I was sitting at my kitchen table at 11 PM on a Wednesday, staring at a pile of bills and a spreadsheet that made my stomach hurt. Two credit cards. A car loan. A personal loan from when the furnace died. Student loans. Total debt: just over $37,000.

I knew I needed a plan. I had been making minimum payments on everything for years, and the balances barely moved. It felt like running on a treadmill — exhausting effort, zero progress.

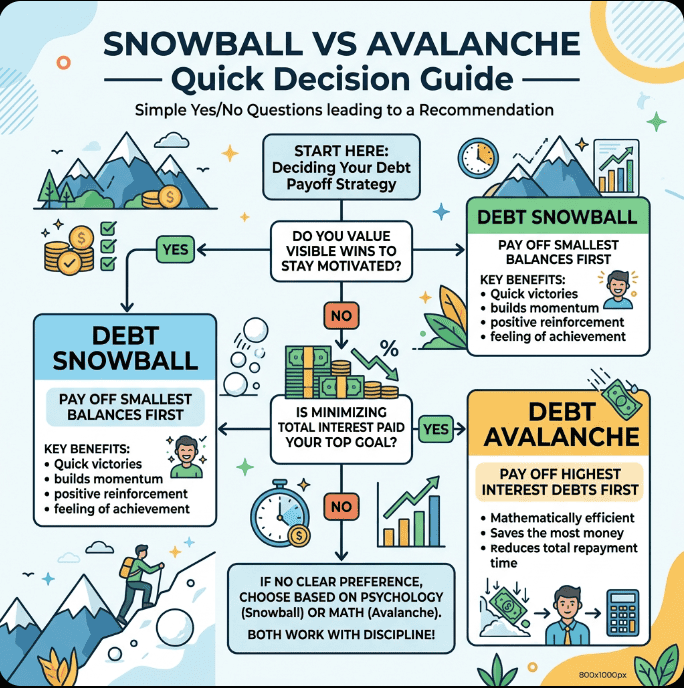

That night I discovered that there are really only two serious strategies for paying off debt: the debt snowball and the debt avalanche. Both work. Both have helped millions of people become completely debt-free. But they work differently, they feel different, and depending on your personality and your specific debt situation, one will almost certainly work better for you than the other.

This guide will break down both methods in complete detail, compare them head-to-head with real numbers, help you figure out which one fits your life, and give you a step-by-step plan to start using it today.

Because here’s the truth nobody talks about — picking the “mathematically perfect” strategy matters less than picking the one you’ll actually stick with long enough to cross the finish line.

What Is the Debt Snowball Method?

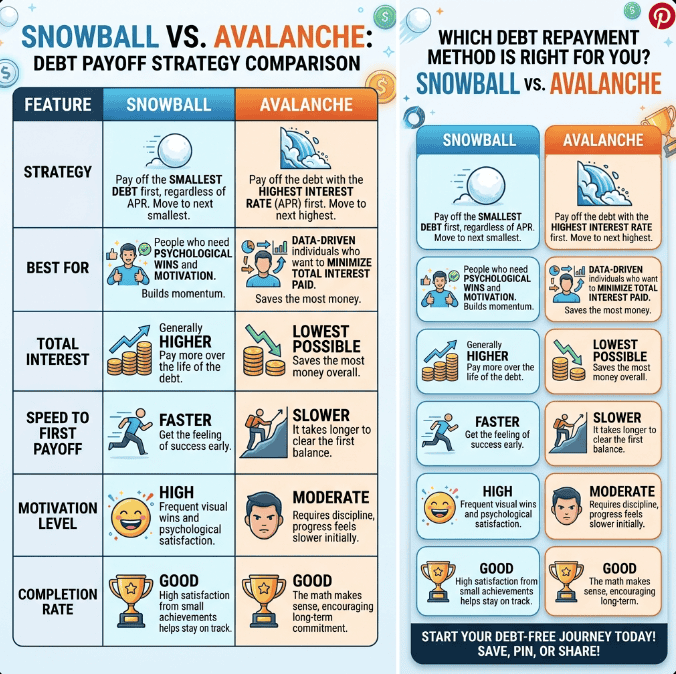

The debt snowball method was popularized by Dave Ramsey, and it’s built on a simple, powerful idea: pay off your smallest debt first, regardless of interest rate.

Here’s how it works step by step.

Step 1: List all your debts from smallest balance to largest balance. Ignore interest rates completely — only the balance matters.

Step 2: Make minimum payments on every debt except the smallest one.

Step 3: Throw every extra dollar you can find at the smallest debt. Attack it with everything you’ve got.

Step 4: When the smallest debt is paid off, take the entire payment you were making on it (minimum payment plus the extra) and add it to the minimum payment of the next smallest debt.

Step 5: Repeat until every debt is gone.

The payment “snowballs” — it grows larger with each debt you eliminate because you keep rolling the previous payments into the next target.

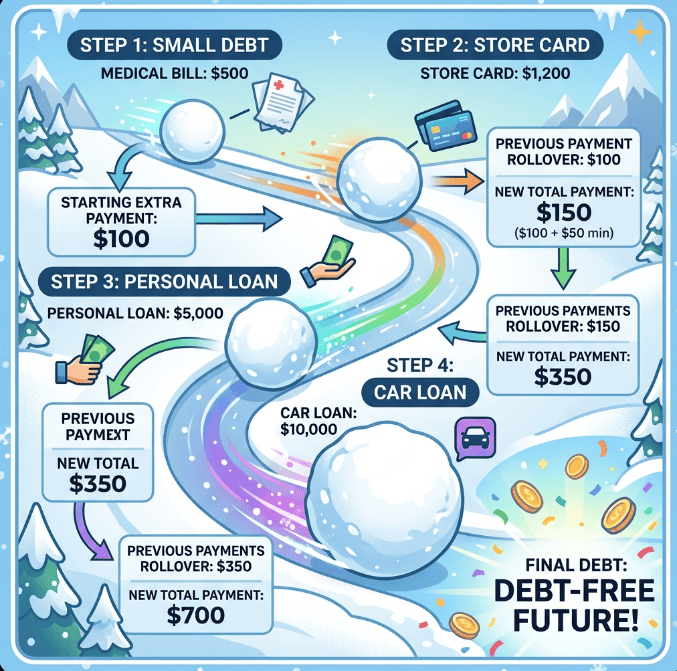

Debt Snowball Example With Real Numbers

Let’s say you have four debts and $500 per month to put toward debt payments above the minimums.

Car Loan: $9,000 balance, 6% interest, $250 minimum payment

Total debt: $17,500

With the snowball method, you’d attack Credit Card A first (smallest balance). You pay the $25 minimum plus your extra $500, throwing $525 per month at it. In less than two months, it’s gone.

Now you take that $525 and add it to the Medical Bill’s $100 minimum. You’re now paying $625 per month on the medical bill. It’s gone in about 3.5 months.

Next, you roll that $625 into Credit Card B’s $110 minimum. Now you’re paying $735 per month. Gone in about 7 months.

Finally, the full $735 rolls into the car loan’s $250 minimum. You’re now throwing $985 per month at it. The remaining balance disappears in about 7 months.

Total time to debt-free: approximately 20 months.

The snowball effect is real. Your payment started at $525 and grew to $985 without you earning a single extra dollar. That momentum is incredibly motivating.

Debt Snowball vs Debt Avalanche

What Is the Debt Avalanche Method?

The debt avalanche method is the mathematician’s approach. Instead of targeting the smallest balance, you target the debt with the highest interest rate first.

The logic is straightforward — high-interest debt costs you the most money over time, so eliminating it first saves you the most in total interest paid.

Here’s how it works.

Step 1: List all your debts from highest interest rate to lowest interest rate. Ignore balances — only the rate matters.

Step 2: Make minimum payments on every debt except the one with the highest interest rate.

Step 3: Throw every extra dollar at the highest-interest debt.

Step 4: When it’s paid off, move to the next highest interest rate and repeat.

Car Loan: $9,000 balance, 6% interest, $250 minimum

Medical Bill: $2,200 balance, 0% interest, $100 minimum

With the avalanche method, you’d attack Credit Card A first (highest interest at 22%). Same as the snowball in this case. Gone in less than 2 months.

Next, you’d attack Credit Card B (18% interest, $5,500 balance). You pay $635 per month. This takes about 9 months.

Then the Car Loan (6% interest). You pay $885 per month. About 8 months.

Finally, the Medical Bill (0% interest). You pay $985 per month. About 2 months.

Total time to debt-free: approximately 21 months.

Wait — that’s almost the same as the snowball! In this particular example, the difference is only about one month and roughly $400 in total interest saved. That’s because the highest-interest debt also happened to be the smallest balance.

But here’s where the avalanche shines — when your highest-interest debt has a large balance. If that $5,500 credit card at 18% were your first target instead of the $800 card, you’d save significantly more interest over the repayment period.

Pro Tip: The difference between snowball and avalanche savings depends entirely on your specific debt mix. For some people, it’s hundreds of dollars. For others, it’s thousands. Run both calculations for your own debts to see the actual difference.

Let me break down the honest pros and cons of each method so you can see which one aligns with how you think and how you’re motivated.

The Debt Snowball: Pros

Quick wins build momentum. Paying off your first debt in 1-2 months feels incredible. That emotional boost drives you to keep going. Studies from Harvard Business School confirm that people who tackle smaller tasks first are more likely to follow through on larger ones.

It’s simple. Sort by balance, attack the smallest. No interest rate calculations, no spreadsheets needed. Even on your most exhausted day, the plan is clear.

It works for emotional spenders. If your debt problem is partly behavioral — emotional spending, lack of motivation, history of starting and quitting — the snowball’s quick rewards address the root cause. It rewires your relationship with money through positive reinforcement.

Early freed-up cash flow. Eliminating small debts quickly frees up their minimum payments, which gives you more breathing room in your monthly budget sooner.

The Debt Snowball: Cons

You may pay more interest. By ignoring interest rates, you might keep a high-interest credit card alive longer than necessary, which costs you more in total interest.

It can take slightly longer. In some debt configurations, the snowball method results in a few extra months to become debt-free.

It’s not always the financially optimal choice. If pure math is your priority, the avalanche is technically superior.

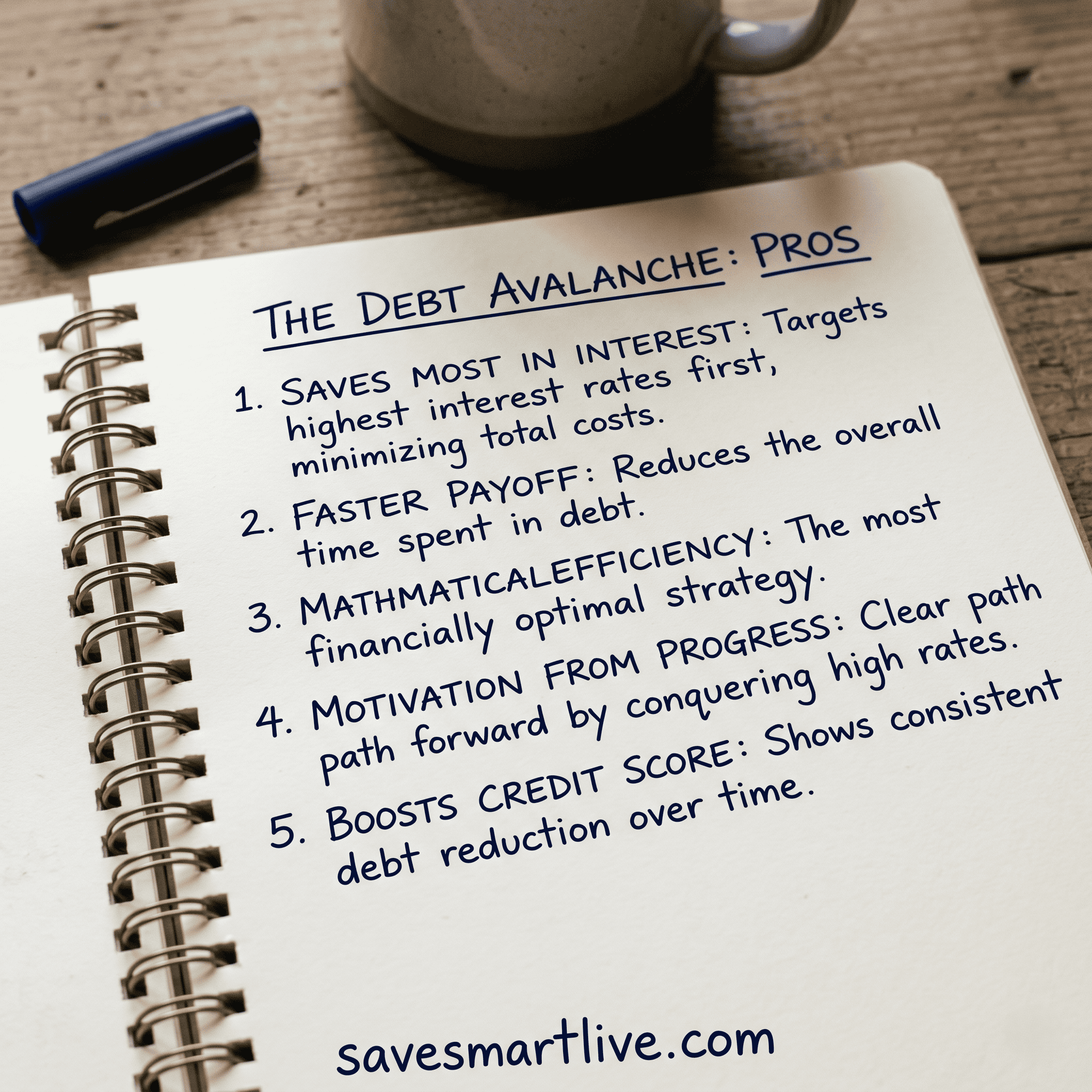

The Debt Avalanche: Pros

Saves the most money. By targeting high-interest debt first, you pay the least total interest over the life of your repayment plan. For people with large high-interest balances, this can mean saving $1,000 to $5,000 or more.

Mathematically optimal. The avalanche is the most efficient path from a pure numbers perspective. If you’re analytical and motivated by logic, this approach aligns with how you think.

Faster total payoff (sometimes). Because you’re eliminating the costliest debt first, the total repayment timeline can be shorter — though the difference varies by situation.

The Debt Avalanche: Cons

Slow early progress. If your highest-interest debt also has a large balance, it could take 6 to 12 months before you pay off your first debt. That long stretch without a “win” causes many people to lose motivation and quit.

Psychologically harder. Making payments for months without seeing a debt balance hit zero is discouraging. The emotional reality of debt payoff matters just as much as the math, and the avalanche ignores the emotional component.

More people quit. This is the biggest downside. Research consistently shows that people using the snowball method are more likely to become completely debt-free than those using the avalanche. The mathematically inferior strategy actually produces better real-world results because people stick with it.

Which Method Should You Choose?

Here’s my honest recommendation after studying both methods and watching hundreds of people go through debt payoff.

Choose the Debt Snowball if:

You’ve tried to pay off debt before and quit

You’re motivated by visible progress and quick wins

Your debt balances are varied (some small, some large)

You tend to be an emotional or impulsive spender

You need the psychological boost of crossing debts off your list

The interest rate difference between your debts is small (less than 5%)

Choose the Debt Avalanche if:

You’re highly disciplined and won’t quit even without early wins

You’re motivated by math and logic rather than emotion

You have one debt with a significantly higher interest rate than the others

The total interest savings is substantial (run the numbers to check)

You’re comfortable with delayed gratification

Or… Choose the Hybrid Approach

Here’s something most guides won’t tell you — you don’t have to pick one method exclusively. Many successful debt-payers use a hybrid approach.

Start with the snowball. Pay off your smallest 1-2 debts quickly to build confidence and momentum. Celebrate those wins.

Then switch to the avalanche. Once you’ve proven to yourself that you can pay off debt, redirect your snowball payment toward the highest-interest remaining debt.

This gives you the psychological benefits of the snowball and the mathematical benefits of the avalanche. It’s the best of both worlds, and it works incredibly well in practice.

Pro Tip: The difference between snowball and avalanche success is rarely about the strategy itself. It’s about consistency. The person who picks either method and sticks with it for 24 months will beat the person who spends 6 months deciding which method is “optimal” and never starts.

How to Start Your Debt Payoff Plan Today

Regardless of which method you choose, here are the exact steps to begin.

Step 1: List Every Debt You Owe

Write down every single debt. Include the creditor name, total balance, interest rate, and minimum monthly payment. Don’t skip any — student loans, credit cards, medical bills, car loans, personal loans, money owed to family members, buy-now-pay-later balances, everything.

Step 2: Choose Your Order

If snowball, sort by balance (smallest to largest). If avalanche, sort by interest rate (highest to lowest). If hybrid, start with the 1-2 smallest debts, then switch to highest interest.

Step 3: Find Extra Money to Throw at Debt

Your minimum payments keep you afloat. Extra payments sink the debt. Find at least $100 to $300 of extra money per month through budget cuts, side hustles, or redirecting savings.

Common sources of extra money: cutting subscriptions ($30-$100/month), reducing dining out ($50-$200/month), selling unused items ($200-$500 one-time), picking up a side hustle ($200-$1,000/month), redirecting savings temporarily.

Step 4: Automate Minimum Payments

Set up autopay for the minimum payment on every debt except your target debt. This ensures you never miss a payment (which would hurt your credit score) and lets you focus all your energy on the target debt.

Step 5: Attack Your Target Debt

Every extra dollar — every birthday gift, every cash back reward, every overtime paycheck, every leftover budget dollar — goes to the target debt. Be relentless. Be obsessed. This debt needs to feel your fury.

Step 6: Celebrate Each Payoff, Then Roll

When a debt hits zero, take a moment to celebrate. Tell someone. Post about it. Feel proud. Then immediately roll that entire payment into the next debt. Don’t let the freed-up cash disappear into lifestyle inflation.

Staying Motivated During Your Debt-Free Journey

Paying off debt is a marathon, not a sprint. Most people take 18 to 36 months to become completely debt-free. That’s a long time to stay motivated. Here’s how to keep going when it gets hard.

Track your progress visually. Print a debt payoff tracker, coloring chart, or thermometer and display it somewhere you’ll see it daily. Watching the colors fill in or the thermometer rise creates tangible evidence of your progress.

Calculate your “debt-free date.” Use a debt payoff calculator (undebt.it is a great free one) to estimate the exact month and year you’ll be debt-free. Having a concrete date to look forward to is surprisingly powerful.

Find your community. Join debt-free communities on Reddit (r/debtfree, r/personalfinance), Facebook groups, or follow debt payoff accounts on Instagram and Pinterest. Surrounding yourself with people on the same journey keeps you accountable and inspired.

Remember your “why.” Why do you want to be debt-free? Write it down. Maybe it’s to stop feeling anxious about money. Maybe it’s to save for your kids’ education. Maybe it’s to retire early. Whatever your why is, revisit it whenever motivation dips.

Don’t compare your journey. Someone on the internet paid off $80,000 in 12 months on a $200,000 salary. Good for them. Your journey is yours. Paying off $8,000 in 24 months on a $40,000 salary is just as impressive. Progress is progress.

Frequently Asked Questions

Which method saves more money — snowball or avalanche?

The avalanche method saves more money in total interest paid because it targets high-interest debt first. However, the difference varies widely depending on your specific debts. For some people, the savings difference is only $100 to $200. For others with large high-interest balances, it could be $2,000 to $5,000 or more.

Which method is faster?

It depends on your debt configuration. The avalanche is often slightly faster in total time to debt-free, but the difference is usually small — a few months at most. The snowball gives you faster first wins (your smallest debt is eliminated quickly), which feels faster even if the total timeline is similar.

What if my smallest debt also has the highest interest rate?

Then you’ve hit the jackpot — both methods tell you to pay it off first. This is actually quite common. Start there and reassess your strategy after the first debt is gone.

Should I stop saving while paying off debt?

Keep making 401(k) contributions up to your employer match (that’s free money you don’t want to lose), and maintain a small $1,000 emergency fund. Beyond that, temporarily pause extra savings and throw everything at debt. Once you’re debt-free, you can save aggressively.

What about student loans — snowball or avalanche?

If student loans are your only debt, the avalanche typically works better because student loan interest rates can vary significantly between loans (3% to 7%+). Target the highest-rate loans first. If you have student loans mixed with credit card debt, consider the snowball for the credit cards (emotional wins) and the avalanche for the student loans (interest savings).

Can I switch methods midway through?

Absolutely. Many people start with the snowball for the initial motivation, then switch to the avalanche once they’ve built confidence and momentum. There’s no rule that says you have to commit to one method forever.

What if I can’t find any extra money for debt payments?

Focus on two things simultaneously: reducing expenses and increasing income. On the expense side, audit every recurring charge and eliminate anything non-essential. On the income side, even a small side hustle adding $200 to $400 per month can dramatically accelerate your debt payoff timeline.

The Only Wrong Method Is No Method

Here’s what I want you to take away from this guide. The debt snowball and debt avalanche are both proven strategies that have helped millions of people become completely debt-free. The mathematical difference between them is real but often smaller than people expect. The psychological difference is enormous.

Pick the method that matches how your brain works. If you need quick wins, snowball. If you’re motivated by efficiency, avalanche. If you want both, use the hybrid approach.

But please — pick something. The worst financial plan is no plan at all. Every month you spend making only minimum payments is another month of interest working against you, another month of stress, another month of your paycheck belonging to someone else.

You deserve to keep the money you earn. You deserve the freedom that comes from owing nothing to anyone. And you deserve to start that journey today.

Grab a piece of paper. Write down your debts. Pick your method. And take the first step toward a life without debt.

It’s waiting for you.

Save this guide to your Pinterest and share it with someone fighting their way out of debt. For more debt payoff strategies and money tips, visit SaveSmartLive.com.

Which Method Should You Choose?

Which Method Should You Choose?

Staying Motivated During Your Debt-Free Journey

Staying Motivated During Your Debt-Free Journey The Only Wrong Method Is No Method

The Only Wrong Method Is No Method