show a longer track record of managing credit.

Credit Mix — 10% of your score. Lenders like to see that you can manage different types of credit — credit cards (revolving credit), car loans (installment credit), and mortgages. Having only one type is fine, but a mix helps.

New Credit Inquiries — 10% of your score. Every time you apply for new credit, a “hard inquiry” hits your report. One or two inquiries are fine. Five or six in a short period signal desperation to lenders and ding your score.

Understanding these five factors tells you exactly where to focus your energy. Steps 1 through 3 below target the two biggest factors (payment history and utilization), which together control 65% of your score. That’s where the fastest gains happen.

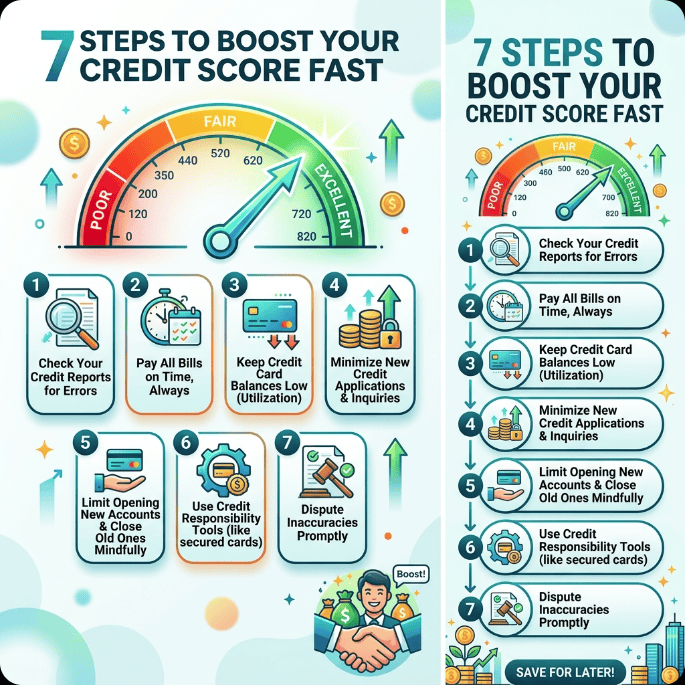

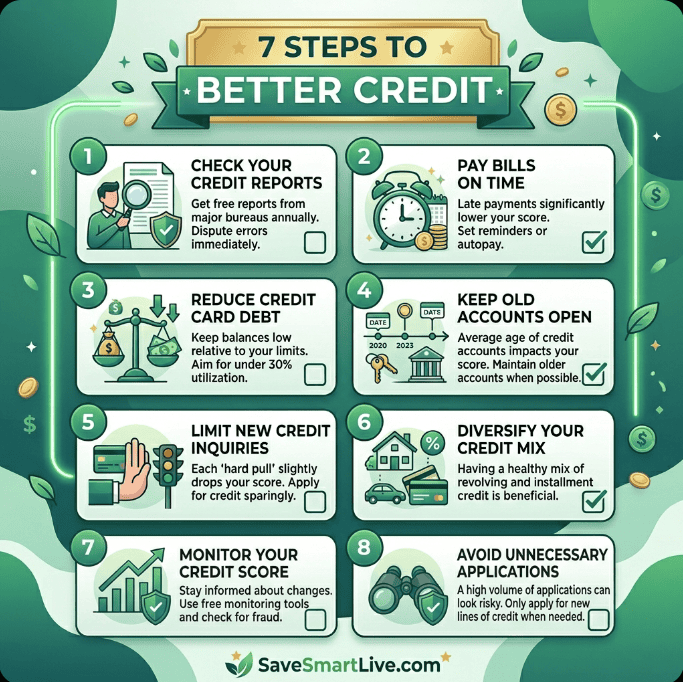

Step 1: Check Your Credit Reports for Errors (Quick Win)

This is the very first thing you should do because it costs nothing, takes 15 minutes, and could give you an immediate score boost.

One in five Americans has an error on their credit report. That’s 20% of people walking around with a score that’s lower than it should be because of mistakes they didn’t make.

Common credit report errors include accounts that don’t belong to you (mixed up with someone who has a similar name), paid debts still showing as unpaid, incorrect balances or credit limits, duplicate accounts, and late payments that were actually paid on time.

Here’s how to check. Go to AnnualCreditReport.com — this is the only official site authorized by federal law to provide free credit reports. You get one free report per year from each of the three major bureaus: Equifax, Experian, and TransUnion.

Pull all three reports. They may contain different information because not all creditors report to all three bureaus. Go through each report line by line and flag anything that looks wrong.

If you find errors, dispute them directly with the bureau that has the incorrect information. You can do this online at each bureau’s website. The bureau has 30 days to investigate and respond. If the error is confirmed, it gets removed, and your score adjusts — sometimes by 20 to 50 points or more depending on the severity of the error.

Pro Tip: Set a calendar reminder to check your credit reports every four months. Check Equifax in January, Experian in May, and TransUnion in September. This way you’re monitoring your credit for free year-round without paying for a monitoring service.

Improve Your Credit Score Fast

Step 2: Pay Every Bill On Time, Every Time (The Most Important Step)

Payment history is 35% of your score. There is nothing — absolutely nothing — that helps your credit more than a consistent record of on-time payments. And there’s nothing that hurts it more than a missed payment.

A single payment that’s 30 days late can drop your score by 60 to 110 points. The higher your score was before the miss, the harder it falls. A person with a 780 score who misses one payment might see their score drop to 670. It’s brutal, and the late payment stays on your report for seven years.

Here’s how to make sure you never miss a payment.

Set up autopay for at least the minimum payment on every account. This is your safety net. Even if you forget, even if you’re sick, even if you’re on vacation, the minimum payment goes out automatically and protects your credit. You can always pay more manually, but the autopay ensures you never miss.

Create payment reminders. Use your phone’s calendar to set reminders three days before each due date. This gives you time to make sure the money is in your account before autopay triggers.

If you’re already behind, get current as fast as possible. If you have past-due accounts, bringing them current is the single most impactful thing you can do. A currently past-due account hurts your score every single month. The moment you catch up, the bleeding stops.

Negotiate with creditors if you can’t pay. If you’re struggling, call your creditors before you miss a payment. Many will offer hardship programs, temporary payment reductions, or extended due dates. A creditor who agrees to a modified payment plan won’t report you as late. But a creditor you ignore will.

Improve Your Credit Score Fast

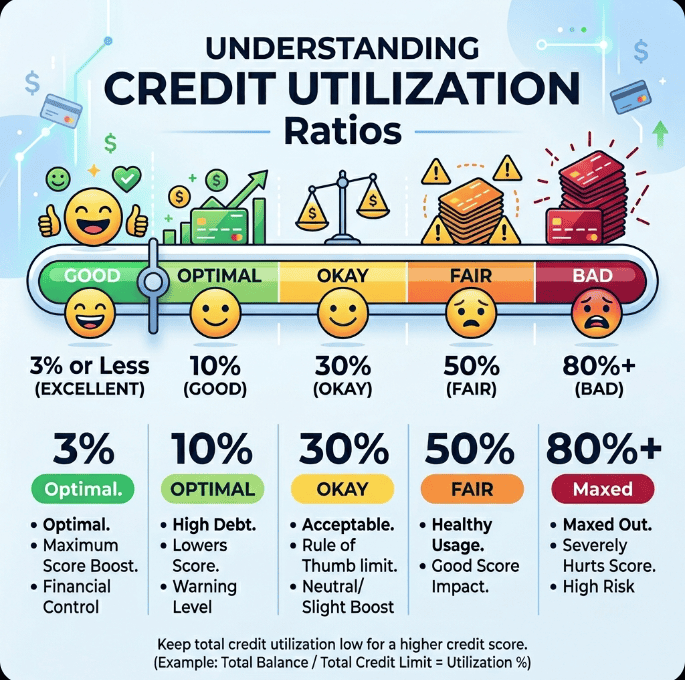

Step 3: Lower Your Credit Utilization Below 30% (Fast Results)

Credit utilization — how much of your available credit you’re using — is 30% of your score and one of the fastest factors to improve. Unlike payment history, which takes months of consistent behavior to build, utilization is recalculated every billing cycle. Lower your balances this month, and your score can improve next month.

The magic number is 30%. Lenders want to see that you’re using less than 30% of your available credit. Below 10% is even better. And 1% to 3% is ideal.

Here’s how to think about it. If you have a credit card with a $3,000 limit, try to keep your statement balance below $900 (30%). Below $300 (10%) is better. Below $90 (3%) is ideal.

If your utilization is currently high, here are the fastest ways to bring it down.

Pay down balances aggressively. This is obvious but worth stating. Every dollar you pay toward your credit card balance lowers your utilization. Focus extra payments on the card with the highest utilization percentage first.

Make multiple payments per month. Instead of one big payment when the bill is due, make smaller payments throughout the month. This keeps your running balance lower, which means a lower utilization is reported to the bureaus.

Ask for a credit limit increase. Call your credit card company and ask for a higher limit. If you have a $3,000 limit and they raise it to $5,000, your utilization drops instantly — even if your balance stays the same. A $1,500 balance on a $3,000 limit is 50% utilization. The same balance on a $5,000 limit is only 30%.

Most credit card companies will increase your limit if you’ve been a customer for at least 6 months and have a decent payment history. Many allow you to request an increase online without even calling.

Don’t close old credit cards. When you close a credit card, you lose that card’s credit limit from your total available credit. This increases your overall utilization even if you haven’t spent more money. Keep old cards open, even if you rarely use them. Charge a small purchase every few months to keep them active.

Pro Tip: Time your credit card payments strategically. Your credit card company reports your balance to the bureaus on a specific date each month (usually your statement closing date, not your due date). If you pay your balance down before the statement closes, a lower balance gets reported. Call your card company to find out your statement closing date.

Step 4: Become an Authorized User on Someone Else’s Card

This is one of the fastest and least-known ways to boost a thin or damaged credit profile, and it’s completely legitimate.

When someone adds you as an authorized user on their credit card, that card’s entire history gets added to your credit report. If they’ve had the card for 10 years with perfect payments and a low balance, all of that positive history now shows up on your report too.

You don’t even have to use the card. In fact, many people who use this strategy never touch the card at all. The person adding you doesn’t even have to give you the physical card. The credit benefit comes from the account appearing on your report, not from actually spending on it.

The best person to ask is a parent, spouse, sibling, or trusted family member who has a credit card with a long history of on-time payments and low utilization.

Important caveats. If the primary cardholder misses payments or carries a high balance, that negative information will hurt your score too. Only get added to accounts with excellent history. Also, not all credit card companies report authorized user activity to all three bureaus, so check before relying on this strategy.

Expected impact: 20 to 50+ point increase within 1-2 billing cycles.

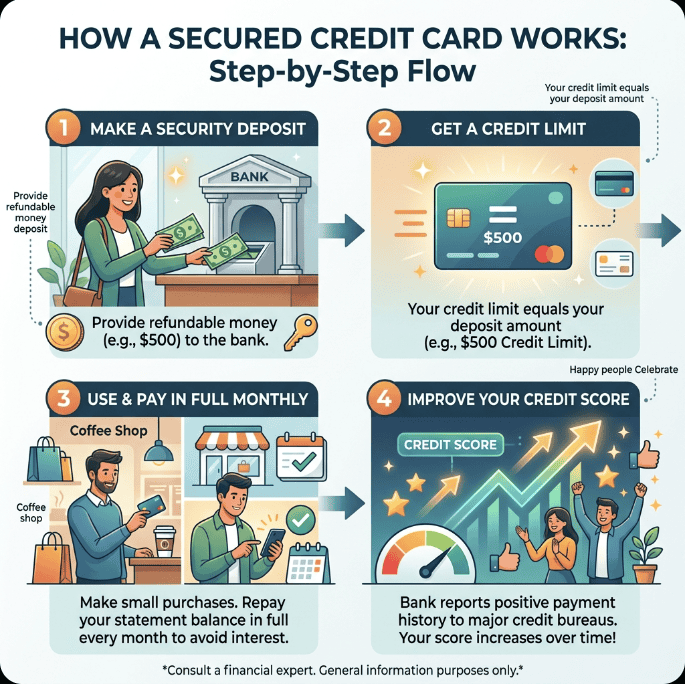

Step 5: Use a Secured Credit Card to Build Fresh History

If your credit is severely damaged or you have no credit history at all, a secured credit card is your best starting tool.

A secured credit card works like a regular credit card, but you put down a cash deposit (usually $200 to $500) that serves as your credit limit. If you deposit $300, your credit limit is $300. This deposit protects the card issuer, which is why they’re willing to give cards to people with bad or no credit.

Use the card for one or two small purchases each month — a tank of gas, a streaming subscription, or your phone bill. Pay the statement balance in full every month, on time. Never carry a balance. Never use more than 30% of the limit.

After 6 to 12 months of responsible use, most secured card issuers will upgrade you to a regular unsecured card and refund your deposit. More importantly, those 6 to 12 months of perfect payment history are now on your credit report, steadily building your score.

Good secured card options include the Discover it Secured Card (earns cash back rewards), the Capital One Platinum Secured Card (possible automatic upgrade to unsecured), and the OpenSky Secured Visa (no credit check to apply).

Expected impact: Steady improvement of 30 to 80 points over 6-12 months of responsible use.

Step 6: Keep Old Accounts Open (Even if You Don’t Use Them)

Your length of credit history accounts for 15% of your score. The longer your average account age, the better your score. This is why closing old credit cards — even ones you no longer use — can actually hurt your score.

When you close your oldest credit card, two negative things happen simultaneously. First, your average account age drops, which directly reduces your score. Second, you lose that card’s credit limit from your total available credit, which increases your overall utilization.

Instead of closing old cards, keep them open and use them occasionally. Charge a small recurring purchase — like a streaming subscription or a monthly bill — to each old card. Set up autopay for the full balance. This keeps the card active (preventing the issuer from closing it for inactivity) while building a longer payment history with zero effort.

If you’re worried about annual fees on a card you no longer use, call the issuer and ask to downgrade to a no-annual-fee version of the same card. This preserves your account age and credit limit while eliminating the fee.

Step 7: Limit Hard Inquiries on Your Credit Report

Every time you apply for a credit card, loan, mortgage, or other credit product, the lender pulls your credit report. This creates a “hard inquiry” that temporarily dings your score by 5 to 10 points.

One or two hard inquiries per year are normal and won’t significantly impact your score. But multiple applications in a short period — applying for five credit cards in two months, for example — signal desperation to lenders and can cost you 25 to 50 points combined.

Here’s how to manage inquiries wisely.

Only apply for credit you actually need. Don’t apply for store credit cards just to get a 10% discount. That inquiry and new account can cost your credit score more than the one-time savings.

Rate-shop within a focused window. If you’re shopping for a mortgage, auto loan, or student loan, multiple inquiries for the same type of credit within a 14 to 45 day window (depending on the scoring model) count as a single inquiry. This means you can get quotes from five mortgage lenders without five separate dings on your score — as long as you do it within a few weeks.

Check whether a lender does a soft or hard pull. Prequalification checks and many credit monitoring tools use “soft inquiries” that don’t affect your score at all. Ask before you apply, and use prequalification tools whenever possible to check your odds before committing to a hard inquiry.

Be patient. Hard inquiries fall off your credit report after two years and stop affecting your score after about 12 months. If you’ve had several recent inquiries, simply waiting and not applying for new credit will naturally heal this factor.

Pro Tip: If you’re rebuilding your credit, resist the urge to apply for everything at once. Get one secured card, use it responsibly for 6-12 months, and let your score build naturally before applying for additional credit products.

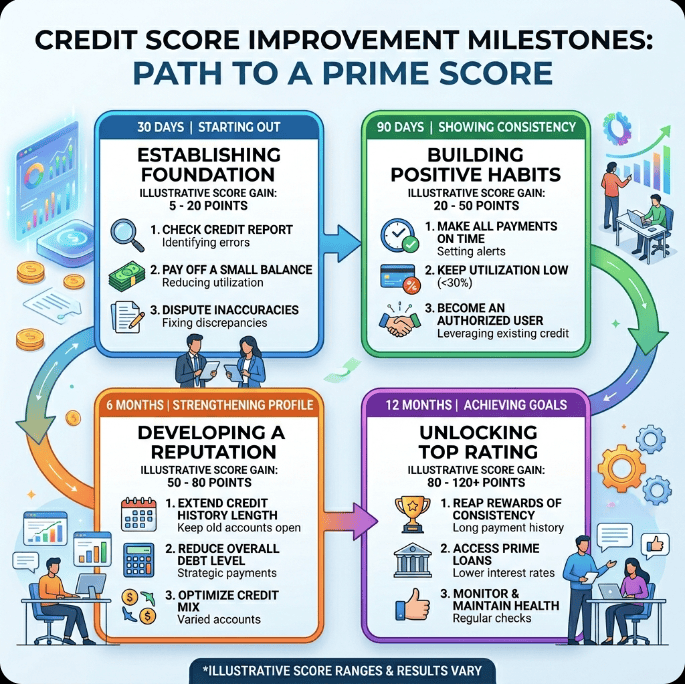

Realistic Credit Score Improvement Timeline

Let me set honest expectations about how quickly you can see results.

Within 30 days: If you dispute and remove errors from your credit report, or if you pay down high credit card balances significantly, you can see a 20 to 50 point jump within one billing cycle.

Within 60 to 90 days: Consistent on-time payments, lowered utilization, and becoming an authorized user can produce a 30 to 80 point improvement over 2-3 months.

Within 6 months: Following all seven steps consistently, most people see a 50 to 150 point improvement. A 580 can become a 680. A 650 can become a 750.

Within 12 months: With a full year of on-time payments, low utilization, and responsible credit management, scores typically improve 100 to 200 points from their starting point. This is where real financial doors start opening — better interest rates, easier approvals, lower insurance premiums.

The important thing to understand is that credit repair is not instant. Anyone who promises to “fix your credit overnight” or “boost your score 200 points in a week” is either lying or doing something illegal. Real credit improvement takes consistent action over months. But it works, and the financial benefits last for decades.

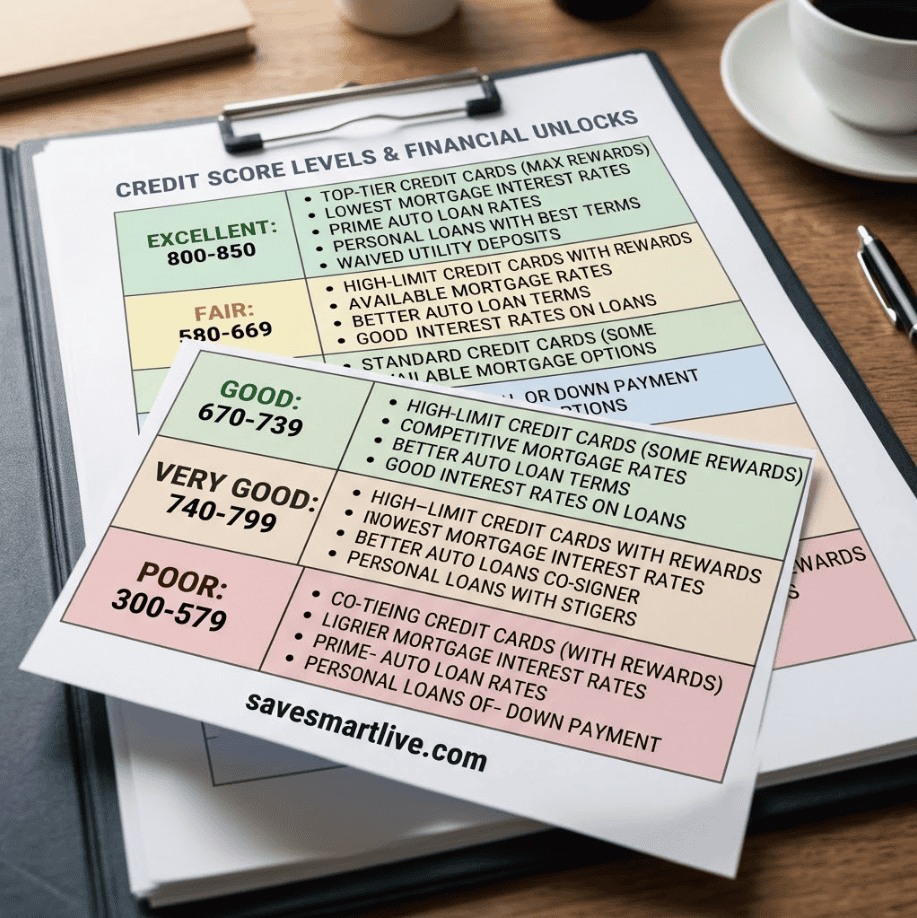

What Your Credit Score Unlocks at Different Levels

Understanding what your score means in practical terms can be incredibly motivating. Here’s what different score ranges typically get you.

300-579 (Poor): Very difficult to get approved for most credit products. If approved, interest rates are extremely high. Landlords and utility companies require large deposits. Some employers check credit for certain positions.

580-669 (Fair): Approved for some credit products but with above-average interest rates. Subprime auto loans, higher insurance premiums, and limited credit card options.

670-739 (Good): This is where life gets significantly easier. Approved for most credit cards, competitive auto loan rates, reasonable mortgage rates, and most rental applications. This is the threshold to aim for if you’re rebuilding.

740-799 (Very Good): Excellent interest rates on everything. The best credit card rewards programs. Premium rental approvals. Lower insurance premiums. You’re in the top tier of borrowers.

800-850 (Exceptional): The absolute best terms available. You’ll qualify for the lowest mortgage rates, the highest credit limits, and the best financial products. The practical difference between 800 and 850 is minimal — both get you the best of everything.

Frequently Asked Questions

How long does it take to improve a credit score?

Significant improvement typically takes 3 to 6 months of consistent action. Quick wins (error disputes, paying down balances) can show results within 30 days. Building a strong credit history takes 12 months or more of on-time payments.

Does checking my own credit score lower it?

No. Checking your own score is a “soft inquiry” and has zero effect on your credit. Check it as often as you want. Free options include Credit Karma, Credit Sesame, and your bank or credit card app.

Will paying off collections raise my score?

It depends on the scoring model. Under newer FICO models (FICO 9 and 10) and VantageScore, paid collections are either removed or given less weight. Under older models, a paid collection still shows as a negative mark. Either way, paying off collections is the right move because many lenders manually consider whether collections are paid or unpaid.

Should I close credit cards I don’t use?

Generally, no. Closing cards reduces your available credit (hurting utilization) and can lower your average account age. Keep old cards open with small occasional purchases and autopay.

How much can my score improve in 6 months?

With consistent action on all seven steps, a 50 to 150 point improvement in 6 months is realistic. The biggest gains come from paying down high utilization and establishing a pattern of on-time payments.

Is it worth paying for credit repair services?

Usually no. Everything a credit repair company does — disputing errors, negotiating with creditors, advising you on strategy — you can do yourself for free. Save that $50 to $100 per month and put it toward paying down debt instead.

What’s the fastest way to build credit from zero?

Open a secured credit card, use it for one or two small purchases per month, and pay the full balance every month. Ask a family member to add you as an authorized user on their longest-held, best-managed credit card. Within 6 to 12 months, you’ll have a solid foundation.

Your Credit Score Is a Tool, Not a Report Card

I want to leave you with a mindset shift that helped me more than any single tip in this guide.

Your credit score is not a measure of your worth as a person. It’s not a grade on your financial intelligence. It’s not a permanent judgment about your past mistakes.

It’s a tool. A tool that, when maintained properly, gives you access to better opportunities — lower interest rates, better housing options, cheaper insurance, and more financial flexibility. A tool that you have the power to improve, starting right now, regardless of where the number sits today.

I went from 583 to 761. Not because I’m special or particularly disciplined. But because I followed these seven steps consistently, month after month, until the score reflected the changes I’d made.

You can do the same thing. The steps are simple. The results are proven. And the impact on your financial life is genuinely transformational.

Start with Step 1. Pull your credit reports tonight. Everything else flows from there.

Found this guide valuable? Save it to Pinterest and share it with someone working on their credit. For more money tips and financial strategies, visit SaveSmartLive.com.

Related articles:

- How to Create a Monthly Budget That Actually Works

- Debt Snowball vs Debt Avalanche: Which Is Better?

- How to Start an Emergency Fund From Zero

- Beginner Guide to Investing: Start With Just $100

Read More : 20 Realistic Side Hustles That Pay $500 or More Per Month in 2026