start an emergency fund from zero

I want to tell you about the worst Tuesday of my life. I woke up, drove to work, and my car started making a grinding noise that I knew — even with zero mechanical knowledge — was going to be expensive. The mechanic confirmed it. $1,400 for a new transmission part. My checking account had $212 in it. My savings account? Zero. Literally zero.

I ended up putting the repair on a credit card at 24% interest. It took me almost a year to pay it off, and by the time I did, I had paid nearly $1,700 total for a $1,400 repair. That extra $300 went straight to the credit card company. For nothing.

That Tuesday taught me something I will never forget. Not having an emergency fund doesn’t just leave you unprepared. It actively makes your life more expensive. Every surprise bill, every unexpected cost, every financial curveball hits harder when there’s no cushion to absorb it. You end up borrowing money, paying interest, accumulating debt, and digging a deeper hole.

If you’re reading this with $0 in savings, I get it. I’ve been exactly where you are. But I’m also proof that you can build an emergency fund from absolutely nothing — even when money is tight. This guide will show you exactly how.

What Is an Emergency Fund and Why Does It Matter So Much?

An emergency fund is money you set aside specifically for unexpected, necessary expenses. Not for vacations. Not for holiday shopping. Not for that jacket you’ve been eyeing. Emergencies only.

What counts as an emergency? Things like unexpected car repairs, medical bills not covered by insurance, emergency home repairs (like a busted water heater in January), sudden job loss, or an urgent flight to help a family member.

What doesn’t count? A great sale at your favorite store, a friend’s birthday dinner, a concert you forgot was this weekend, or anything you could have predicted and planned for.

Here’s why this fund matters more than almost anything else in your financial life.

It prevents debt spirals. Without savings, every surprise bill goes onto a credit card. Credit card interest compounds, minimum payments barely touch the principal, and before you know it, a $500 surprise has become $700 of debt that takes a year to pay off. An emergency fund breaks this cycle completely.

It reduces stress dramatically. Financial stress is one of the leading causes of anxiety, relationship problems, and even physical health issues. Having even $1,000 in the bank creates a psychological safety net that changes how you feel every single day. You sleep better. You worry less. You make better decisions because you’re not operating from a place of panic.

It protects your other financial goals. Without an emergency fund, every unexpected expense derails your budget, your debt payoff plan, and your savings goals. That $300 you’ve been putting toward your credit card payment? Gone when the washing machine breaks. The emergency fund absorbs those hits so your other goals stay on track.

It gives you options. When you have savings, you can leave a toxic job without starving. You can take time to find the right mechanic instead of the cheapest one. You can negotiate medical bills because you have cash to offer. Money in the bank gives you the ability to make choices instead of being forced into corners.

Pro Tip: Think of your emergency fund as insurance you pay to yourself. Instead of paying an insurance company, you’re building a fund that you control, that earns interest, and that you’ll get back if you never need it.

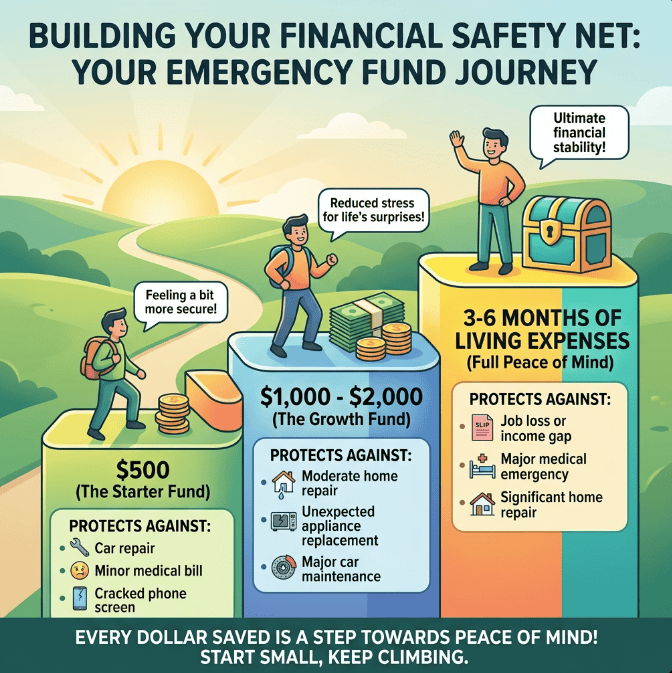

How Much Should You Save? (The Three Stages)

Financial experts love to throw around “3 to 6 months of expenses” as the goal for an emergency fund. And they’re right — eventually. But when you’re starting from zero, that number can feel so overwhelming that it paralyzes you into doing nothing.

That’s why I break it into three stages. Each stage is a milestone that provides real protection and real motivation to keep going.

Stage 1: The Starter Fund — $500

Your first goal is $500. That’s it. Five hundred dollars between you and financial disaster.

This amount won’t cover every possible emergency, but it handles the most common ones — a minor car repair, a doctor’s copay, a broken appliance, or an unexpected bill. According to the Federal Reserve, nearly 40% of Americans can’t cover an unexpected $400 expense without borrowing. By saving $500, you instantly put yourself ahead of almost half the country.

$500 is also psychologically powerful. It proves to yourself that you can save. For many people, reaching this milestone is the first time they’ve ever had money set aside for anything. That feeling of security — even a small amount — is genuinely life-changing.

Timeline: 1 to 3 months for most people.

Stage 2: The Solid Foundation — $1,000 to $2,000

Once you hit $500, push to $1,000. Then $2,000 if you can. This amount covers most real-world emergencies — a car repair, an ER visit with insurance, an emergency vet bill, or a month of essential expenses if your hours get cut at work.

$1,000 to $2,000 is also the sweet spot where you can start aggressively paying off debt without worrying that one bad week will undo everything. Many financial planners, including Dave Ramsey, recommend saving $1,000 first, then attacking debt with everything you have, then building the full emergency fund after.

Timeline: 3 to 6 months for most people.

Stage 3: The Full Emergency Fund — 3 to 6 Months of Expenses

This is the ultimate goal. Calculate your essential monthly expenses — housing, food, utilities, insurance, transportation, minimum debt payments — and multiply by 3 for a leaner fund or 6 for maximum security.

For a family spending $3,500 per month on essentials, the full emergency fund is $10,500 to $21,000. For a single person spending $2,000 per month, it’s $6,000 to $12,000.

This level of savings protects you from the big stuff — job loss, extended illness, major home repairs, or any financial disruption that takes months to recover from. It’s the difference between a tough situation and a financial catastrophe.

Timeline: 6 to 18 months for most people (after Stage 2).

Where to Keep Your Emergency Fund

Before you start saving, you need to decide where the money goes. This matters more than you might think.

The Best Option: A High-Yield Savings Account

A high-yield savings account (HYSA) is the ideal home for your emergency fund. It keeps your money safe, accessible when you need it, and earning interest while it sits there.

As of 2026, the best high-yield savings accounts offer 4% to 5% APY. That means a $10,000 emergency fund earns you $400 to $500 per year just for existing. That’s free money.

Good options include Marcus by Goldman Sachs, Ally Bank, Capital One 360, Discover Online Savings, and American Express High-Yield Savings. All of these are FDIC insured, meaning your money is protected up to $250,000 even if the bank fails.

The key feature of a HYSA for emergency funds is that it’s separate from your checking account. This separation creates a psychological barrier that prevents casual spending. The money is accessible — you can transfer it in 1 to 2 business days — but it’s not sitting in your checking account tempting you every time you check your balance.

Where NOT to Keep Your Emergency Fund

Not in your checking account. It will get spent. Guaranteed. When emergency money mixes with everyday spending money, boundaries disappear.

Not in a CD (Certificate of Deposit). CDs lock your money for a fixed period. Emergencies don’t wait for maturity dates. You need instant access.

Not in investments. The stock market can drop 20% in a month. If your car breaks down during a market crash, your $5,000 emergency fund might only be worth $4,000. Emergency funds need to be stable and predictable.

Not under your mattress. Cash at home doesn’t earn interest, can be lost to theft or fire, and is incredibly easy to dip into for non-emergencies.

Pro Tip: Name your savings account something specific like “Emergency Fund — Do Not Touch” or “Financial Safety Net.” Studies show that people who label their savings accounts with specific names are less likely to withdraw money for non-emergencies.

10 Ways to Find Money for Your Emergency Fund (Starting From Zero)

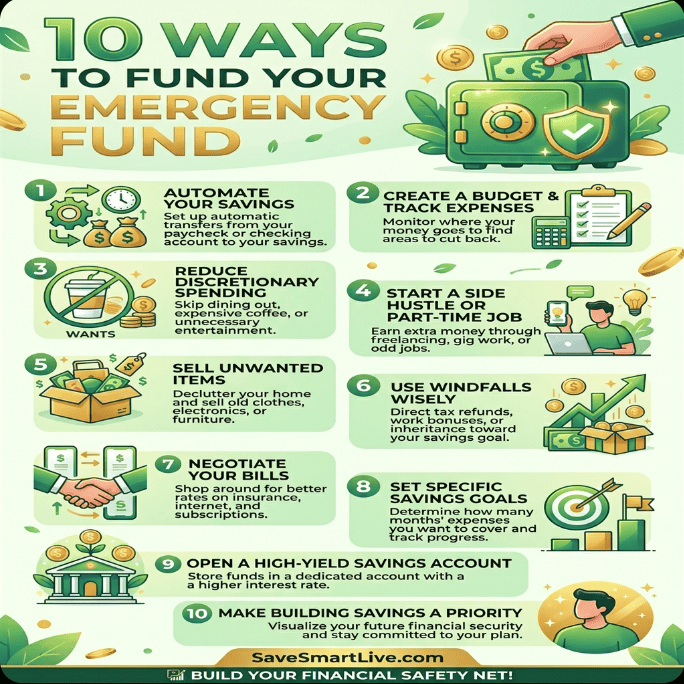

This is the part most guides skip. They tell you to “save more” without acknowledging that if you could easily save more, you already would be. When money is tight, finding extra dollars requires creativity and intentionality. Here are ten practical strategies that actually work.

1. Sell Things You Don’t Need

Walk through your house with fresh eyes. Every room has items you’ve forgotten about, outgrown, or replaced. Old phones, clothes that don’t fit, kitchen gadgets gathering dust, books you’ve read, exercise equipment you don’t use, toys your kids have outgrown.

List them on Facebook Marketplace, Mercari, Poshmark, or eBay. Most people can generate $200 to $1,000 in their first month of selling. That alone could fund your entire Stage 1 emergency fund.

2. Redirect One Expense

Pick one recurring expense you can temporarily eliminate or reduce, and redirect that exact amount to your emergency fund.

Cancel a streaming service you barely watch — $15/month. Switch to a cheaper phone plan — $30/month savings. Cut dining out from four times a month to two — $60/month saved. Pause your gym membership and work out at home — $40/month.

Even one change generates $15 to $60 per month that goes straight to your emergency fund. Stack two or three changes and you’re saving $50 to $150 monthly.

3. Use the 1% Method

Save 1% of your income this month. If you bring home $3,000, save $30. Next month, bump it to 2% ($60). Then 3% ($90).

The increases are so small they’re painless, but after 6 months at an average of 3.5%, you’re saving $105 per month on a $3,000 income — which means $630 saved in the first six months with virtually no lifestyle impact.

4. Save Your Tax Refund

The average American tax refund is about $3,000. If you receive a refund, commit right now — before it arrives — to putting at least half of it into your emergency fund.

It’s tempting to spend a tax refund on wants because it feels like “bonus money.” But it’s not bonus money. It’s your money that the government held for free all year. Using it to build financial security is one of the smartest things you can do.

5. Automate a Small Transfer on Payday

Set up an automatic transfer of $25 or $50 from your checking to your savings account on every payday. This is the single most effective savings strategy because it removes the need for willpower. The money moves before you see it, before you can spend it, before you can talk yourself out of it.

$25 per paycheck (biweekly) = $650 per year. $50 per paycheck = $1,300 per year. All automated. All painless.

6. Save All Unexpected Money

Any money that comes to you unexpectedly goes straight to the emergency fund. Birthday gifts, cash back rewards, rebate checks, refunds, bonuses, overtime pay, found money — all of it.

This rule is powerful because unexpected money isn’t part of your budget. You weren’t planning on it, so you won’t miss it. But your emergency fund will grow noticeably faster.

7. Do a No-Spend Weekend

One weekend per month, commit to spending absolutely nothing. Zero dollars from Friday evening to Sunday night. Cook with what’s already in your fridge and pantry. Find free entertainment — parks, hiking, library, game nights, movie marathons at home.

A typical American family spends $150 to $300 on an average weekend (dining out, entertainment, shopping, gas for outings). Even cutting that to $0 once a month and redirecting it to savings adds $1,800 to $3,600 per year.

8. Pick Up a Quick Side Hustle

Even a temporary side gig can fast-track your emergency fund. Deliver food for DoorDash for 5 hours on weekends and earn $75 to $125. Walk dogs through Rover for a few hours. Babysit for a neighbor’s date night.

You don’t have to commit to a long-term side hustle. Just earn enough to build your fund, then stop if you want to.

9. Use Cash Back and Reward Apps

Apps like Ibotta, Rakuten, Fetch Rewards, and Dosh give you cash back on purchases you’re already making. The amounts are small — $5 here, $10 there — but over a year, active users typically earn $100 to $300 in cash back.

Route all cash back earnings directly into your emergency fund. It’s found money that requires almost no extra effort.

10. Challenge Yourself With a Savings Game

Try the 52-week challenge (save $1 in week one, $2 in week two, etc. — total: $1,378), the $5 bill challenge (save every $5 bill you receive), or the round-up challenge (round every purchase up to the nearest dollar and save the difference).

These challenges gamify saving and make it genuinely fun. When saving feels like a game you’re winning rather than a sacrifice you’re enduring, you stick with it.

How to Protect Your Emergency Fund Once You Build It

Building the fund is step one. Keeping it intact is step two, and it’s just as important. Here’s how to make sure your hard work doesn’t disappear.

Define what counts as an emergency — in writing. Before you need the money, write down specific criteria. An emergency is unexpected, necessary, and urgent. A concert ticket is not an emergency. A car repair so you can get to work is.

Keep the fund in a separate account. If it’s in your checking account, you will spend it. A separate high-yield savings account — ideally at a different bank than your everyday checking — adds enough friction to prevent casual withdrawals.

Replenish it immediately after using it. If you dip into your emergency fund, your next financial priority is refilling it. Reduce spending on wants temporarily and direct that money back to the fund until it’s whole again.

Don’t invest your emergency fund. I know it’s tempting when you see your savings sitting there earning “only” 4% to 5%. But the stock market can crash 30% in a month. Your emergency fund’s job is not to grow aggressively — it’s to be there when you need it. Stability beats returns for this specific money.

Don’t feel guilty about using it for real emergencies. That’s literally what it’s for. If the roof leaks or you need emergency surgery, use the fund without hesitation or guilt. Then rebuild it. That’s the cycle.

Pro Tip: Once your emergency fund is fully built (3-6 months), stop contributing to it and redirect that money toward investing, retirement, or other goals. Don’t keep piling money into an emergency fund beyond 6 months of expenses — at that point, it’s more productive invested elsewhere.

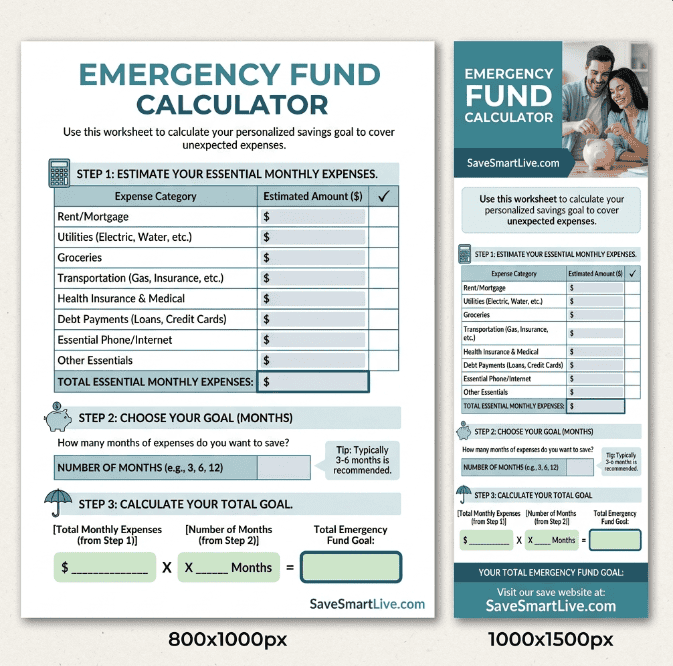

Emergency Fund Calculator: How Much Do You Actually Need?

Here’s a simple way to calculate your personal emergency fund target.

List your essential monthly expenses only:

- Rent or mortgage: $________

- Utilities (electric, water, gas, internet): $________

- Groceries (not dining out): $________

- Transportation (car payment, gas, insurance, transit): $________

- Health insurance premium: $________

- Minimum debt payments: $________

- Phone bill: $________

- Childcare (if applicable): $________

- Any other non-negotiable expenses: $________

Total Essential Monthly Expenses: $________

Now multiply:

- × 3 months = your minimum emergency fund target

- × 6 months = your comfortable emergency fund target

Example: If your essential monthly expenses total $2,800: - 3-month fund = $8,400

- 6-month fund = $16,800

Notice that this calculation uses essential expenses only, not your total monthly spending. You wouldn’t maintain your entertainment budget, shopping habits, or dining-out frequency during a financial emergency. You’d cut to essentials. So your fund only needs to cover essentials.

start an emergency fund from zero

start an emergency fund from zero

The Biggest Mistakes People Make With Emergency Funds

Starting too big. If someone tells you to save $15,000 and you currently have $0, that feels impossible and you never start. Start with $500. Then $1,000. Then keep going. Small wins create momentum.

Using it for non-emergencies. A sale at Target is not an emergency. A vacation is not an emergency. Your friend’s wedding is not an emergency (you knew about it months ago). Protect this fund with clear rules.

Not starting because “it’s not worth it.” I’ve heard people say “what’s the point of saving $25 a month?” The point is that $25 per month is $300 per year, and $300 can cover a flat tire, a doctor’s visit, or a plumbing bill that would otherwise go on a credit card. Small amounts matter enormously.

Keeping it too accessible. If your emergency fund is in the same bank account you use for daily spending, it will slowly drain. Separate accounts at separate banks are ideal.

Giving up after one withdrawal. You’ll use your emergency fund at some point. That’s the whole purpose. Don’t see a withdrawal as a failure. See it as the fund doing its job perfectly. Rebuild it and move on.

Frequently Asked Questions

Should I save an emergency fund or pay off debt first?

Save a starter emergency fund of $500 to $1,000 first, then attack debt aggressively. The reason is simple — without any savings, every unexpected expense goes onto a credit card, adding more debt. The starter fund breaks that cycle and gives you breathing room to focus on debt payoff.

How long does it take to build an emergency fund?

It depends on your income, expenses, and how aggressively you save. A $1,000 starter fund typically takes 2 to 4 months. A full 3-6 month fund takes 6 to 18 months for most people. The timeline doesn’t matter as much as the consistency.

Where should I keep my emergency fund?

A high-yield savings account is the best option. It keeps your money safe, accessible, and earning interest (4-5% APY currently). Keep it separate from your checking account to reduce temptation.

Is $1,000 enough for an emergency fund?

$1,000 is a great starting point and covers most common emergencies. However, it won’t cover major events like job loss or serious medical bills. Once you’ve paid off high-interest debt, build toward 3-6 months of essential expenses for full protection.

What if I can barely afford my bills — how do I save anything?

Start with literally any amount you can. $5 per week. $10 per paycheck. One dollar a day. Use strategies like selling unused items, cutting one subscription, or using cash back apps. The amount matters less than the habit. Once saving becomes automatic, you’ll naturally find ways to increase the amount over time.

Should my emergency fund be in cash or a bank account?

A bank account, specifically a high-yield savings account. Cash at home earns no interest, can be lost or stolen, and is too easy to spend. A savings account earns interest, is FDIC insured up to $250,000, and adds just enough friction to prevent impulsive withdrawals.

Can I use my emergency fund to invest?

No. Emergency funds and investment portfolios serve completely different purposes. Your emergency fund needs to be stable, liquid, and immediately accessible. Investments can lose value in the short term. Keep them separate.

Your Emergency Fund Journey Starts With One Dollar

Your Emergency Fund Journey Starts With One Dollar

I know this article threw a lot of numbers and strategies at you. So let me simplify everything into one sentence.

Save one dollar today.

That’s it. That’s the whole first step. One single dollar moved from your checking account to a savings account. Or one dollar bill put into a jar on your kitchen counter.

Tomorrow, save another dollar. The day after that, another one. In a week, you’ll have $7. In a month, $30. It’s not much, but it’s infinitely more than $0. And more importantly, you’ll have proven to yourself that you can do this.

The journey from $0 to $500 is the hardest part. The journey from $500 to $1,000 feels easier because you already have momentum. And the journey from $1,000 to a full 3-6 month emergency fund feels almost inevitable because by that point, saving is just what you do.

You deserve the peace of mind that comes with knowing you’re prepared. You deserve to sleep soundly on a Tuesday night, knowing that whatever tomorrow throws at you, you can handle it.

Start with one dollar. The rest will follow.

Found this helpful? Save it to your Pinterest for later and share it with someone who’s starting their savings journey. For more money-saving tips and strategies, visit SaveSmartLive.com.

Related articles:

- How to Create a Monthly Budget That Actually Works (2026 Guide)

- 15 Money Saving Challenges to Try in 2026

- Debt Snowball vs Debt Avalanche: Which Is Better?

- 50/30/20 Budget Rule Explained (With Free Template)

Read More : How to Create a Monthly Budget That Actually Works (2026 Guide)