How to Create a Monthly Budget That Actually Works

How to Create a Monthly Budget That Actually Works (2026 Guide)

Are you tired of running out of money before the month ends? Do you feel like no matter how hard you try, your paycheck just disappears? You are not alone. According to recent studies, nearly 60% of Americans live paycheck to paycheck — and most of them don’t have a working monthly budget.

Here’s the thing: creating a budget is not about restricting yourself. It’s about telling your money where to go instead of wondering where it went. A solid monthly budget gives you control, reduces stress, and helps you reach your financial goals faster than you ever thought possible.

In this complete guide, you will learn exactly how to create a monthly budget from scratch — even if you’ve never budgeted before. We’ll walk through every step, cover the most popular budgeting methods, and give you practical tips that work in real life, not just on paper.

Whether you earn $2,000 or $10,000 a month, this guide will help you take control of your money starting today.

What Is a Monthly Budget and Why Do You Need One?

A monthly budget is a simple plan that tracks how much money comes in and how much money goes out every single month. It breaks your income into categories like housing, food, transportation, savings, and entertainment — so you always know exactly where your dollars are going.

But why does this matter? Let’s be honest. Most people think they know where their money goes. But when you actually sit down and track it, the results can be shocking. That daily coffee habit? It could be costing you $150 a month. Those subscription services you forgot about? Another $50 to $100 slipping away quietly.

A budget helps you see the full picture. And once you see it, you can change it.

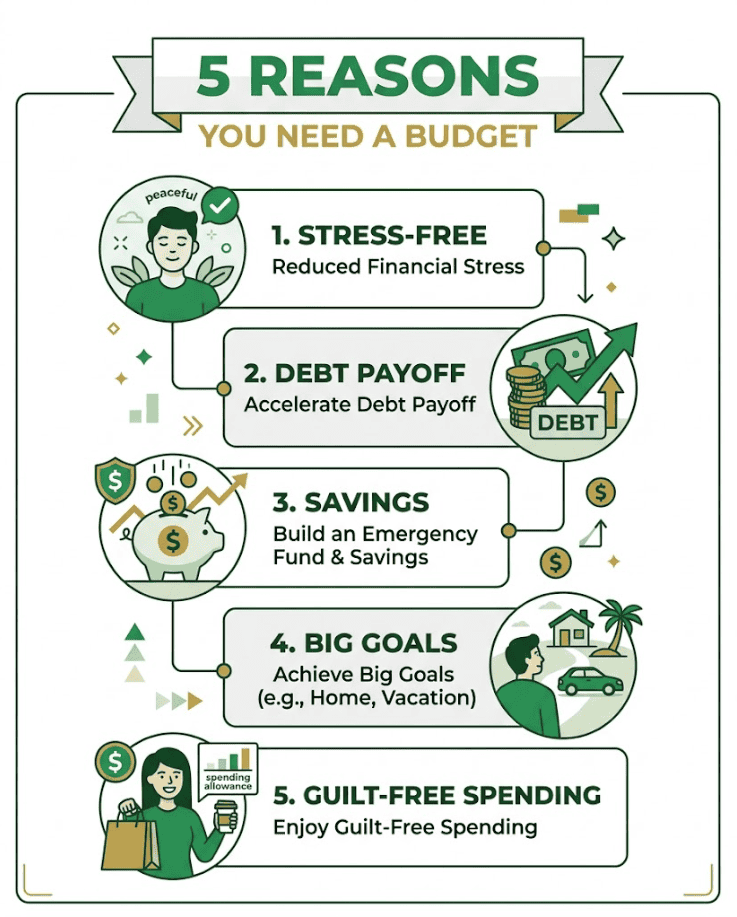

Here are some powerful reasons why you need a monthly budget:

It reduces financial stress. When you know exactly how much you can spend on groceries, gas, and fun stuff, you stop worrying. There are no more surprises at the end of the month.

It helps you pay off debt faster. A budget shows you where you can cut expenses and redirect that money toward paying down credit cards, student loans, or medical bills.

It builds your savings automatically. When saving money is a line item in your budget — not an afterthought — it actually happens. Consistently.

It helps you reach big goals. Want to buy a house? Take a vacation? Retire early? A budget is your roadmap to get there.

It gives you permission to spend. This one surprises people. When you budget $200 for entertainment, you can actually enjoy spending that $200 guilt-free because you know everything else is covered. Step 1: Calculate Your Total Monthly Income

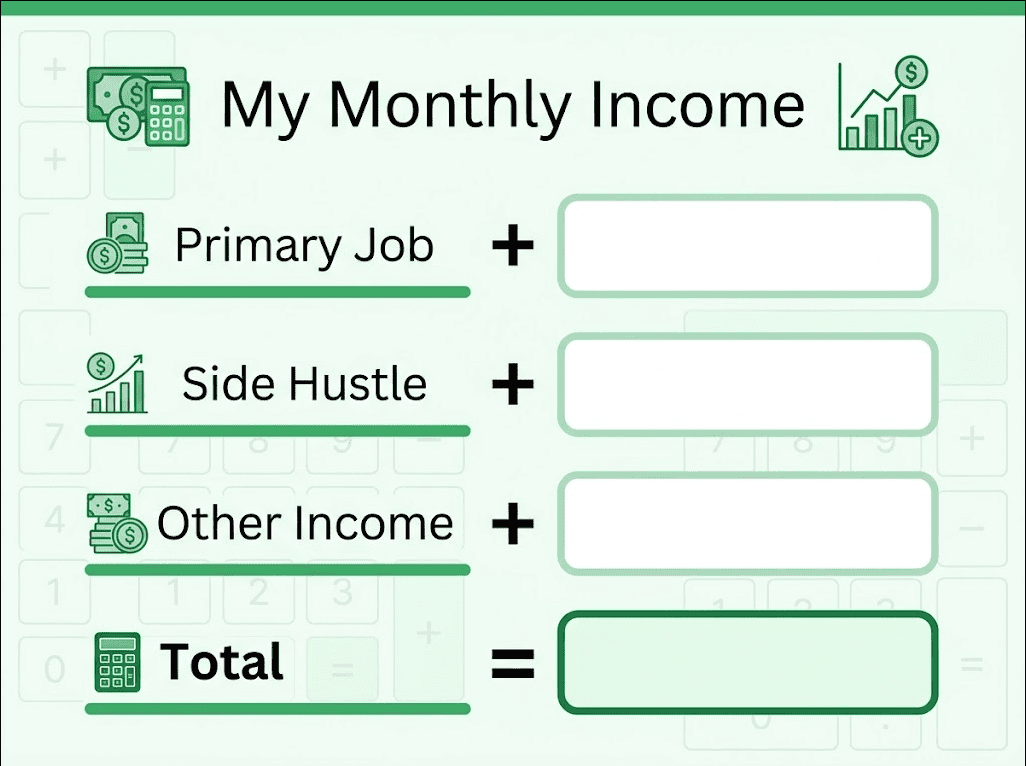

Step 1: Calculate Your Total Monthly Income

Before you can tell your money where to go, you need to know exactly how much money you have coming in each month. This is your starting point, and getting it right is crucial.

Your total monthly income includes everything you earn after taxes. This is your net income — the amount that actually hits your bank account, not your gross salary.

Here is what to include when calculating your monthly income:

Your primary paycheck. If you get paid biweekly, multiply your paycheck by 2 for most months. If you get paid weekly, multiply by 4. For salaried employees paid monthly, this is straightforward.

Side hustle income. Do you drive for Uber, freelance on the weekends, sell items online, or do any other side work? Include the average monthly amount you earn from these activities.

Other income sources. This could include child support, alimony, rental income, investment dividends, government benefits, or any other regular money coming in.

Irregular income tip: If your income varies month to month (freelancers, gig workers, commission-based jobs), use the average of your last 3 months of income. Or better yet, budget based on your lowest recent month — this keeps you safe and anything extra becomes a bonus.

Let’s look at a simple example:

Sarah’s Monthly Income Breakdown:

- Primary job (after taxes): $3,200

- Weekend freelance writing: $400

- Etsy shop sales (average): $150

- Total Monthly Income: $3,750

Write down your total monthly income right now. This number is the foundation of your entire budget.

How to Create a Monthly Budget That Actually Works

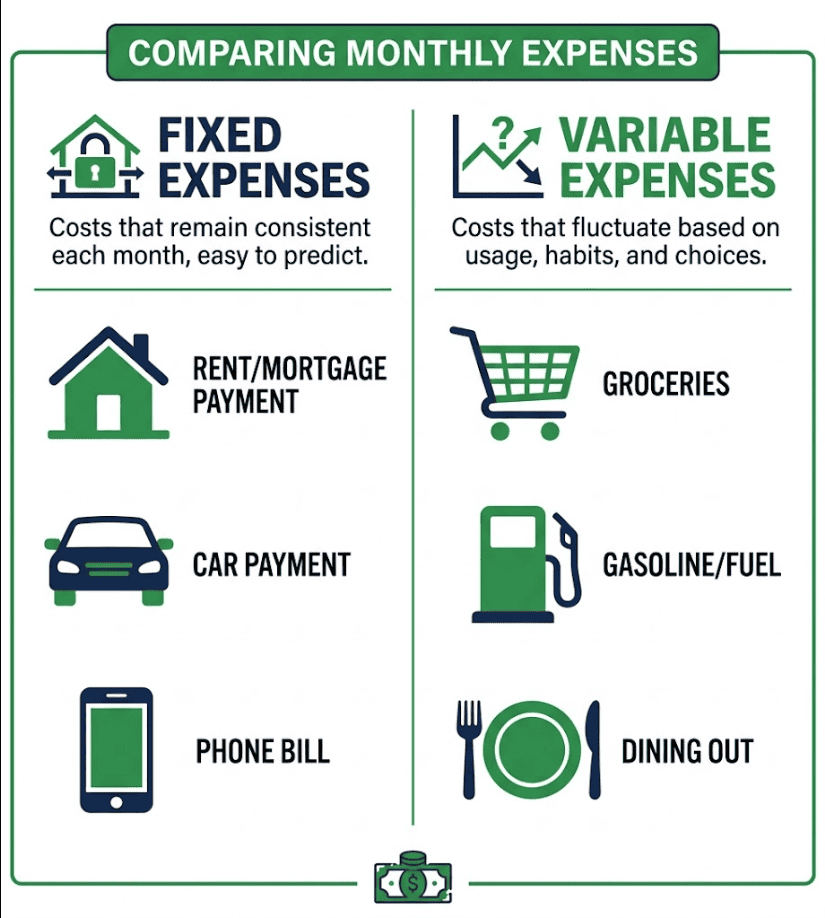

Step 2: List All Your Monthly Expenses

Now comes the part that opens most people’s eyes. You need to write down every single thing you spend money on in a typical month. And I mean everything — from your rent to that $1.50 vending machine snack.

There are two types of expenses you need to track:

Fixed Expenses (Same Every Month)

These are bills that stay roughly the same amount each month. They are predictable and easier to plan for.

Common fixed expenses include:

- Rent or mortgage payment

- Car payment

- Car insurance

- Health insurance

- Life insurance

- Internet and phone bill

- Streaming subscriptions (Netflix, Spotify, etc.)

- Gym membership

- Student loan payment

- Minimum credit card payments

- Child care costs

- Any other recurring monthly bills

Variable Expenses (Change Every Month)

These expenses fluctuate from month to month. They are harder to predict but usually offer the most opportunity for savings.

Common variable expenses include:

- Groceries and household supplies

- Gas and transportation

- Electricity and water bills

- Dining out and takeout

- Coffee shops

- Clothing and personal care

- Entertainment and hobbies

- Gifts and celebrations

- Home maintenance and repairs

- Medical expenses and prescriptions

- Pet expenses

- Miscellaneous spending

Pro tip: Go through your last 3 months of bank statements and credit card statements. Highlight every transaction and assign it to a category. This exercise alone can be life-changing because you will see spending patterns you never noticed before.

Many people discover they are spending $300 to $500 more per month than they realized — often on small, forgettable purchases that add up quickly.

How to Create a Monthly Budget That Actually Works

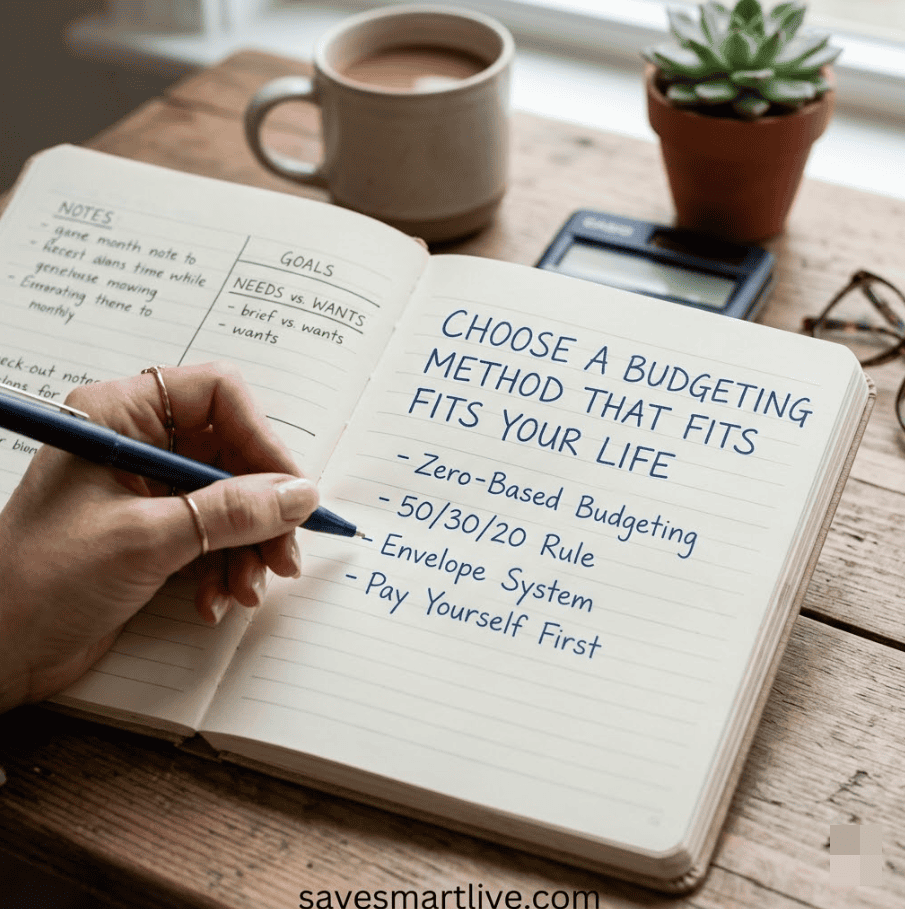

Step 3: Choose a Budgeting Method That Fits Your Life

Here is where most budgeting guides get it wrong. They tell you there is only one way to budget. The truth is, there are several proven methods, and the best one is the one you will actually stick with.

Let me walk you through the four most popular budgeting methods so you can pick the one that matches your personality and financial situation.

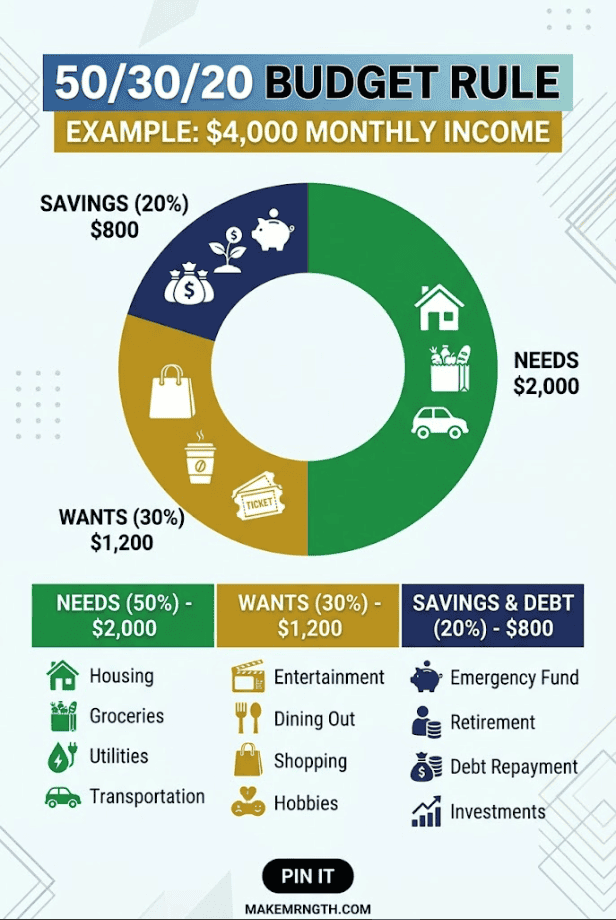

Method 1: The 50/30/20 Budget Rule

This is the most popular budgeting method for beginners because it is simple and flexible. It was popularized by Senator Elizabeth Warren in her book “All Your Worth.”

Here is how it works:

50% of your income goes to Needs. These are things you absolutely must pay for — housing, utilities, groceries, insurance, minimum debt payments, transportation.

30% of your income goes to Wants. These are things you enjoy but could live without — dining out, entertainment, shopping, vacations, subscriptions.

20% of your income goes to Savings and Debt. This includes your emergency fund, retirement contributions, extra debt payments, and other financial goals.

Example with $4,000 monthly income:

- Needs (50%): $2,000

- Wants (30%): $1,200

- Savings/Debt (20%): $800

Best for: People who want a simple framework without tracking every single dollar. Great for beginners.

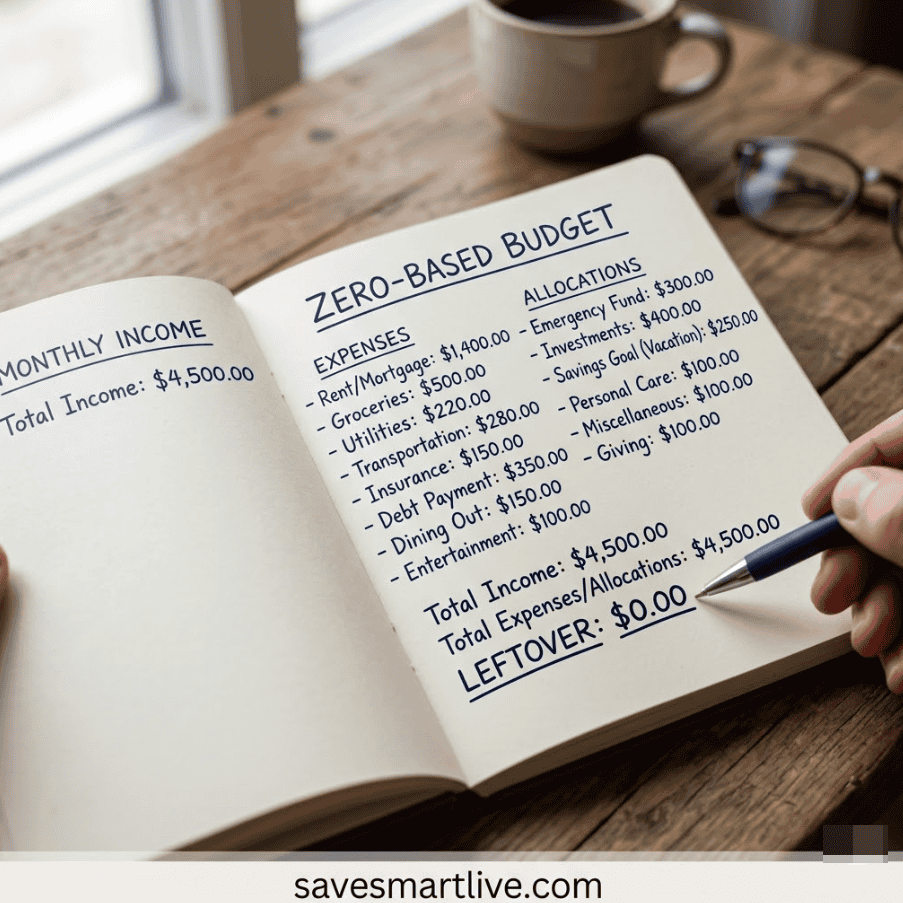

Method 2: Zero-Based Budget

With a zero-based budget, you assign every single dollar a job. Your income minus your expenses should equal exactly zero. This does not mean you spend everything — it means every dollar is accounted for, including savings.

Here is how it works:

Start with your total income at the top. Then subtract each expense category one by one until you reach zero. If you have $200 left over after all expenses, you assign that $200 to a specific category — maybe extra savings, debt payoff, or next month’s expenses.

Example:

- Income: $3,500

- Rent: -$1,200

- Utilities: -$200

- Groceries: -$400

- Gas: -$150

- Insurance: -$250

- Dining out: -$100

- Entertainment: -$75

- Savings: -$300

- Debt payoff: -$500

- Miscellaneous: -$125

- Clothing: -$100

- Personal care: -$50

- Phone: -$50

- Remaining: $0

Every dollar has a purpose. Nothing is left unassigned.

Best for: People who want complete control over their money and don’t mind spending a little more time on their budget each month.

Method 3: The Envelope System

The envelope system is a cash-based budgeting method that makes overspending physically impossible. It was made famous by financial guru Dave Ramsey.

Here is how it works:

You create physical envelopes for each spending category (groceries, gas, dining out, entertainment, etc.). At the beginning of the month, you put the budgeted cash amount in each envelope. When an envelope is empty, you stop spending in that category. Period.

Example envelopes:

- Groceries: $400 cash

- Gas: $150 cash

- Dining out: $100 cash

- Entertainment: $75 cash

- Personal spending: $50 cash

Best for: People who struggle with overspending, especially on credit cards. The physical act of handing over cash makes you think twice about every purchase.

Method 4: Pay Yourself First

This method flips traditional budgeting upside down. Instead of budgeting expenses first and saving what is left over, you save first and spend what is left over.

Here is how it works:

The moment your paycheck arrives, you immediately transfer a set percentage (usually 20% or more) to savings and investments. Then you pay your fixed bills. Whatever remains is yours to spend however you want on variable expenses.

Best for: People who are good at managing day-to-day expenses but struggle to save consistently. This method makes saving automatic and non-negotiable.

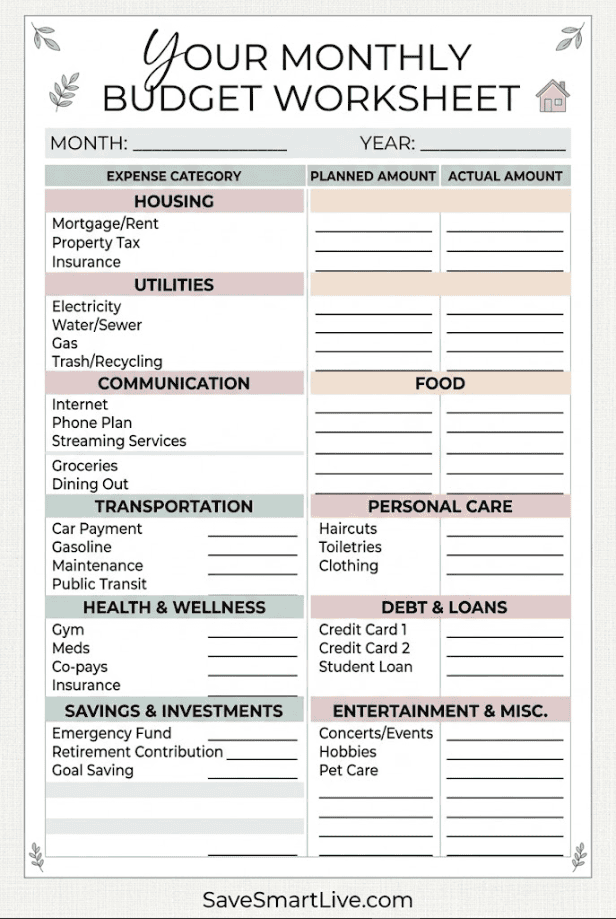

Step 4: Set Up Your Budget (Template Included)

Now that you have picked your method, it is time to actually build your budget. You can do this with pen and paper, a spreadsheet, or a budgeting app. Here is a simple template you can follow regardless of which method you chose.

Your Monthly Budget Template

Income Section:

- Primary job income: $______

- Side hustle income: $______

- Other income: $______

- Total Income: $______

Fixed Expenses:

- Housing (rent/mortgage): $______

- Car payment: $______

- Insurance (auto/health/life): $______

- Phone bill: $______

- Internet: $______

- Subscriptions: $______

- Minimum debt payments: $______

- Child care: $______

- Total Fixed Expenses: $______

Variable Expenses:

- Groceries: $______

- Gas/Transportation: $______

- Utilities (electric/water/gas): $______

- Dining out: $______

- Entertainment: $______

- Clothing: $______

- Personal care: $______

- Household supplies: $______

- Miscellaneous: $______

- Total Variable Expenses: $______

Financial Goals:

- Emergency fund: $______

- Retirement savings: $______

- Extra debt payoff: $______

- Vacation fund: $______

- Other savings goals: $______

- Total Savings: $______

The Math:

- Total Income: $______

- Minus Total Fixed Expenses: $______

- Minus Total Variable Expenses: $______

- Minus Total Savings: $______

- = Remaining: $______ (should be $0 for zero-based budget)

Step 5: Track Your Spending Daily

Step 5: Track Your Spending Daily

Creating a budget is only half the battle. The magic happens when you actually track your spending against your budget throughout the month. Without tracking, your budget is just a wish list.

Here are the best ways to track your daily spending:

Option 1: Budgeting Apps (Easiest)

Modern budgeting apps connect to your bank accounts and automatically categorize your transactions. They show you in real-time how much you have left in each category.

Best free budgeting apps in 2026:

EveryDollar — Built by Dave Ramsey’s team. Simple, clean interface. Perfect for zero-based budgeting. Free version available.

Mint (Credit Karma) — Automatically tracks and categorizes spending. Good for people who want a hands-off approach. Completely free.

YNAB (You Need A Budget) — The gold standard of budgeting apps. Uses the zero-based method. Costs $14.99/month but many users say it saves them $600+ per month. Free 34-day trial available.

Goodbudget — Digital version of the envelope system. Great for couples who want to share envelopes. Free version with limited envelopes.

PocketGuard — Shows you exactly how much you have available to spend after bills and savings goals. Very beginner-friendly. Free version available.

Option 2: Spreadsheet (Most Customizable)

If you prefer more control, a Google Sheets or Excel spreadsheet lets you customize everything. You can create tabs for each month, add charts to visualize your spending, and adjust categories to match your exact needs.

Option 3: Pen and Paper (Most Intentional)

There is something powerful about physically writing down every purchase. Studies show that people who write down their spending are more aware of their habits and tend to spend less. A simple notebook works perfectly.

Whichever method you choose, the key is consistency. Try to update your budget tracker every evening. It takes less than 5 minutes and keeps you accountable.

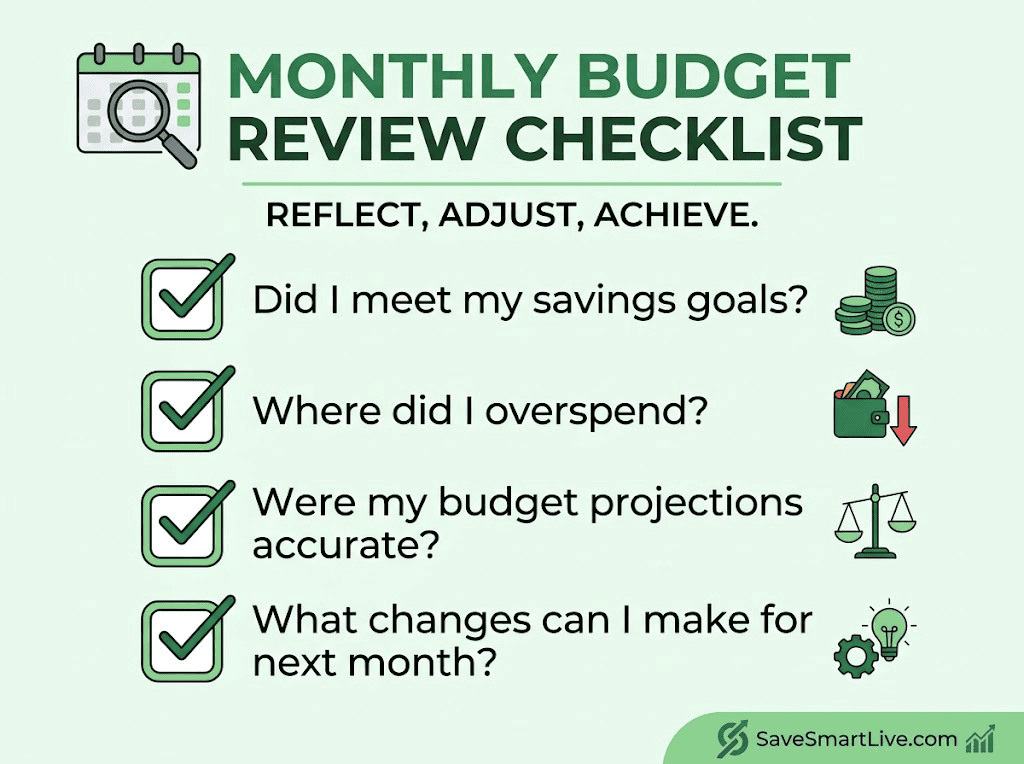

Step 6: Adjust and Optimize Every Month

Step 6: Adjust and Optimize Every Month

Your first budget will not be perfect. That is completely normal. Budgeting is a skill, and like any skill, it gets better with practice.

At the end of each month, sit down and review your budget. Ask yourself these questions:

Did I overspend in any category? If you budgeted $400 for groceries but spent $500, figure out why. Were prices higher than expected? Did you eat out less and buy more groceries? Adjust the numbers for next month.

Did I underspend in any category? If you budgeted $200 for gas but only spent $120, that is great! You can redirect that extra $80 toward savings or debt payoff.

Are there expenses I can eliminate? Look for subscriptions you are not using, memberships you forgot about, or habits that are costing more than they are worth.

Am I making progress toward my goals? Check your savings account balance, your debt balances, and your overall net worth. Are the numbers moving in the right direction?

The golden rule of budgeting: Give yourself grace during the first 3 months. It typically takes about 90 days to dial in a budget that truly works for your lifestyle. Do not give up if month one is messy. Keep going.

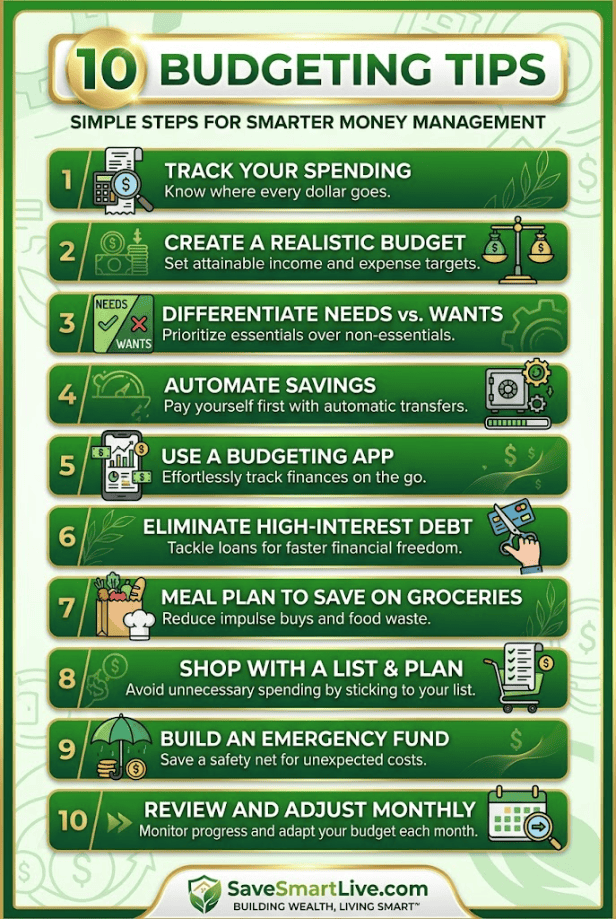

10 Budgeting Tips That Make a Real Difference

10 Budgeting Tips That Make a Real Difference

After years of studying personal finance and talking to people who have successfully transformed their finances, here are the budgeting tips that consistently make the biggest impact:

Tip 1: Use the 24-hour rule for non-essential purchases. Before buying anything over $50 that you did not plan for, wait 24 hours. If you still want it the next day, buy it. This simple habit can save you hundreds of dollars every month by eliminating impulse purchases.

Tip 2: Round up your bills. If your electric bill is $87, budget $100. If your groceries are usually $380, budget $400. The extra money adds up in a buffer fund that protects you from small overages.

Tip 3: Automate your savings. Set up an automatic transfer from your checking account to your savings account on payday. When saving is automatic, you never have to rely on willpower.

Tip 4: Use cash for problem categories. If you always overspend on dining out or entertainment, switch to cash for those categories only. When the cash is gone, you are done for the month.

Tip 5: Plan your meals before you grocery shop. Meal planning is the single most effective way to reduce your food budget. When you know exactly what you need, you buy less and waste less.

Tip 6: Review your subscriptions quarterly. Set a reminder every 3 months to review all your recurring charges. Cancel anything you have not used in the past 30 days.

Tip 7: Budget for fun. Seriously. If your budget has zero room for enjoyment, you will abandon it within weeks. A sustainable budget includes money for things you love — whether that is date nights, hobbies, or a monthly treat.

Tip 8: Use “sinking funds” for irregular expenses. Car repairs, holiday gifts, back-to-school supplies, and annual subscriptions are predictable but irregular. Create separate savings categories for these expenses and contribute small amounts each month so you are never caught off guard.

Tip 9: Have a budget meeting with your partner. If you share finances with a spouse or partner, schedule a weekly or monthly “money date” to review the budget together. This keeps both people accountable and avoids money arguments.

Tip 10: Celebrate your wins. Paid off a credit card? Hit a savings milestone? Stayed under budget for the whole month? Celebrate it! Positive reinforcement keeps you motivated for the long haul.

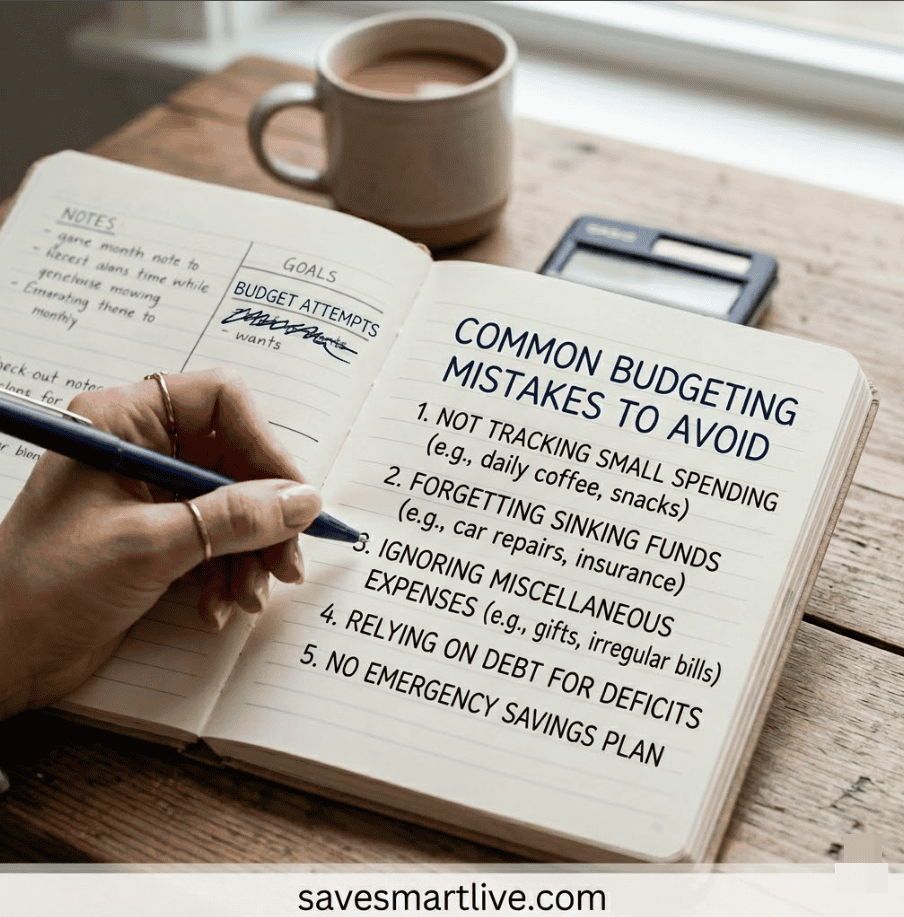

Common Budgeting Mistakes to Avoid

Common Budgeting Mistakes to Avoid

Even experienced budgeters make mistakes. Here are the most common ones so you can avoid them from the start:

Not including irregular expenses. Things like car registration, holiday gifts, and annual insurance premiums are easy to forget. Build them into your budget using sinking funds.

Making the budget too restrictive. If you cut every fun expense to zero, you are setting yourself up for failure. A good budget is realistic, not punishing.

Not budgeting for emergencies. Unexpected expenses will happen. Budget a small amount each month for your emergency fund — even $50 is a start.

Giving up after one bad month. One month of overspending does not mean budgeting does not work. It means you are human. Review what went wrong, adjust, and try again.

Not involving your partner. If you share expenses with someone, both people need to be involved in the budget. One-sided budgeting leads to resentment and failure.

Forgetting about irregular income. If you receive bonuses, tax refunds, or unexpected money, have a plan for it in advance. A good rule is 50% toward financial goals and 50% toward wants.

Frequently Asked Questions About Monthly Budgeting

How much should I save each month?

Financial experts generally recommend saving at least 20% of your after-tax income. However, if that feels impossible right now, start wherever you can — even 5% or 10% is better than nothing. The most important thing is to start and then increase gradually.

What if my income changes every month?

If you have irregular income, budget based on your lowest earning month from the past 3 to 6 months. This ensures you can always cover your essentials. In months when you earn more, put the extra toward savings and debt.

What is the best budgeting app for beginners?

For most beginners, EveryDollar or Mint are great starting points because they are free and easy to use. If you want more detailed tracking and are willing to invest in a tool, YNAB is considered the gold standard in budgeting apps.

How often should I update my budget?

Review your budget at least once a week to track spending and once at the end of each month to make adjustments for the next month. Many successful budgeters check their budget daily — it takes less than 2 minutes.

Should I use cash or cards for budgeting?

Both work, but they serve different purposes. Cards are more convenient and easier to track digitally. Cash is better for controlling spending in problem categories because it creates a physical limit. Many people use a combination — cards for fixed bills and cash for variable expenses.

What if I have debt? Should I budget for savings too?

Yes. Even if you are paying off debt, try to save at least a small emergency fund of $500 to $1,000 first. This prevents you from going deeper into debt when unexpected expenses arise. After that, focus aggressively on debt payoff.

Can budgeting really help me save money?

Absolutely. Studies show that people who follow a monthly budget save 15% to 20% more than those who do not. A budget does not magically create more money, but it shows you exactly where your money is leaking — and those leaks are usually bigger than you think.

Your Next Steps: Start Your Budget Today

You now have everything you need to create a monthly budget that actually works. Let me recap the key steps:

- Calculate your total monthly income — know exactly what you are working with.

- List every expense — go through bank statements, find the leaks.

- Choose your budgeting method — 50/30/20, zero-based, envelope, or pay yourself first.

- Set up your budget — use the template above or a budgeting app.

- Track your spending daily — consistency is the secret ingredient.

- Review and adjust monthly — your budget is a living document, not a stone tablet.

The hardest part is not creating the budget — it is starting. So here is my challenge to you: Take 30 minutes today and complete Steps 1 and 2. Just calculate your income and list your expenses. That is it. Once you see the numbers in front of you, the motivation to keep going will kick in naturally.

Remember, budgeting is not about perfection. It is about progress. Even a rough budget is infinitely better than no budget at all.

Your future self will thank you for starting today.

Did you find this guide helpful? Share it with someone who needs to hear this, and save it to your Pinterest board for later! For more practical money tips, budgeting strategies, and saving hacks, explore our other guides on SaveSmartLive.com.

Related articles you might enjoy:

- 15 Money Saving Challenges to Try in 2026

- 50/30/20 Budget Rule Explained (With Free Template)

- How to Start an Emergency Fund From Zero

Read more : How to Improve Your Credit Score Fast: 7 Proven Steps That Actually Work