The 50/30/20 Budget Rule

I remember the first time I sat down to create a budget. I had a spreadsheet open, twenty-something expense categories, and absolutely no idea how much to allocate to each one. Should groceries be $300 or $500? How much is “normal” for entertainment? What percentage of my income should go toward rent?

I spent two hours overthinking it, got frustrated, closed the spreadsheet, and didn’t try again for six months.

If that sounds familiar, the 50/30/20 budget rule might just change your financial life. It changed mine. Instead of getting buried in dozens of categories and tiny amounts, this method splits your money into just three simple buckets. That’s it. Three buckets. Even on your worst, most exhausted, can’t-think-straight day, you can manage three buckets.

This guide will walk you through exactly how the 50/30/20 rule works, show you real-life examples at different income levels, help you figure out what counts as a “need” versus a “want” (it’s trickier than you think), and give you a step-by-step plan to start using this method today.

What Is the 50/30/20 Budget Rule?

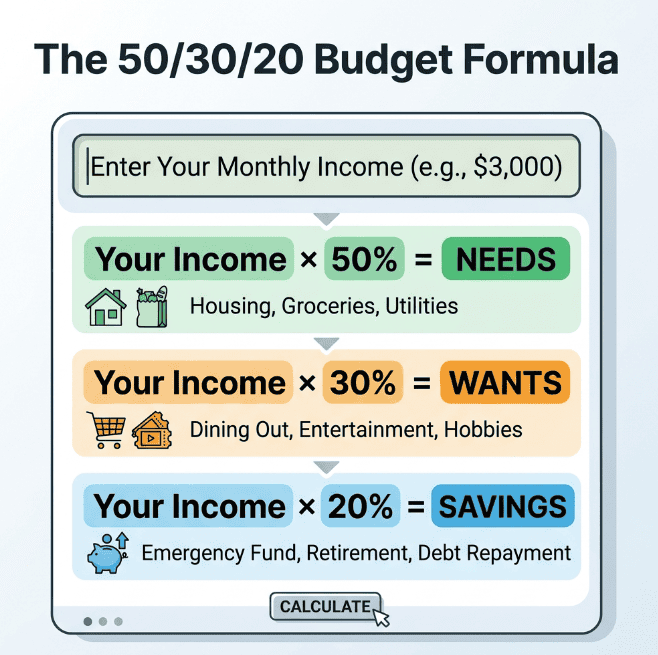

The 50/30/20 rule is a budgeting framework that divides your after-tax income into three categories.

50% goes to Needs — the things you absolutely must pay for to survive and function. Think housing, groceries, utilities, insurance, minimum debt payments, and transportation to work.

30% goes to Wants — the things that make life enjoyable but that you could technically live without. This includes dining out, streaming services, hobbies, new clothes beyond the basics, vacations, and that gym membership.

20% goes to Savings and Debt Repayment — money that goes toward building your future. Emergency fund contributions, retirement savings, investment accounts, and extra payments on any debt you’re carrying.

The beauty of this system is in its simplicity. You don’t need to track whether you spent $47.82 on coffee this month or $52.13 on household supplies. You just need to keep three numbers in check.

This rule was popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their book “All Your Worth: The Ultimate Lifetime Money Plan.” Since then, it has become one of the most widely recommended budgeting methods by financial advisors, personal finance bloggers, and money coaches around the world.

The 50/30/20 Budget Rule

How to Calculate Your 50/30/20 Budget

Let’s make this concrete with actual numbers. The first thing you need is your monthly after-tax income. This is your take-home pay — the amount that actually lands in your bank account after federal taxes, state taxes, Social Security, and Medicare are deducted.

If you’re salaried, check your most recent pay stub. Look for “net pay.” If you get paid biweekly, multiply that number by 2 (or multiply by 26 and divide by 12 for a more accurate monthly figure). If you’re hourly or freelance, use your average monthly take-home from the last three months.

Once you have your monthly after-tax income, the math is straightforward.

Monthly after-tax income × 0.50 = your Needs budget

Monthly after-tax income × 0.30 = your Wants budget

Monthly after-tax income × 0.20 = your Savings budget

That’s it. Three numbers. Your entire financial plan for the month.

The 50/30/20 Budget Rule

Real-Life Examples at Different Income Levels

Let’s see how this looks at four different income levels so you can find the one closest to yours.

Example 1: $3,000 Monthly Income

This is common for entry-level workers, recent graduates, and single-income households.

- Needs (50%) = $1,500. This covers rent ($800-$1,000), utilities ($100-$150), groceries ($250-$300), car insurance ($100), gas ($75), phone ($50), and minimum debt payments.

- Wants (30%) = $900. This covers dining out, entertainment, streaming services, clothing, personal care, hobbies, and small treats.

- Savings (20%) = $600. This goes toward your emergency fund, retirement contributions, and any extra debt payments.

At this income level, the needs bucket is tight. You’ll need to be intentional about housing costs — financial experts generally recommend keeping rent below 30% of your income. In this case, that’s $900 or less.

Example 2: $4,500 Monthly Income

This represents a mid-career professional or a dual-income household.

- Needs (50%) = $2,250. More breathing room for housing ($1,200-$1,400), higher grocery budgets, and better insurance coverage.

- Wants (30%) = $1,350. Enough for regular date nights, a gym membership, a couple of streaming services, and occasional weekend trips.

- Savings (20%) = $900. At this level, you can build an emergency fund relatively quickly and start making meaningful retirement contributions.

Example 3: $6,000 Monthly Income

This represents a well-paying professional job or a combined household income.

- Needs (50%) = $3,000. Comfortable housing, reliable car, full insurance coverage, quality groceries, and all bills comfortably covered.

- Wants (30%) = $1,800. Significant freedom for lifestyle choices — dining, travel, hobbies, and personal spending without guilt.

- Savings (20%) = $1,200. At $1,200 per month, you’re saving $14,400 per year. Invested wisely, this grows into real wealth over time.

Example 4: $8,000 Monthly Income

Higher income — but the percentages still apply.

- Needs (50%) = $4,000. Premium housing, newer vehicles, comprehensive coverage across all insurance types.

- Wants (30%) = $2,400. Vacations, restaurant experiences, premium gym memberships, and significant hobby budgets.

- Savings (20%) = $1,600. $19,200 per year toward financial independence. If you invest this consistently, you could build a million-dollar portfolio in approximately 25 years.

Pro Tip: As your income grows, consider shifting to 50/20/30 — moving more toward savings (30%) and reducing wants (20%). Higher earners who save 30% or more build wealth dramatically faster without sacrificing quality of life

Needs vs. Wants: The Tricky Part

This is where most people get stuck. The line between needs and wants isn’t always obvious, and being honest with yourself about which category something falls into is one of the hardest parts of budgeting.

Let me help you sort through the gray areas.

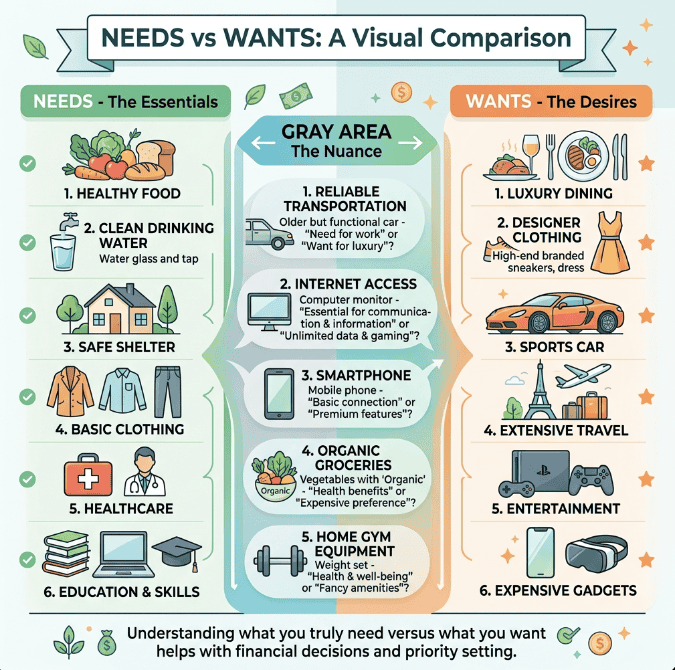

These Are Needs (the 50%)

Needs are expenses that, if you stopped paying them, would directly threaten your ability to live safely, stay healthy, keep your job, or fulfill legal obligations.

Housing — rent or mortgage, renter’s or homeowner’s insurance, property tax, basic maintenance.

Utilities — electricity, water, gas, heating. Not cable TV. Not premium internet packages. Basic service that keeps your home functional.

Groceries — food you buy to cook and eat at home. Not the fancy organic snacks. Not the $8 cold-pressed juice. Basic nutritious food to feed your household.

Transportation to work — car payment, gas, car insurance, public transit pass. The costs directly related to getting you to your job.

Insurance — health insurance, car insurance, and any insurance legally required or essential for your wellbeing.

Minimum debt payments — the minimum required payment on all debts. Not extra payments — those go in the 20% savings category.

Childcare — if you work and need childcare to do so, it’s a need.

Phone — a basic phone plan. Not the newest iPhone upgrade. Not the unlimited premium data plan with international features. A functional phone that keeps you connected and employable.

These Are Wants (the 30%)

Wants are anything that makes life more comfortable, enjoyable, or convenient but that you could technically live without. Be honest with yourself here — most of us have more wants disguised as needs than we’d like to admit.

Dining out and takeout — all of it, including “quick” lunches and coffee shop visits.

Entertainment — streaming services, concert tickets, movies, sporting events, books, video games, apps.

Gym membership — you can exercise for free. A gym is a convenience, not a requirement.

Shopping — clothing beyond basic essentials, home décor, gadgets, gifts.

Travel and vacations — every cent, including the “but it was such a good deal” flights.

Upgraded services — the premium phone plan, the faster internet, the fancy cable package, the higher-tier streaming subscription.

Personal care beyond basics — haircuts are arguably needs, but salon treatments, spa visits, and premium beauty products are wants.

The Gray Areas

Some expenses genuinely fall in between, and it’s okay to split them.

Internet is a need for most people who work from home or have kids in school. But the $100/month gigabit plan might be a want — the $50 basic plan would cover the need, and the extra $50 is a want.

A car might be a need if there’s no public transit where you live. But a $500/month payment on a new SUV when a reliable used car would cost $200/month means $200 is a need and $300 is a want.

Groceries can blur too. Basic rice, vegetables, chicken, and bread are needs. The artisan cheese, imported chocolate, and premium snack brands are wants.

The key is honesty. Nobody is grading your budget but you. The more honest you are about the distinction between needs and wants, the more effective this system becomes.

The 20% Savings Category: Where Real Progress Happens

The savings bucket is only 20% of your income, but it’s where the real transformation happens. This is the money that changes your future. Here’s how to prioritize it.

Priority 1: Build a Starter Emergency Fund ($1,000)

If you have nothing saved, the first $1,000 should go into a basic emergency fund. This isn’t for vacations or shopping — it’s for genuine emergencies like a car repair, an unexpected medical bill, or a broken appliance.

Having even $1,000 set aside prevents you from going into debt when life throws surprises. And trust me, life always throws surprises.

Priority 2: Pay Off High-Interest Debt

Once you have $1,000 saved, redirect the 20% toward destroying any high-interest debt — credit cards, personal loans, payday loans, anything with interest rates above 7% to 8%.

The math on this is brutal. If you’re carrying $5,000 in credit card debt at 22% interest and only making minimum payments, it takes over 14 years to pay off and costs you $7,700 in interest alone. That’s more than the original balance.

Using your 20% to aggressively attack this debt is one of the smartest financial moves you can make.

Priority 3: Build a Full Emergency Fund (3-6 Months)

After high-interest debt is gone, build your emergency fund to cover 3 to 6 months of essential expenses. This is your financial safety net — the cushion that lets you handle a job loss, a major medical event, or any significant financial disruption without panic.

Priority 4: Invest for Retirement

With debt cleared and your emergency fund solid, the 20% can go toward building long-term wealth. Contribute to your employer’s 401(k) (especially if they offer a match — that’s free money), open a Roth IRA, or invest in low-cost index funds.

Pro Tip: If your employer matches 401(k) contributions, contribute at least enough to get the full match from day one, even while you’re paying off debt. A 100% match is a guaranteed 100% return on your money — you’ll never find a better deal.

Common Mistakes People Make With the 50/30/20 Rule

After helping many people implement this budget, I’ve seen the same mistakes come up repeatedly. Here’s what to watch out for.

Mistake 1: Using gross income instead of net. The 50/30/20 rule only works with your after-tax, take-home pay. Using your gross salary will throw every calculation off and leave you short at the end of the month.

Mistake 2: Miscategorizing wants as needs. That premium streaming bundle isn’t a need. Neither is the expensive phone plan, the $200 monthly hair appointment, or the daily Starbucks. Being honest about wants versus needs is essential.

Mistake 3: Forgetting irregular expenses. Car registration, annual insurance premiums, birthday gifts, and holiday spending are predictable but not monthly. Divide their annual cost by 12 and include them in the appropriate category.

Mistake 4: Giving up because the percentages don’t work perfectly. If you live in an expensive city and housing alone takes 40% of your income, the strict 50% needs target might be impossible right now. That’s okay. Use the framework as a guideline and adjust to your reality. Maybe your split is 60/20/20 while you work on increasing your income.

Mistake 5: Not adjusting as life changes. Got a raise? Recalculate. Paid off a debt? Redirect that payment to savings. Had a baby? Reassess your needs. Your budget should evolve with your life.

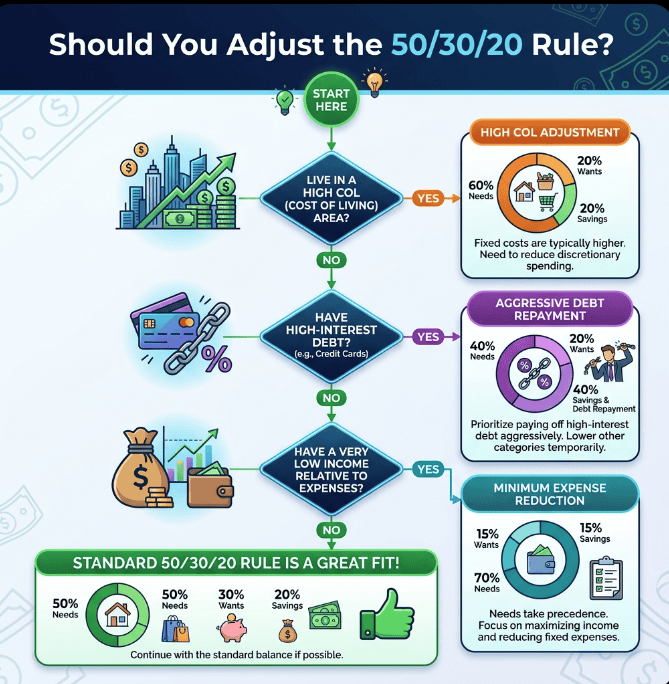

When the 50/30/20 Rule Might Not Work for You

I want to be honest — this rule isn’t perfect for everyone, and that’s okay. Here are situations where you might need to modify it.

If you live in a high cost-of-living area. In cities like San Francisco, New York, or Boston, housing alone can eat 40% to 50% of your income. You may need to temporarily run a 60/20/20 or even 70/15/15 split until you can increase your income or reduce housing costs.

If you have very high debt. Someone carrying $50,000 in student loans and credit card debt might need a more aggressive approach — temporarily shifting to 50/20/30 where 30% goes to debt payoff and only 20% to wants.

If you have a very low income. When you’re earning minimum wage, 50% for needs might not even cover rent. In this case, focus on covering essentials first, cutting every possible want, and working on increasing your income through side hustles or career development.

If you’re already financially comfortable. If you earn well above average, you might want to save 30% or more and reduce wants to 20%. The wealthiest people didn’t get that way by spending 30% on wants.

The 50/30/20 rule is a framework, not a law. Use it as your starting point and customize it for your situation.

How to Set Up Your 50/30/20 Budget in 4 Steps

Step 1: Find Your After-Tax Monthly Income

Check your most recent pay stub for “net pay.” If you’re paid biweekly, multiply by 26 and divide by 12. If you have variable income, use the average of your last three months.

Include all income sources — your main job, side hustles, freelance work, rental income, or any other regular money coming in.

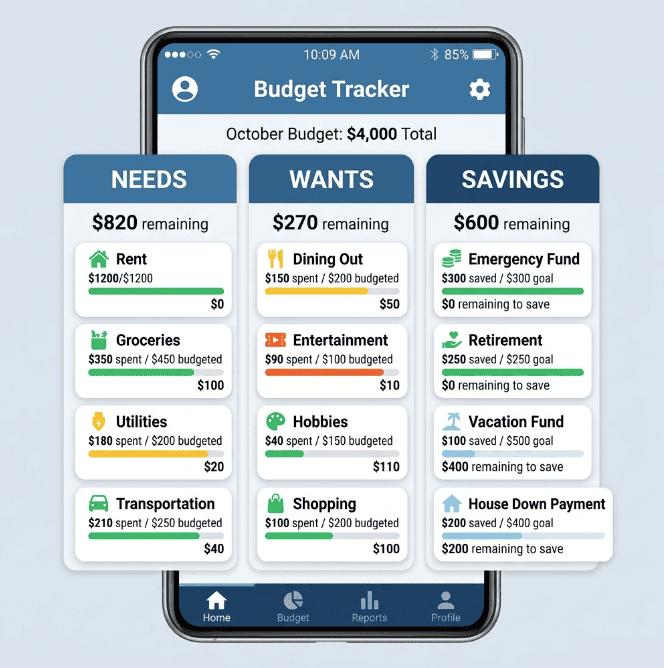

Step 2: Calculate Your Three Numbers

Multiply your monthly income by 0.50, 0.30, and 0.20. Write these three numbers down. These are your spending limits for each category.

Step 3: Categorize Your Current Spending

Go through last month’s bank and credit card statements. Categorize every expense as a Need, Want, or Savings/Debt payment. Add up each category and compare to your target numbers.

This step is almost always an eye-opener. Most people discover their needs are reasonable, their wants are higher than expected, and their savings are lower than they thought.

Step 4: Adjust and Commit

Look at your current spending and your target percentages. Where are the gaps? Usually, wants need to come down so savings can go up.

Pick two or three specific changes you can make this month. Maybe it’s packing lunch instead of buying it three times a week ($180/month saved). Maybe it’s canceling two streaming services ($25/month). Maybe it’s switching to a cheaper phone plan ($30/month).

Small changes in the wants category directly fund your savings goals.

Pro Tip: Automate your savings on payday. As soon as your paycheck hits, have 20% automatically transferred to savings. Then your needs get paid from what’s left. Whatever remains is your wants budget. When it’s gone, it’s gone.

Best Tools for Tracking Your 50/30/20 Budget

You don’t need fancy software to follow this rule, but the right tool makes it easier to stay on track.

YNAB (You Need A Budget) — the most powerful budgeting app available. Costs $14.99/month but comes with a free trial. Users report saving $600+ per month on average. Excellent for the 50/30/20 method.

EveryDollar — free, simple, and built for beginners. Created by Dave Ramsey’s team. Works well for three-category budgeting.

Mint by Credit Karma — automatically categorizes your spending and shows you where your money goes. Free and easy to set up.

Google Sheets — if you prefer spreadsheets, a simple three-category sheet updated weekly gives you complete control and customization. Plenty of free templates available online.

Pen and paper — a notebook with three columns works perfectly. Sometimes the simplest tools are the most effective.

Frequently Asked Questions

Frequently Asked Questions

Is the 50/30/20 rule based on gross or net income?

Always use net income — your after-tax, take-home pay. Using gross income will inflate your budget and leave you short on cash. If you’re unsure of your net income, check the “net pay” line on your most recent pay stub.

What if my needs are more than 50%?

This is common, especially in expensive cities. If your needs exceed 50%, temporarily adjust the ratio. You might run 60/20/20 or even 65/15/20 while you work on reducing costs or increasing income. The key is still having all three categories represented.

Does the 20% savings include retirement contributions?

Yes. Any money going toward your financial future counts — 401(k) contributions, IRA deposits, emergency fund contributions, extra debt payments beyond minimums, and general savings. If your employer matches your 401(k), that match doesn’t count as part of your 20% — it’s bonus money.

Is a gym membership a need or a want?

A want. Exercise is important for health, but you can run outside, do bodyweight exercises at home, or follow free YouTube workouts. A gym membership is a convenience upgrade. That said, if going to the gym is what keeps you consistent with exercise, it might be a worthwhile want.

What about saving more than 20%?

If you can save more than 20%, absolutely do it. Many people pursuing financial independence save 30%, 40%, or even 50% of their income. The 20% is a minimum target, not a maximum.

How do I handle irregular income with this rule?

Use the average of your last three to six months of income. In months where you earn more, save the excess. In months where you earn less, you may need to temporarily reduce wants. Having a stable baseline prevents the financial rollercoaster.

Can I use the 50/30/20 rule to pay off debt faster?

Absolutely. You can temporarily modify the rule to something like 50/20/30 — keeping needs the same, reducing wants to 20%, and allocating 30% to savings and aggressive debt payoff. Once the debt is gone, shift back to the standard 50/30/20.

Start Your 50/30/20 Budget This Week

Start Your 50/30/20 Budget This Week

The 50/30/20 rule isn’t just another budgeting method — it’s a philosophy of balance. It acknowledges that you need to cover your essentials, that you deserve to enjoy your money, and that your future self needs you to save. All three matter. None gets ignored.

If you’ve tried complicated budgets before and given up, give this one a real shot. The simplicity is the point. Three categories. Three numbers. One clear framework that works whether you make $30,000 or $130,000 a year.

Here’s your homework: grab your most recent pay stub, calculate your three numbers, and compare them to how you actually spent money last month. Just that exercise alone will tell you exactly where you stand — and what needs to change.

Your money is working hard. It’s time to make sure it’s working hard for the right things.

Enjoyed this guide? Pin it for later and share it with someone who could use a simpler approach to budgeting. For more practical money tips, explore SaveSmartLive.com.

Related articles:

- How to Create a Monthly Budget That Actually Works (2026 Guide)

- 15 Money Saving Challenges to Try in 2026

- How to Start an Emergency Fund From Zero

- Zero-Based Budget Explained: How to Give Every Dollar a Job

Read More : $50 Weekly Meal Plan for a Family of Four (With Grocery List)