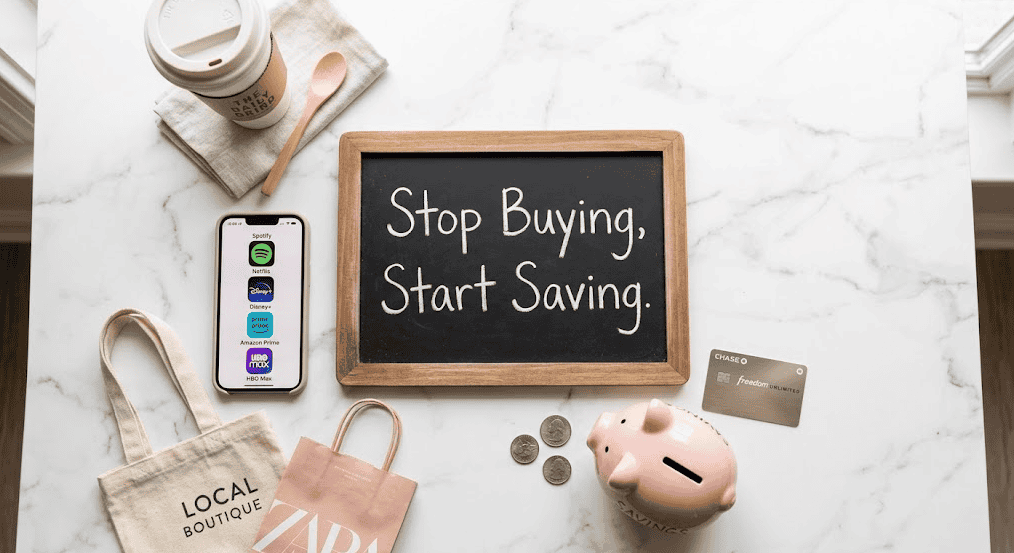

Let’s be honest with each other for a second. Most of us don’t have a saving problem — we have a spending problem. And not even big, dramatic spending. It’s not the vacation or the new couch that’s quietly draining your bank account every month. It’s the small stuff. The $6 coffee. The subscription you forgot you had. The “just one more” online order that shows up in a box you don’t even remember placing.

Here’s the thing — you don’t need a second job to save $500 a month. You don’t need to give up everything you love or live like you’re broke. You just need to get honest about what you’re buying out of habit, boredom, or convenience — and make a few intentional swaps.

This article is going to walk you through 15 specific things to stop buying to save money — things that sound small but add up to hundreds of dollars every single month. Some of these will feel obvious. Others might genuinely surprise you. But all of them are things real people have cut and never once missed.

Ready to find $500 you didn’t know you were losing? Let’s go.

Let’s start with the most classic money-saving advice — because as cliché as it sounds, it’s still one of the biggest leaks in most people’s monthly budget. If you’re stopping at a coffee shop every morning before work, you are likely spending between $5 and $8 per visit. That adds up to $150–$240 every single month just on coffee. Just. Coffee.

Now, this isn’t about telling you that you can’t enjoy a nice latte. Life is short and good coffee genuinely makes mornings better. This is about recognizing when a daily ritual has quietly become a daily expense that you’ve stopped even noticing.

The fix is simpler than you think. Invest once in a quality home espresso machine or a French press. Buy a bag of good coffee beans from the same brand your favorite café uses — most of them are available at grocery stores or online. Learn to make your go-to drink at home. Within two weeks, you’ll have your routine dialed in, and you’ll be saving $120–$200 every single month with almost zero sacrifice in quality.

The Math: $6 daily coffee × 25 workdays = $150/month saved. Keep your one or two “treat” café visits on the weekends. You deserve them.

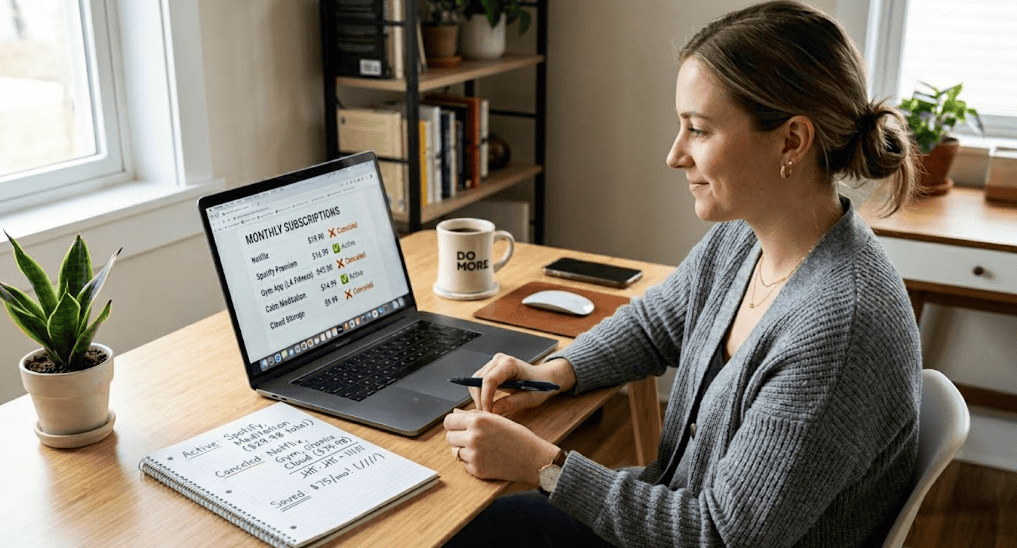

2. Unused Subscriptions You Forgot You Had

This one is the sneakiest budget killer of the modern age — and almost everyone is guilty of it. Think about how many subscriptions are currently quietly charging your credit card every month. Streaming services, music apps, meal planning tools, meditation apps, online magazine subscriptions, fitness platforms, cloud storage, software trials that became paid plans, premium versions of apps you use for free anyway.

Go right now — seriously, pause and look — and check your bank statement for recurring charges. Most people are genuinely shocked to discover they’re paying for 8 to 12 subscriptions they either forgot about, barely use, or completely stopped using months ago.

The average American spends over $200 per month on subscriptions, and studies show that most people underestimate their subscription spending by nearly 200%. That means you think you’re spending $50 and you’re actually spending $150. It’s practically a magic trick — except the money is disappearing from your account, not your hand.

The Action Plan: Go through your bank and credit card statements line by line. Write down every recurring charge. Then ask yourself honestly: “Did I use this in the last 30 days?” If the answer is no, cancel it today. You can always re-subscribe later if you genuinely miss it — but you won’t. You haven’t missed it yet, have you?

3. Bottled Water

If you are regularly buying single-use plastic water bottles — whether from the grocery store in cases or individually at gas stations and convenience stores — you are spending money on something you could get essentially for free. And you’re generating a significant amount of plastic waste in the process.

A case of 24 water bottles costs around $4–$6 at the grocery store. Most families go through one or two cases a week. That’s $20–$48 per month, and some households spend far more when you add in individual bottle purchases on the go.

The solution costs you money once and saves you money forever. A quality water filter pitcher (like a Brita or PUR) costs around $25–$35 and replacement filters cost about $5–$7 each and last for months. A good insulated reusable water bottle — the kind that keeps your water ice cold for 24 hours — costs $20–$35 and lasts for years. Together, that’s a one-time investment that pays for itself within the first month.

Bonus Benefit: You’ll actually drink more water because your reusable bottle is always with you. Your skin will look better. Your energy will improve. Your wallet will be fuller. There is genuinely no downside to this swap.

4. Convenience and Pre-Packaged Foods

We live in an age of extreme convenience, and the food industry has made a fortune charging us premium prices for the privilege of not having to do five extra minutes of work. Pre-cut vegetables. Individual snack packs. Pre-washed salad bags. Single-serve yogurt cups. Microwave meal kits. Individually packaged everything.

Every single one of these items costs dramatically more per ounce than their non-convenience counterparts. A bag of pre-washed, pre-cut broccoli florets costs about twice as much as a whole head of broccoli that takes 90 seconds to break apart. A six-pack of individual snack-sized chip bags costs more than a large bag you could portion yourself into a reusable container in under a minute.

Think about how many convenience premiums you’re paying every time you shop. It’s not just one item — it’s twenty items, each costing 30–100% more than the unprocessed version. For a family doing a full weekly grocery run, this convenience tax can easily add $50–$80 per month to your grocery bill without you ever noticing.

The Swap: Buy whole, unprocessed versions of the foods you love. Wash and prep them yourself when you get home — make it part of your Sunday routine. Wash and dry your salad greens, cut up your vegetables, portion your snacks into small reusable containers. This ten-minute weekly task can save you hundreds of dollars a year.

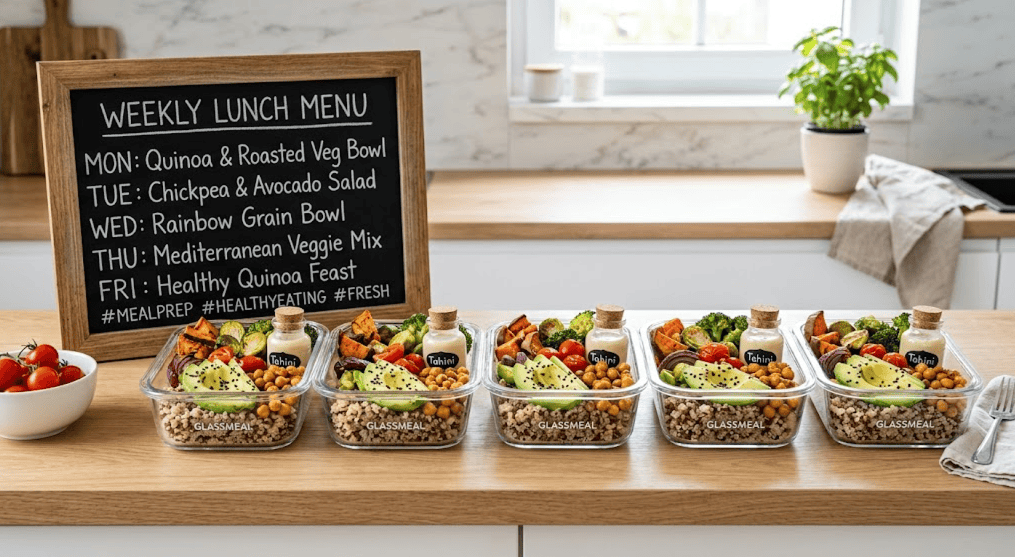

5. Eating Out for Lunch Every Workday

Lunch is the meal that silently destroys more budgets than almost any other single habit. It feels harmless — you’re just grabbing something quick, you’re busy, you deserve a break from your desk, it’s only $12. But $12, five days a week, four weeks a month? That’s $240. Every month. Just lunch.

If you’re grabbing coffee too (see Idea #1), your midday spending alone can easily reach $300–$350 per month. That’s a car payment. That’s a significant chunk of rent. That’s a plane ticket.

The good news is that you don’t have to eat sad desk lunches to fix this. Meal prepping for the workweek is genuinely one of the highest-ROI financial habits you can build. Spend an hour on Sunday making a big batch of something you actually love — a grain bowl with roasted vegetables and a delicious sauce, a pot of soup you can portion into individual containers, a big pasta salad, or marinated proteins you can throw into wraps or bowls throughout the week.

When your lunch is something you actually made with care and that tastes great, you stop feeling like you’re depriving yourself. You start feeling proud of yourself. And the $150–$200 you save every month starts adding up in ways that are very, very motivating.

6. Brand Name Products When Generic Works Just as Well

This is the money-saving tip that sounds obvious but that almost no one actually does consistently — because brand loyalty is powerful and marketing is very, very good at its job.

Here is a fact that the food and consumer goods industry does not want you to think too hard about: generic store-brand products are often made in the exact same factories as the name-brand versions. The pasta, the canned tomatoes, the acetaminophen, the dish soap, the baking soda, the flour — frequently identical product, completely different price tag.

The price difference between name-brand and generic can range from 20% to 50% depending on the product category. Over a full monthly grocery run, switching strategically from brand name to generic on items where quality is genuinely identical can save $40–$80 per month for a single person, and significantly more for families.

The Smart Approach: You don’t have to go fully generic on everything. There are some products where brand genuinely matters to you — maybe it’s your favorite coffee creamer, or a specific brand of pasta sauce you love. Keep those. But look at everything else in your cart with fresh eyes. The cleaning products, the pantry staples, the over-the-counter medicines, the paper goods — try the generic version once. You’ll be surprised how often you can’t tell the difference.

7. Impulse Purchases While Online Shopping

Online shopping has made impulse buying dangerously easy. You’re scrolling through your phone before bed, you see something interesting, it’s on sale, free shipping with Prime, one click and it’s ordered before your brain has even finished the thought. Three days later a box arrives and you barely remember what’s in it.

This is not a willpower problem. It is a design problem. Online shopping platforms spend hundreds of millions of dollars engineering their apps and websites specifically to make buying feel effortless and delaying feel difficult. The one-click purchase, the countdown sale timer, the “only 3 left in stock” warning — all of it is designed to short-circuit your decision-making process and get you to buy before you think.

The single most effective tool against impulse online shopping is something called the 48-Hour Rule. When you see something you want online, instead of buying it, add it to a wishlist or a separate “want” folder. Set a reminder for 48 hours later. If you still genuinely want it after 48 hours of not thinking about it, buy it. If you forgot about it — and you will forget about it more often than you think — you just saved yourself that money.

Most impulse purchases are driven by emotion in the moment, not genuine need or sustained desire. The 48-hour gap creates space for that emotion to pass. People who use this rule consistently report saving $100–$200 per month almost immediately.

8. Gym Memberships You Never Use

January first. You’re motivated. You sign up for the gym. You go four times in January, twice in February, once in March, and then… you stop going. But the membership? That quietly charges your account every single month like clockwork. You keep meaning to cancel it. You keep telling yourself you’ll start going again. You don’t. The months roll by. The money disappears.

This is one of the most common and most expensive passive money drains in existence. The fitness industry is actually built around this model — they sign up far more members than their facilities could ever accommodate, because they know most people will pay and never show up.

If you have a gym membership and you are not going at least 8–10 times per month, you are not getting your money’s worth. A typical gym membership costs $30–$80 per month. That’s $360–$960 per year for equipment you’re not using.

The Honest Conversation: Before you cancel, ask yourself why you’re not going. Is it inconvenient? Is it intimidating? Is it that you just don’t enjoy that kind of workout? If the gym genuinely isn’t working for you, free alternatives are genuinely excellent. YouTube has thousands of free, high-quality workout programs — strength training, yoga, Pilates, HIIT, running plans — for every fitness level. Your neighborhood is free. Bodyweight workouts require nothing.

Cancel the membership you’re not using. Your bank account will feel it immediately.

9. Fast Fashion and Trend-Chasing Clothes

Fast fashion is one of the most expensive habits disguised as a bargain. The prices are low, which makes it feel like you’re being smart with your money. But the reality is that cheap clothing wears out, goes out of style, or falls apart so quickly that you end up buying more, more often — and spending far more in total than if you’d invested in fewer, better-quality pieces to begin with.

The average American spends over $1,800 per year on clothing — and a significant chunk of that is on fast fashion items that get worn a handful of times before being discarded. Think about your own closet for a moment. How many items in there have tags still on them? How many did you buy because they seemed like a great deal, wore once, and never reached for again?

Trend-chasing is the engine that drives this cycle. When you buy something because it’s trendy right now, it has a built-in expiration date — the trend passes, the item no longer feels current, and you need something new. It’s a treadmill designed to keep you spending.

The Alternative: Build a small, intentional wardrobe of classic pieces in neutral colors that genuinely work together and that you actually love wearing. Buy secondhand when possible — thrift stores and resale apps like ThredUp and Poshmark have incredible finds at a fraction of retail prices. Set a monthly clothing budget and stick to it. A “one in, one out” rule (for every new item you buy, one old item leaves your closet) keeps things from accumulating and helps you buy more mindfully.

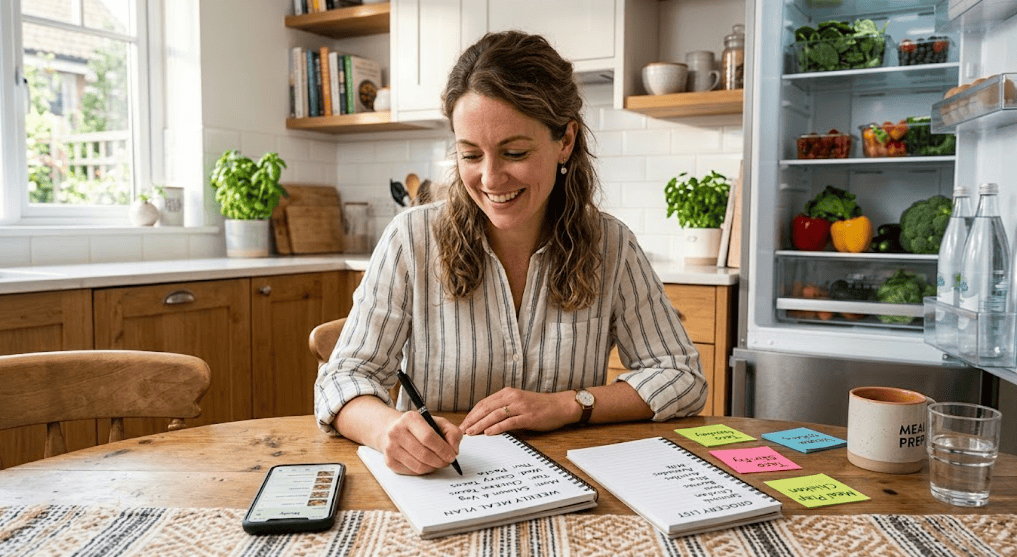

10. Excessive Grocery Shopping Without a List

Going to the grocery store without a plan is one of the most reliable ways to spend $40–$80 more than you intended every single time. You walk in for five things and walk out with thirty. The endcap display got you. The sale signs got you. The fact that you were hungry when you shopped got you.

Grocery stores are masterfully designed environments built to maximize how much you spend. The staples you need — milk, eggs, bread — are placed at the back so you have to walk through the entire store to reach them. The most expensive items are placed at eye level. The checkout lane is stocked with impulse purchases. None of this is accidental.

The single most powerful thing you can do to cut your grocery bill is also the simplest: make a meal plan and a list before you shop, and stick to it. Plan out every meal you intend to cook that week. Write down exactly what you need. Shop only from that list.

This one habit, done consistently, can cut grocery spending by 20–30% for most households. That’s $50–$100 per month for a single person, and $100–$200 per month for a family, just from being more intentional before you walk through the doors.

Pro Tips: Never shop hungry. Shop the perimeter of the store first (fresh produce, proteins, dairy) before going into the middle aisles. Use a grocery store app to check your total as you shop so there are no surprises at checkout.

11. Lottery Tickets and Scratch Cards

This one might feel like a small thing — and individually, it is. A scratch card here, a lottery ticket there. But if you’re buying these regularly, even just a few times a week, the cost adds up far more than most people realize. And the expected return is mathematically almost always negative.

The average regular lottery ticket buyer spends around $50–$100 per month on lottery tickets and scratch cards. Over the course of a year, that’s $600–$1,200 spent on something with an expected return of about 50 cents per dollar. It is one of the worst financial returns of any common spending habit.

The dream that a $2 ticket will change your life is psychologically very powerful — and that’s exactly why lottery and scratch card marketing works so well. Hope is a very compelling product. But the math is brutally clear: you are far more likely to build genuine financial security through consistent small savings than through any lottery ticket ever printed.

The Reframe: Take that $50–$100 per month and put it into a high-yield savings account instead. It won’t make you a millionaire overnight. But in 12 months you’ll have $600–$1,200 in real, accessible money that you actually have. That’s a real emergency fund. That’s a real vacation. That’s a real financial cushion — none of which the lottery ticket gives you.

12. Paying for Shipping on Every Online Order

Free shipping has trained us to feel like we’re getting a deal when we reach the order minimum for it — but it’s also trained us to place orders far more frequently than we otherwise would. The result? We might be avoiding the $5.99 shipping fee, but we’re placing three separate orders where we used to place one, spending more overall.

And when we don’t hit the free shipping minimum, we do one of two things: we either pay the shipping fee ($5–$15 per order), or we add items to our cart to reach the minimum — which means we’re spending more money to avoid paying for shipping. Both outcomes cost us money.

Here’s how to genuinely win at this game: Consolidate your orders. Instead of ordering things as you think of them, keep a running list and place one larger order once a week or once every two weeks. You’ll qualify for free shipping more naturally, you’ll place fewer impulse orders, and you’ll save on both shipping fees and the extra items you add unnecessarily.

Also consider: does the thing you’re ordering exist locally? Sometimes the most cost-effective choice is simply walking into a store and buying the one item you need, rather than placing an online order with shipping costs and a 3–5 day wait. The convenience of online ordering has real value, but it’s worth checking first.

Organized skincare products on a bathroom vanity promoting budget-friendly self-care tips.

13. Excessive Beauty and Skincare Products

Walk into any beauty retailer and it’s designed to make you feel like you need everything. The serums, the toners, the essences, the eye creams, the overnight masks, the mists, the exfoliants — each one promising to solve a different problem, each one suggesting that without it, your skin is somehow lacking.

The beauty industry is worth hundreds of billions of dollars and it spends a significant portion of that money on marketing designed specifically to create insecurity and then immediately offer to solve it for $45 per product. And it works, because it makes us feel like we’re investing in ourselves.

But here’s the honest truth that dermatologists have been saying for years: an effective skincare routine does not require twelve products. A gentle cleanser, a good moisturizer with SPF, and a targeted treatment for your specific concern (retinol, vitamin C, or whatever your dermatologist recommends) is genuinely all most people need. Everything else is largely redundant.

Take an honest look at your bathroom counter or cabinet. How many half-used products are sitting there? How many did you buy because of an influencer recommendation or a sale? How many do you actually use consistently? For most people, the answer reveals $50–$150 per month spent on beauty products they don’t really need.

The Challenge: Use up what you already have before buying anything new. This one rule alone, for most people, means not buying anything for two to three months.

14. Paying Full Price When Sales and Coupons Are Available

This isn’t about becoming an extreme couponer with binders full of paper clippings. This is about the much simpler habit of never paying full retail price for something when a discount is consistently available — and in 2025, discounts are almost always available if you take 30 seconds to look.

Think about the last few things you bought online. Did you check for a coupon code before checking out? Did you check if the item was cheaper on a competing site? Did you check if the browser extension Honey or Capital One Shopping would auto-apply a discount? If you didn’t do any of these things, there is a very real chance you left money on the table.

For clothing, furniture, and home goods — most retailers run predictable sales cycles. Furniture goes on sale around holiday weekends. Clothing goes deeply discounted at the end of each season. Appliances go on sale during Black Friday and Labor Day. If you can wait even a few weeks on a non-urgent purchase, you can often get 20–40% off.

Apps and Tools to Use: Download Honey or Capital One Shopping (they auto-find coupon codes at checkout). Sign up for email lists of stores you shop at regularly — they almost always send a welcome discount code, plus exclusive sale alerts. Use Rakuten for cash back on online purchases. These tools take minutes to set up and save real money with zero ongoing effort.

15. Energy You’re Paying for But Not Using

This final one is the most invisible — which is exactly why it’s often overlooked. Your electricity and utility bills might be significantly higher than they need to be because of habits so automatic you’ve stopped seeing them.

Lights left on in empty rooms. Devices left on standby or plugged in when not in use (this is called “vampire energy” — electronics that draw power even when they appear to be off). A thermostat set aggressively high or low when nobody is home. A refrigerator with a gasket that doesn’t seal properly. A water heater set 20 degrees higher than necessary.

None of these feel like spending money. But collectively, energy waste can add $50–$100 to your monthly utility bill that you are literally paying for without receiving any benefit. The lights aren’t illuminating anything. The electronics aren’t doing anything. The extra heat or cooling isn’t making anyone more comfortable — the house is empty.

The Fixes — All Free or Nearly Free:

Switch to LED bulbs (they use up to 80% less energy than traditional bulbs). Install a smart or programmable thermostat (a one-time cost of $25–$120 that typically saves $100–$180 per year). Unplug devices and chargers when not in use or plug them into a smart power strip that cuts standby power automatically. Set your water heater to 120°F instead of the default 140°F — you won’t notice the difference in your shower and you’ll see it in your bill.

The Mindset Shift: Start thinking of every light switch and every plug as a small cash register. Every time you leave a light on in an empty room, you’re inserting a coin into a machine that gives you nothing. That small mental reframe makes the habit change remarkably easy to stick with.

Conclusion: You Don’t Need More Money — You Need Fewer Leaks

Here’s the mindset shift that changes everything: you are probably not underpaid. You are almost certainly over-spending — but not on the things you think. It’s not the one big splurge. It’s the daily coffee, the forgotten subscription, the impulse order, the convenience premium, the energy you’re paying for in an empty room.

When you add up all 15 things in this list, the potential monthly savings are real:

Daily coffee shop drinks: $150

Unused subscriptions: $60–$100

Bottled water: $20–$40

Convenience foods: $50–$80

Eating out for lunch: $150–$200

Brand-name premiums: $40–$80

Impulse online purchases: $50–$100

Unused gym membership: $30–$80

Fast fashion: $50–$100

Unplanned grocery trips: $50–$100

Lottery tickets: $30–$50

Unnecessary shipping: $20–$40

Excess beauty products: $40–$80

Paying full price: $30–$60

Wasted energy: $40–$80

Total potential monthly savings: $800–$1,390.

You don’t have to tackle all 15 at once. Pick three that resonate most with your life. Start there. Build the habit. Then add another. Small, consistent changes compound into genuinely life-changing financial results — and the best part is, after a few weeks, you won’t even miss what you stopped buying.

The $500 was always there. You just didn’t know where to find it.