15 Money Saving Challenges

Let me tell you something I wish someone told me five years ago. I used to think saving money meant putting away whatever was “left over” at the end of the month. Spoiler alert — there was never anything left over. Not once. Every single month, I would look at my bank account and wonder where it all went.

Then I stumbled onto something called a savings challenge. It sounded almost too simple — follow a set plan, save specific amounts on specific days, and watch the money pile up. I figured I had nothing to lose, so I tried the 52-week challenge. By December, I had saved over $1,300 without even feeling it.

That experience changed how I think about money. Saving doesn’t have to be painful. It doesn’t require a massive paycheck or some complicated financial strategy. Sometimes, all you need is a fun challenge that tricks your brain into building a habit.

So if you’ve been struggling to save, or if you just want a fresh approach for 2026, this list is for you. I’ve put together 15 money saving challenges that range from super easy to genuinely aggressive — so no matter where you are financially, there’s something here that fits.Why Savings Challenges Work Better Than “Just Saving More”

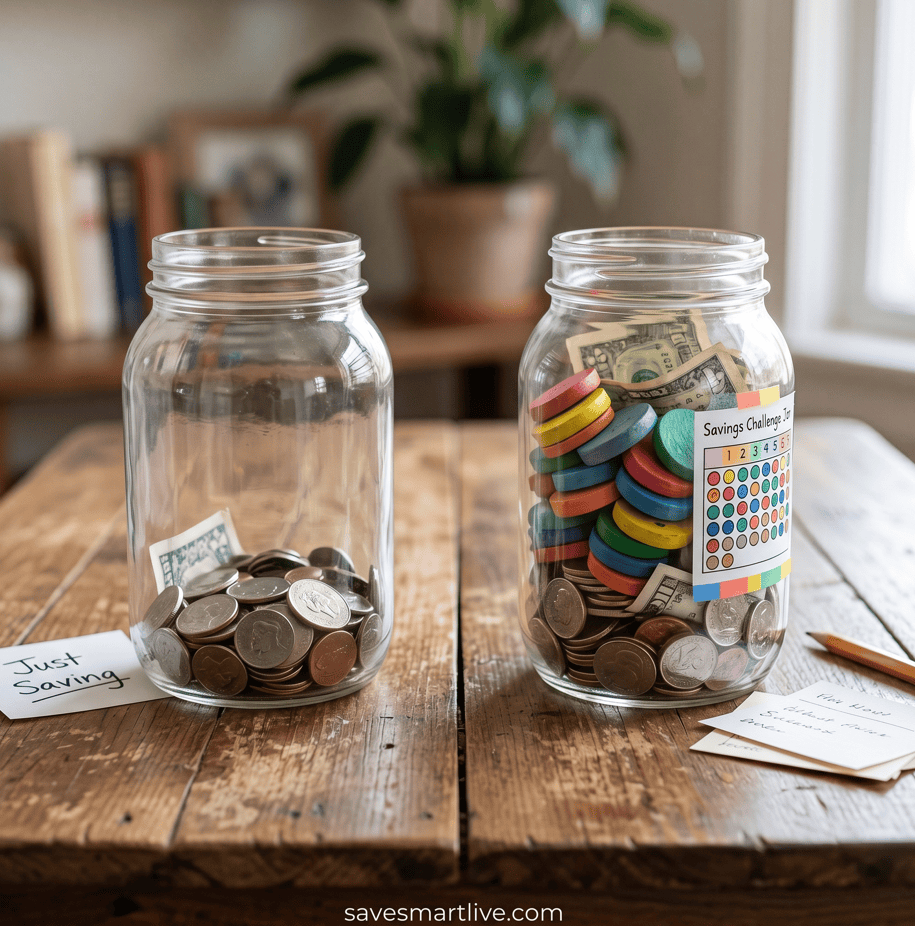

Before we get into the challenges, let’s talk about why this approach works when everything else hasn’t.

The problem with telling yourself “I’ll save more this month” is that it’s vague. There’s no structure, no specific amount, no accountability. It’s like saying “I’ll eat healthier” — it sounds nice but rarely leads to action.

Savings challenges work because they give you three things your brain craves.

First, they give you a clear target. You know exactly how much to save and when. There’s no guessing, no decision fatigue. You just follow the plan.

Second, they create momentum. Most challenges start small — sometimes as little as a dollar or even a penny. That low barrier makes it easy to start, and once you start seeing your savings grow, motivation kicks in naturally. You don’t want to break the streak.

Third, they make it feel like a game. Let’s be honest, budgeting can feel boring. But when you turn saving into a challenge — especially when you can track your progress visually with a chart or printable — it activates the same part of your brain that enjoys completing levels in a video game. You want to finish. You want to win.

That’s why millions of people swear by savings challenges. They take something that normally feels like deprivation and turn it into something that actually feels rewarding.

The 15 Best Money Saving Challenges for 2026

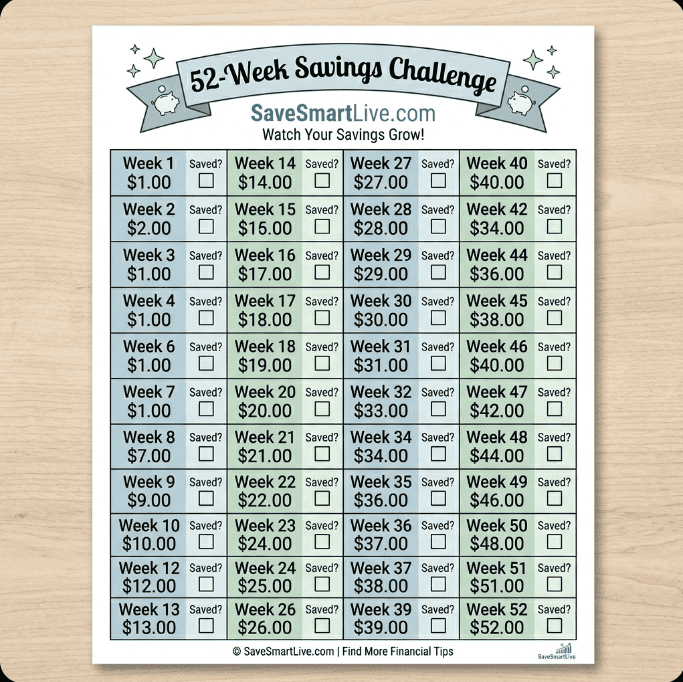

Challenge 1: The Classic 52-Week Money Challenge

This is the one that started it all for most people, and it’s still one of the best.

Here’s how it works. In week one, you save $1. In week two, you save $2. In week three, $3. You keep increasing by one dollar each week until week 52, when you save $52.

By the end of the year, you’ll have saved exactly $1,378.

What makes this challenge so effective is how gently it starts. Saving $1 in January is effortless. By the time the amounts get larger in November and December, you’ve already built the habit and the motivation to keep going.

One tip that makes this even easier — do the challenge in reverse. Start with $52 in week one when your New Year motivation is high, and work your way down to $1 by December when holiday expenses are eating into your budget. Same total savings, much easier finish.

Pro Tip: Print out a 52-week tracker and put it on your fridge. Crossing off each week is surprisingly satisfying and keeps the challenge visible.

Total saved: $1,378

15 Money Saving Challenges

Challenge 2: The $5 Bill Challenge

This one requires zero planning and zero math. Every time a $5 bill lands in your hands — whether from change at a store, a friend paying you back, or an ATM withdrawal — you don’t spend it. You put it in a jar or envelope immediately.

That’s it. No schedule, no chart, no tracking needed.

Most people who try this save between $500 and $1,500 per year depending on how often they use cash. It works because you barely notice $5 leaving your wallet, but over months, those bills stack up surprisingly fast.

The key is having a dedicated place for your $5 bills. A jar on your dresser, an envelope in a drawer, even a small safe. If you can see the pile growing, you’ll be even more motivated to keep going.

Total saved: $500-$1,500 per year (varies)

15 Money Saving Challenges

Challenge 3: The No-Spend Challenge (7, 14, or 30 Days)

This challenge is intense but incredibly eye-opening. You pick a timeframe — one week, two weeks, or a full month — and you commit to spending money only on absolute necessities. That means groceries, bills, gas, and medicine. Everything else is off limits.

No dining out. No coffee shops. No Amazon orders. No Target runs “just to browse.” No subscriptions you could pause.

The first few days feel uncomfortable, I won’t lie. But something interesting happens around day four or five. You stop thinking about spending. You start getting creative with what you already have. You cook meals from the back of your pantry. You find free entertainment. You realize how many of your purchases were driven by boredom or habit, not actual need.

Most people who complete a 30-day no-spend challenge save anywhere from $300 to $800 — and many of them permanently change their spending habits afterward because they finally see how much of their spending was mindless.

Start with a 7-day challenge if a full month feels too extreme. Even one week of intentional non-spending will open your eyes.

Pro Tip: Before starting, make a list of “approved expenses” so you’re clear on what counts as necessary. Gray areas lead to cheating.

Total saved: $300-$800 per month

Challenge 4: The Round-Up Challenge

Every time you make a purchase, round up to the nearest dollar and save the difference.

Buy a coffee for $4.37? Round up to $5 and save $0.63. Gas costs $42.18? Save $0.82. Grocery bill is $87.54? Save $0.46.

These amounts are so small you’ll never miss them, but over hundreds of transactions per year, they add up to real money. Most people save between $300 and $600 annually with the round-up method.

Several banking apps and fintech tools do this automatically now. Acorns, Chime, and Bank of America’s “Keep the Change” program all round up purchases and deposit the difference into savings. If manual rounding sounds tedious, let technology do the work.

Total saved: $300-$600 per year

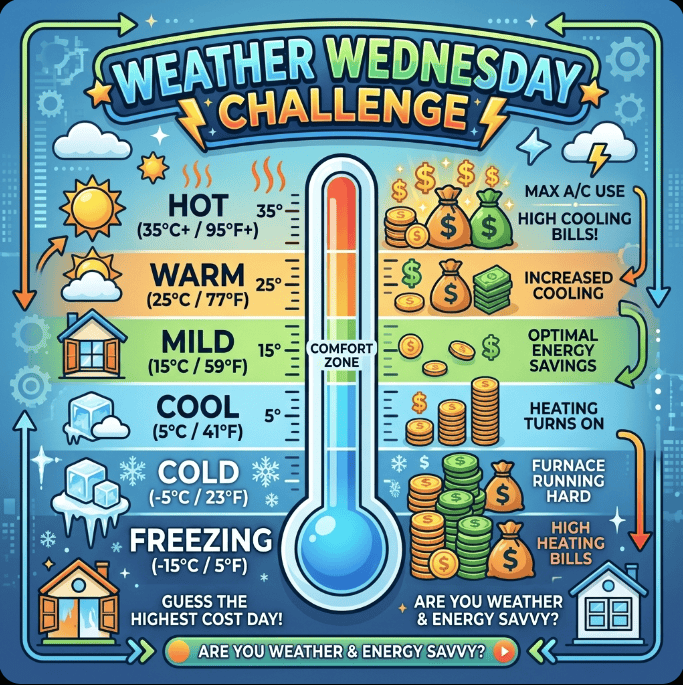

Challenge 5: The Weather Wednesday Challenge

Here’s a fun one. Every Wednesday, check the temperature outside and save that amount in dollars.

If it’s 72 degrees, save $72. If it’s 35 degrees, save $35. If it’s 98 degrees in August, well, your savings account is going to have a great week.

This challenge is unpredictable, which is what makes it fun. You never know exactly what you’ll save each week, and it connects your saving habit to something you’re already aware of — the weather.

Over a full year, depending on where you live, this challenge can net you anywhere from $2,000 to $4,000. If those amounts are too high for some weeks, modify the rule — save half the temperature, or save the temperature in cents instead of dollars.

Total saved: $2,000-$4,000 per year (adjustable)

Challenge 6: The Penny Challenge (365 Days)

This is the gentlest savings challenge you’ll find, and it’s perfect for anyone who feels like they literally cannot afford to save anything.

Day one, save one penny. Day two, save two pennies. Day three, three pennies. You increase by one penny each day for a full year.

By the end of 365 days, you’ll have saved $667.95.

Now, I know what you’re thinking — “saving pennies seems pointless.” But that’s exactly why it works. The amounts are so ridiculously small at the beginning that there’s absolutely no excuse not to do it. And by the time you’re saving $2 or $3 per day in the later months, the habit is so deeply ingrained that it feels automatic.

This challenge proves a powerful point: you don’t need to start big. You just need to start.

Total saved: $667.95

Challenge 7: The Bi-Weekly Savings Challenge

If you get paid every two weeks, this challenge aligns perfectly with your paycheck cycle.

Every payday, increase your savings transfer by $10. First paycheck, save $10. Second paycheck, save $20. Third paycheck, $30. And so on through all 26 pay periods of the year.

By the end of the year, you’ll have saved $3,510.

What makes this work is that it ties directly to when money hits your account. You save before you spend, and the increases are gradual enough that your lifestyle adjusts naturally. By the time you’re saving $200+ per paycheck toward the end of the year, you’ve already adapted to living on less because the changes happened slowly.

Pro Tip: Set up automatic transfers on payday so the money moves before you even see it in your checking account. What you don’t see, you don’t miss.

Total saved: $3,510

Challenge 8: The Spare Change Jar Challenge

Old school? Absolutely. Effective? Surprisingly, yes.

Get a large jar, put it somewhere you pass every day — your kitchen counter, your dresser, by the front door — and dump all your spare change into it at the end of each day. Coins from your pockets, coins from your car cup holder, coins from the bottom of your bag.

At the end of the year, take the jar to a Coinstar machine or your bank. Most people are shocked to find they’ve saved between $200 and $500 without any conscious effort.

If you want to supercharge this, add a rule: any $1 bills go in the jar too.

Total saved: $200-$500+ per year

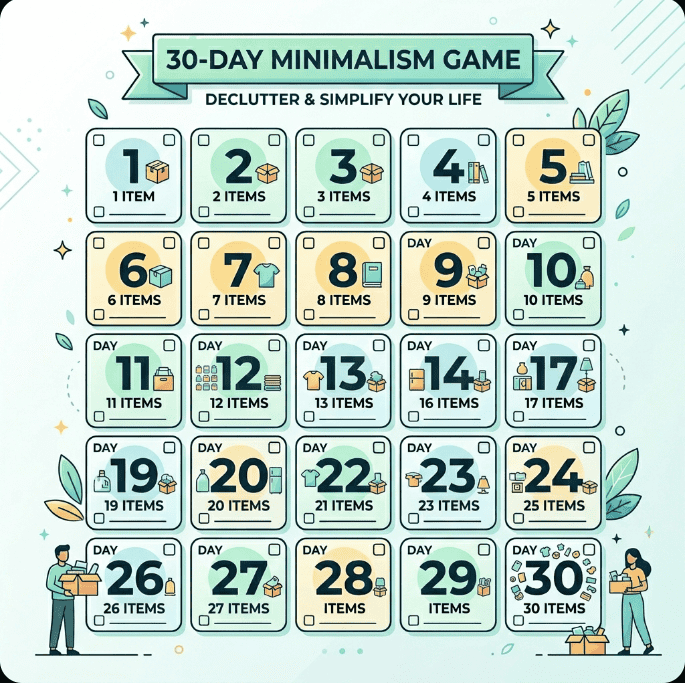

Challenge 9: The 30-Day Minimalism Game

This challenge comes from The Minimalists, and it’s brilliant because it combines decluttering with earning money.

On day one, find one item in your house you no longer need and sell it or set it aside. On day two, find two items. Day three, three items. By day 30, you’re finding 30 items.

Over 30 days, you’ll identify 465 items you don’t need. Sell them on Facebook Marketplace, eBay, Mercari, or at a garage sale. Donate what doesn’t sell.

Most people earn between $200 and $1,000 from selling their unwanted stuff, depending on what they have. But the real benefit goes beyond the money — you end up with a cleaner, less cluttered home, which reduces stress and makes you more intentional about future purchases.

Total earned: $200-$1,000+

Challenge 10: The “Cancel One Thing” Challenge

Look at your bank statement right now. Count how many recurring subscriptions and memberships you’re paying for. Netflix, Spotify, gym membership, streaming services, app subscriptions, magazine subscriptions, meal kit services, software tools, cloud storage upgrades — it adds up fast.

The average American spends about $219 per month on subscriptions. Many of them are for services they rarely or never use.

Here’s the challenge: cancel one subscription per month for the next 6 months. Just one. Pick the one you used the least in the past 30 days. Cancel it today. Next month, cancel another one.

Even if each subscription is only $10 to $15, canceling six of them saves you $60 to $90 per month — that’s $720 to $1,080 per year of found money.

You probably won’t even miss most of them.

Pro Tip: Before canceling, check if you can downgrade to a free tier instead. Spotify Free, YouTube with ads, and basic cloud storage often cover 90% of what you actually use.

Total saved: $720-$1,080 per year

Challenge 11: The “Match It” Challenge

This one works great for couples, but anyone can do it.

Every time you spend money on a non-essential item — a latte, a new shirt, a movie ticket, takeout dinner — you “match” that amount by putting the same dollar amount into savings.

Bought a $5 latte? Transfer $5 to savings. Ordered $30 of takeout? Save $30. Spent $60 on a new pair of shoes? That’s $60 to savings.

This challenge makes you hyper-aware of your discretionary spending because every purchase has a double cost. You’ll naturally start spending less because you know you have to save the same amount. And when you do spend, your savings benefit equally.

Depending on your spending habits, this can easily generate $2,000 to $5,000 in savings per year.

Total saved: $2,000-$5,000 per year

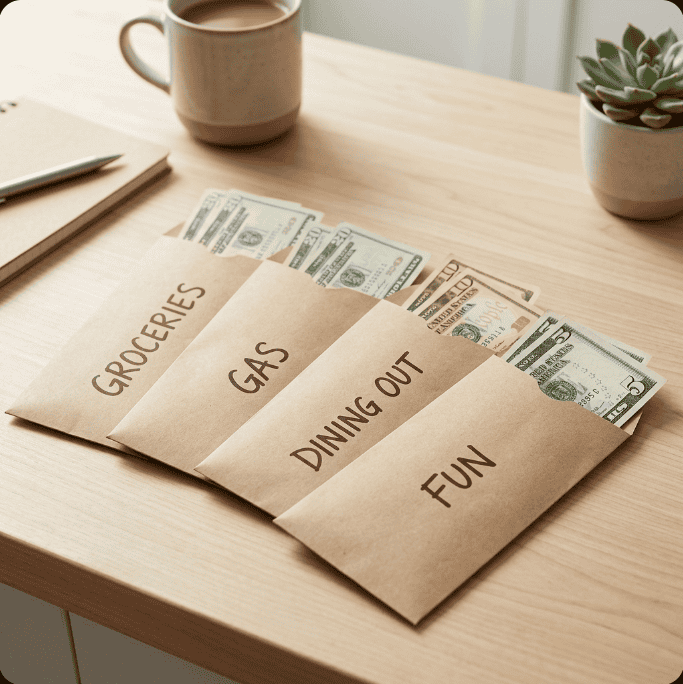

Challenge 12: The Cash-Only Challenge

For one full month, use only cash for all variable expenses. No credit cards, no debit cards, no Apple Pay, no Venmo for non-bills.

At the beginning of the month, withdraw your budgeted amount for groceries, gas, dining, entertainment, and personal spending. Divide it into envelopes. When an envelope is empty, you’re done spending in that category.

Studies consistently show that people spend 12% to 18% less when they use cash instead of cards. There’s something psychological about physically handing over money that makes each purchase feel more real.

On a typical monthly variable spending of $1,500, saving 15% means an extra $225 per month — or $2,700 per year.

Total saved: $2,000-$3,000 per year

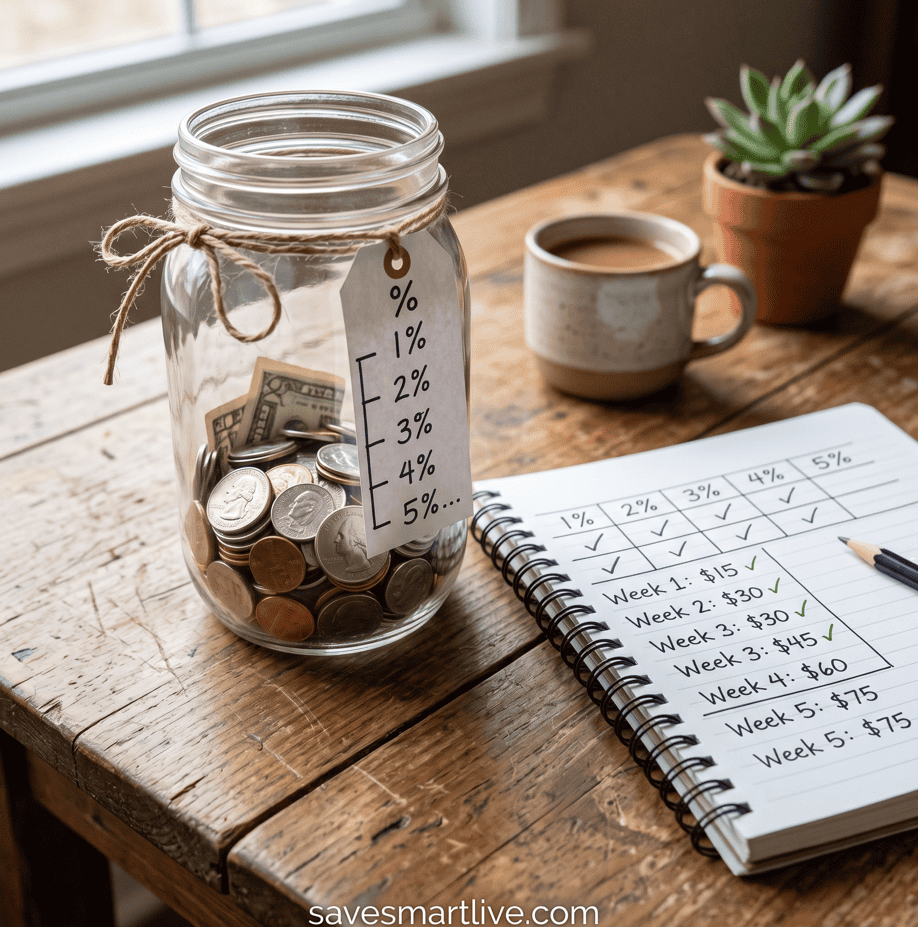

Challenge 13: The 1% Challenge

This one is for people who want to save more but feel like they can’t afford it.

Starting this month, save 1% of your income. That’s it. If you make $3,000 a month, that’s $30. Next month, bump it up to 2%. Then 3%. Increase by one percent each month.

By month 12, you’re saving 12% of your income — a rate that would have felt impossible when you started, but now feels completely normal because you adjusted gradually.

The magic of this challenge is that 1% is so small it’s invisible to your lifestyle. And each subsequent 1% increase is equally invisible. But the cumulative effect over a year is massive. On a $3,000 monthly income, you’d save approximately $2,340 in the first year.

Pro Tip: Don’t wait until you “feel ready” to increase the percentage. Schedule the increase in advance for the 1st of each month so it happens automatically.

Total saved: Varies (approximately $2,000-$4,000 on average income)

Challenge 14: The Holiday Sinking Fund Challenge

This isn’t a typical savings challenge — it’s a strategy that prevents the single biggest budget-busting event of the year: holiday spending.

The average American family spends about $900 on Christmas gifts alone. Add in decorations, food, travel, and events, and it easily hits $1,200 to $1,500. For most families, this spending goes straight onto credit cards, which then takes months to pay off.

Here’s the challenge: starting in January, save $100 per month into a dedicated “Holiday Fund.” By November, you’ll have $1,100 sitting there waiting — and December spending won’t touch your regular budget or your credit cards.

If $100 per month is too much, adjust to $50 or $75. The point is that you’re saving throughout the year instead of scrambling in December.

This challenge alone can prevent $500 to $1,500 in credit card debt every year.

Total saved: $600-$1,200 (plus credit card interest avoided)

Challenge 15: The 100 Envelope Challenge

This challenge went viral on social media, and for good reason — it’s visual, it’s exciting, and it can save you a serious amount of money.

Number 100 envelopes from 1 to 100. Every day (or every other day, or twice a week — whatever pace works for you), randomly pick an envelope and put that dollar amount inside it. Envelope #47? Put $47 in it. Envelope #3? Put $3 in.

When all 100 envelopes are filled, you’ll have saved exactly $5,050.

The random element keeps it interesting — you never know if you’re going to pull a $2 envelope or a $95 envelope. And physically stuffing cash into envelopes makes the savings feel tangible and real.

If $5,050 feels like too much, modify the challenge: use 50 envelopes ($1,275 total) or scale each amount by half (envelopes 0.50 to $50 for a $2,525 total).

Total saved: $5,050 (adjustable)

How to Choose the Right Savings Challenge for You

With 15 options in front of you, here’s how to pick the one that will actually stick.

If you’ve never saved consistently before, start with the Penny Challenge or the 52-Week Challenge. They build the habit without any financial pressure.

If you’re an impulse spender, the Cash-Only Challenge or the Match It Challenge will transform your awareness of where money goes.

If you want maximum savings in minimum time, the 100 Envelope Challenge or the Bi-Weekly Challenge will build your savings the fastest.

If you’re a couple, the Match It Challenge and the Holiday Sinking Fund are perfect for doing together and keeping each other accountable.

If you want something fun and unpredictable, the Weather Wednesday Challenge or the $5 Bill Challenge add an element of surprise that keeps things interesting.

The most important thing is this: pick one challenge and start it today. Not tomorrow, not next Monday, not next month. Today. Even if all you do is save $1, you’ve begun.

Pro Tip: You can combine challenges. Run the 52-Week Challenge as your baseline and add the $5 Bill Challenge or the Round-Up Challenge on top for bonus savings.

How to Track Your Savings Challenge Progress

Tracking your progress is what separates people who finish challenges from people who quit in week three. Here are the best ways to stay on track.

Use a physical tracker on your wall. Print a chart for your specific challenge and tape it somewhere you’ll see it every day — the fridge, the bathroom mirror, your home office wall. There’s something deeply satisfying about physically marking off each milestone.

Use a savings challenge app. Apps like SaverLife, Qapital, and even simple habit-tracking apps like Streaks or HabitBull can automate reminders and track your progress digitally.

Use a spreadsheet. Create a simple Google Sheet with your target amounts, actual amounts saved, and a running total. Add a chart that shows your savings growing over time — watching that line go up is incredibly motivating.

Tell someone about your challenge. Accountability matters. Share your challenge with a friend, your partner, or even on social media. When other people know about your goal, you’re significantly more likely to follow through.

![]()

What to Do With the Money You Save

Saving money is great. But what you do with it matters even more. Here are the smartest ways to use your challenge savings, in order of priority.

First, build a starter emergency fund. If you don’t have at least $1,000 set aside for emergencies, that’s where your savings should go first. This small cushion prevents you from going into debt when the car breaks down or the dog needs a vet visit.

Second, pay down high-interest debt. Credit card debt at 20% to 29% interest is an emergency. Every dollar you throw at it gives you an immediate guaranteed return equal to that interest rate.

Third, build a full emergency fund. Financial experts recommend 3 to 6 months of essential expenses. This is your financial safety net that lets you sleep at night.

Fourth, start investing. Once your emergency fund is solid and high-interest debt is gone, put your savings to work. Even $100 per month invested in an index fund can grow to over $180,000 in 30 years thanks to compound interest.

Frequently Asked Questions

Which savings challenge saves the most money?

The 100 Envelope Challenge saves the most at $5,050, followed by the Bi-Weekly Challenge at $3,510 and the Weather Wednesday Challenge which can reach $4,000 depending on your climate. However, the “best” challenge is the one you’ll actually complete. Saving $1,378 with the 52-Week Challenge is infinitely better than starting and quitting a challenge that promises $5,000.

Can I do a savings challenge with a low income?

Absolutely. The Penny Challenge saves $667.95 over a year and starts with literally one cent. The Round-Up Challenge saves small amounts on purchases you’re already making. The 1% Challenge starts at just 1% of whatever you earn. No income is too small to start saving.

What if I miss a week or fall behind?

Don’t quit. Just pick up where you left off or double up the next week. A savings challenge is not a pass-fail test — it’s a tool to build a habit. If you complete 80% of the challenge, you still saved 80% of the money. That’s a huge win.

Should I use a savings account or keep cash?

For most challenges, a separate high-yield savings account works best because the money earns interest and isn’t as tempting to spend. However, the Cash Envelope and $5 Bill challenges work better with physical cash because the tangible nature is part of what makes them effective. Use whatever method reduces the temptation to spend the savings.

Can I combine multiple savings challenges?

Yes, and many people do. A popular combination is running the 52-Week Challenge as a baseline while also doing the $5 Bill Challenge and the Round-Up Challenge on top. Just make sure the combined amounts are realistic for your budget. The goal is to save more, not to overcommit and give up.

How do I stay motivated when the challenge gets hard?

Three things help the most. First, track your progress visually — watching the numbers grow is the best motivation. Second, celebrate milestones. When you hit $500 saved, do something small to acknowledge it. Third, remember your why. Are you saving for an emergency fund? A vacation? Debt freedom? Keep that goal visible.

When is the best time to start a savings challenge?

Right now. Seriously. Most people wait for January 1st or the first of the month, but there’s no rule that says you can’t start a 52-week challenge in April or a no-spend challenge on a random Wednesday. The best time to start saving was yesterday. The second best time is today.

Start Your First Savings Challenge Today

You’ve now got 15 proven challenges to choose from. Some will save you a few hundred dollars. Others could save you over $5,000 in a single year. But here’s what matters most — none of them work unless you actually start.

So here’s my challenge to you: pick one challenge from this list right now, write down the name of the challenge and your start date, and save your first amount today. Whether that’s one penny, one dollar, or $52 — just begin.

A year from now, you’ll be so glad you started today.

Your future self is counting on you. Don’t let them down.

Did this guide help you? Save it to your Pinterest board and share it with a friend who needs to hear this! For more money-saving strategies, check out our other guides on SaveSmartLive.com.

Related articles:

- How to Create a Monthly Budget That Actually Works (2026 Guide)

- How to Start an Emergency Fund From Zero

- 10 Things to Stop Buying to Save $500 a Month

- 50/30/20 Budget Rule Explained (With Free Template)Read More: $50 Weekly Meal Plan for a Family of Four (With Grocery List)