how to save $5000 in a year

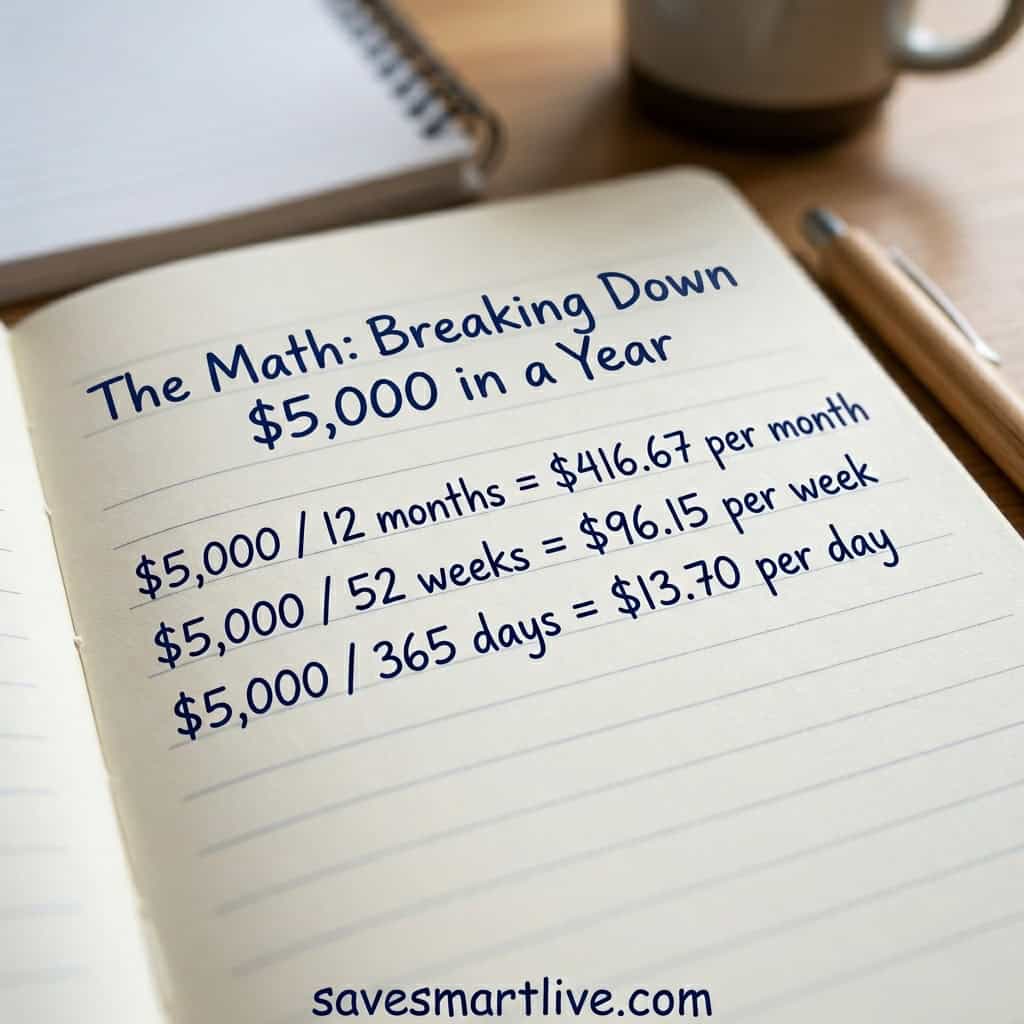

The Math: Breaking Down $5,000 in a Year

Big savings goals feel overwhelming until you break them into small chunks. Once you see the daily and weekly numbers, the goal stops looking scary.

Here is the simple math:

- $5,000 per year

- $416.67 per month

- $96.15 per week

- $13.70 per day

That daily number is powerful. Almost everyone wastes $14 a day without realizing it. Skip one fancy coffee, one impulse Amazon order, or one delivery fee — and you are already there.

You do not have to save the same amount every day. Some weeks you will save more. Some months will be tight. The goal is the yearly total. Stay focused on the big picture.

Here is another way to look at it. If you save just $50 a week from your paycheck, you hit $2,600 in 12 months. Add a small tax refund, one or two side gigs, and a few cut subscriptions — and $5,000 becomes very real.

The math is not magic. It is just consistency. Keep showing up, keep choosing the smart option, and the money adds up faster than you think.

Step 1: Audit Your Current Spending

Before you can save 5000 dollars year after year, you need to know exactly where your money goes today. Most people have no clue how much they spend on food, subscriptions, or random extras each month. That is where the leaks happen.

Pull up your bank and credit card statements from the last 60 days. Sort every transaction into categories:

- Housing (rent, utilities)

- Transportation (gas, insurance, parking)

- Food (groceries, eating out, coffee)

- Subscriptions (streaming, apps, gym)

- Shopping (clothes, gadgets, gifts)

- Entertainment (events, hobbies)

- Other (fees, charges, surprise expenses)

Add it all up. You will probably be shocked. Most people overspend in two or three obvious categories.

This audit is the most important step. You cannot fix what you cannot see.

Use a free app like Mint, Rocket Money, or just a simple Google Sheet. The tool does not matter. The honesty does.

Once you know your spending patterns, you can pinpoint where to cut. Often, just trimming the top three leak categories saves a few hundred dollars a month — without changing your lifestyle much.

Step 2: Set Up a Dedicated Savings Account

If your savings sits in your regular checking account, you will spend it. Period. Out of sight, out of mind is real — but the opposite is even more true. In sight, easy to swipe.

Open a separate high-yield savings account (HYSA). These accounts pay 10x to 20x more interest than regular bank accounts. Top options include Ally, Discover, Marcus, SoFi, and Capital One 360.

Why this matters:

- Your money earns real interest while it sits

- It is harder to spend on impulse

- You feel motivated watching the balance grow

- It does not need to be your main bank

A high-yield savings account can earn you an extra $100 to $200 per year in interest on your $5,000. That is free money for doing absolutely nothing.

Set up the account this week. It takes about 10 minutes online.

Step 3: Automate Your Savings (Pay Yourself First)

This is the most important habit for anyone trying to save 5000 dollars year over year. Automation removes willpower from the equation. You do not have to remember. You do not have to feel like saving. The money just moves on its own.

Set up an automatic transfer of $96 every Friday — or $200 every payday — from checking into your high-yield savings account. Schedule it for the same day your paycheck hits. That way, you save before you can spend.

This is what financial experts call “paying yourself first.” Most people do the opposite. They pay bills, spend on wants, and try to save what is left. Usually, nothing is left.

When you automate, savings becomes a fixed bill. Just like rent or electricity. You stop thinking about it.

Pro tip: Start small if needed. Even $25 a week is better than nothing. As you cut other costs, raise your transfer amount. Within a few months, you will likely hit $96 per week without feeling the pinch.

Automation alone gets most people 70% of the way to their savings goal. The other 30% is everything else in this guide.

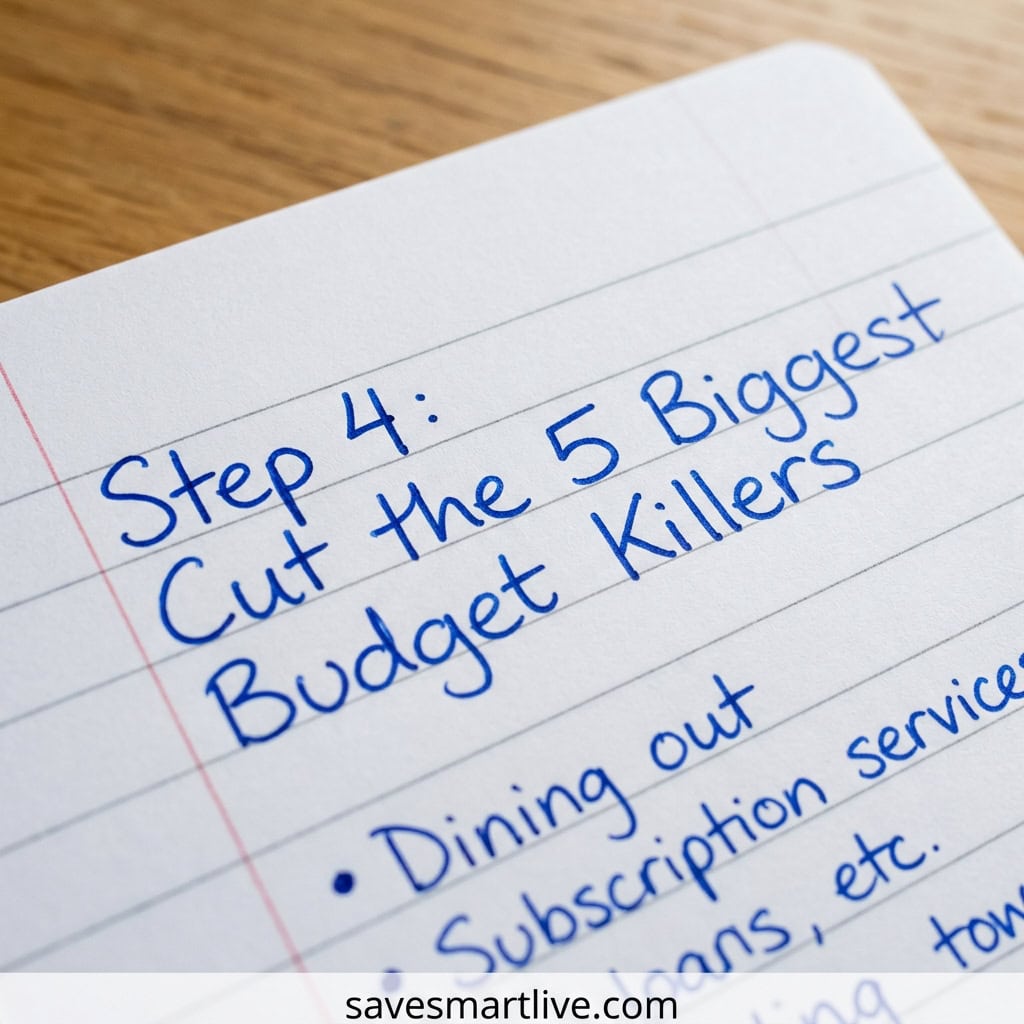

Step 4: Cut the 5 Biggest Budget Killers

Now we get into the fun part — finding extra money in your existing budget. Most people have hundreds of dollars hiding in plain sight every month. These are the five biggest culprits.

1. Forgotten Subscriptions

Streaming services, app trials that turned into auto-charges, premium memberships you never use. The average American spends over $200 a month on subscriptions, often without realizing it.

Action: Cancel any subscription you have not used in 30 days. Save: $50 to $100 a month.

2. Eating Out and Takeout

A $12 lunch four times a week is around $200 a month. Add coffee, snacks, and dinner deliveries — and it easily reaches $400 or more each month.

Action: Cook at home five nights a week. Pack lunch three days a week. Save: $200 to $300 a month.

3. Brand-Name Groceries

Generic and store-brand products are usually 25% to 40% cheaper than name brands. The quality is often identical because they come from the same factories.

Action: Switch to store-brand staples like pasta, cereal, paper goods, and frozen foods. Save: $50 to $100 a month.

4. Impulse Shopping

That midnight Amazon order. The “treat yourself” purchase you forget about by next week. Impulse buying drains $100 to $300 a month for many people.

Action: Use the 24-hour rule. If you want something non-essential, wait 24 hours. Most of the time, the urge passes. Save: $100 to $200 a month.

5. High-Interest Debt

Credit card interest at 20% APR or higher can kill any savings progress. If you carry a balance, every dollar saved is being eaten by interest charges.

Action: Pay more than the minimum each month. Or move debt to a 0% balance transfer card. Save: $50 to $200 a month in interest charges.

Add up the savings from just three of these areas, and you can easily free up $300 to $500 a month. That alone could fund your entire $5,000 yearly goal.

The key is not to do all five perfectly. Start with one or two. Stack wins. Build momentum.

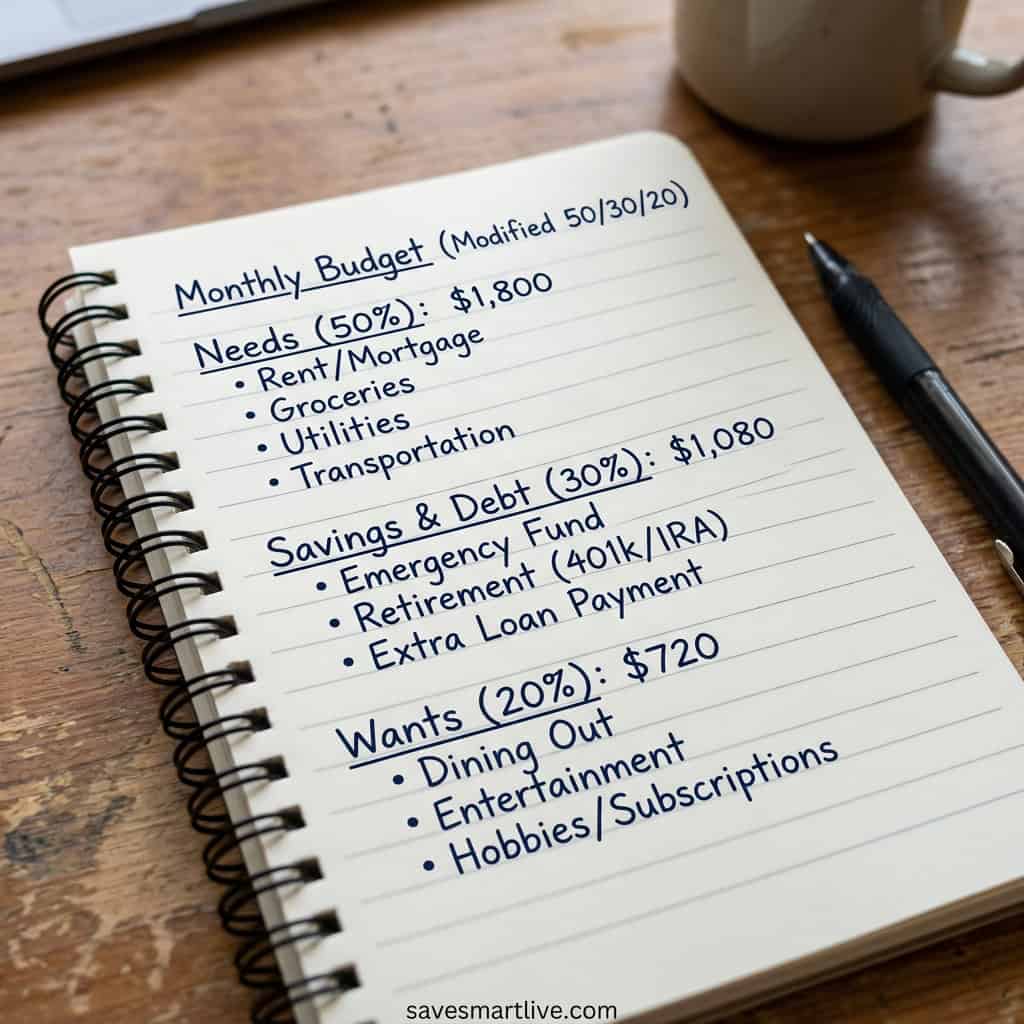

Step 5: Use the 50/30/20 Rule (Modified)

The classic 50/30/20 rule splits your after-tax income three ways:

- 50% on needs (housing, food, transportation)

- 30% on wants (entertainment, shopping)

- 20% on savings and debt repayment

For most average earners, the original rule works — but it can be tweaked for faster savings.

Try the 50/20/30 version (note the swap):

- 50% needs

- 20% wants

- 30% savings and debt

By cutting wants slightly and pushing more into savings, you can hit $5,000 in a year much faster — even on a modest salary.

Quick example: If you take home $3,500 a month, 30% is $1,050. That is way more than the $416 monthly target needed to save 5000 dollars year over year. Even hitting half that pace gets you there comfortably.

This rule gives you a simple framework. You do not need to track every penny. You just need to keep your spending within these rough buckets.

If 30% feels like too much for savings right now, start with 20% and work up. Progress matters more than perfection.

Step 6: Boost Your Income with Side Hustles

Cutting expenses has limits. You can only trim so much before life feels miserable. The other side of the equation is earning more.

Even an extra $200 to $400 a month from a side hustle can completely change your savings trajectory. Combine that with smart spending, and you can save 5000 dollars year well ahead of schedule.

Popular side hustles that work for average earners:

Freelancing online. Use platforms like Fiverr, Upwork, or LinkedIn to offer skills you already have — writing, design, virtual assistance, video editing.

Driving or delivering. Uber, DoorDash, Instacart, and Amazon Flex can earn $15 to $25 an hour with flexible hours.

Selling things you do not use. Old clothes on Poshmark or Mercari. Old electronics on Swappa or eBay. Furniture on Facebook Marketplace.

Tutoring. Online tutoring sites pay $15 to $40 an hour. If you are good with kids or a school subject, this is easy money.

Print on demand. Sell custom t-shirts, mugs, and posters on platforms like Redbubble or Printify with zero inventory.

Pet sitting or dog walking. Apps like Rover let you earn while spending time with animals.

You do not have to do this forever. Even three to six months of consistent side income can fully fund your savings goal.

Pro tip: Send your side hustle income directly into your high-yield savings account. Treat it like bonus money. Out of sight, growing fast.

how to save $5000 in a year

Step 7: Try Money-Saving Challenges

Savings challenges turn a boring goal into a fun game. They keep you motivated when willpower starts to slip.

Here are three challenges that thousands of people use to save 5000 dollars year after year:

The 52-week challenge. Save $1 in week 1, $2 in week 2, and so on. By week 52, you save $52. Total: $1,378. You can double the amounts to hit closer to $2,756. Pair it with other savings habits to reach $5,000.

The no-spend month. Pick one month a year where you only spend on essentials — rent, food, gas, bills. No shopping, no eating out, no extras. Most people save $400 to $800 in a single no-spend month.

The $5 bill challenge. Every time you get a $5 bill in change, stash it in a jar. Sounds tiny, but most people end up saving $300 to $700 a year this way.

These challenges work because they trick your brain. Instead of feeling deprived, you feel like you are winning a game. Pick one. Try it. The momentum will surprise you.

Smart Tips That Multiply Your Savings

A few extra hacks can supercharge your $5,000 savings goal.

Use cashback apps. Rakuten, Ibotta, and Upside give you money back on stuff you already buy.

Round-up apps. Apps like Acorns round up every purchase and save the difference. It adds up to hundreds a year automatically.

Stack tax refunds and bonuses. Drop your full tax refund into savings. Same with work bonuses or birthday cash. These windfalls speed up your goal fast.

Negotiate bills. Call your internet, phone, and insurance providers once a year. Ask for a lower rate. Most companies offer one to keep you.

Buy used. Cars, furniture, electronics — buying gently used can save 30% to 60%.

Pack your lunch. A simple homemade lunch costs around $2. A bought lunch costs $12. Five days a week equals $50 saved every single week.

These small wins stack up. They turn an ambitious goal into an inevitable result.

Common Mistakes That Kill Your Progress

Most people who fail to save $5,000 make the same mistakes. Avoid these traps.

Trying to do everything at once. You do not need to cut every cost on day one. Start with one or two changes. Build from there.

Keeping savings in your checking account. Spending temptation is too high. Move it to a separate high-yield account fast.

Not tracking progress. Without checking your numbers monthly, you have no idea if you are on pace. A quick review keeps you accountable.

Quitting after a setback. One bad month does not ruin a year. Just adjust and move forward.

Comparing to others. Someone else’s savings journey is irrelevant. Focus only on your own progress.

Forgetting to celebrate. Hit $1,000? Celebrate. Hit $2,500? Celebrate. Reward yourself with non-spending wins like a free hike or a movie night at home.

Avoid these traps and you stay on track all year.

How to Stay Motivated for 12 Months

Saving for an entire year is a marathon. Motivation will go up and down. That is normal. Here is how to keep going when it gets hard.

Visualize your goal. Picture exactly what $5,000 will mean to your life. Write it down. Read it weekly.

Track your progress visually. A printed savings chart on your fridge or a thermometer-style tracker keeps you motivated.

Find an accountability partner. A friend or family member working toward the same goal makes the journey easier.

Follow personal finance content. YouTube, Pinterest, and Reddit communities like r/personalfinance keep your mindset sharp.

Reward small wins. Every $500 saved deserves a celebration. Just make sure the reward is free or low-cost.

Remind yourself why you started. When motivation dips, reread your “why.” That emotional anchor is the most powerful tool you have.

Read More: 20 Realistic Side Hustles That Pay $500 or More Per Month in 2026