Free Budget Printables

15 Free Budget Printables You Need Right Now (Start Saving Today!)

Let’s be honest — budgeting sounds great in theory, but the moment you try to do it in your head or on a random sticky note, it falls apart within a week. You forget a bill here, overspend on groceries there, and by the end of the month you’re wondering where your paycheck disappeared to. Sound familiar? You’re not alone.

Here’s the good news: you don’t need a fancy app or a financial advisor to get your money under control. All you need are the right free budget printables — simple, beautifully designed sheets you print at home, fill in with a pen, and actually stick to. There’s something powerful about writing your finances down on paper. It makes everything feel real, trackable, and surprisingly satisfying when you cross off a goal.

Whether you’re trying to pay off debt, save for a vacation, or just stop living paycheck to paycheck, these 15 free budget printables are exactly what you need to get started today. Each one is designed to solve a specific money problem, and the best part? They’re completely free.

1. Monthly Budget Planner — Your Money’s Best Friend

If there’s one printable every person on earth should have, it’s a monthly budget planner. This is the foundation of everything. Before you can save money, pay off debt, or reach any financial goal, you need to know exactly how much money is coming in and where every single dollar is going. A monthly budget planner gives you that crystal-clear picture in one place.

A good monthly budget planner has sections for your income (salary, side income, freelance work), your fixed expenses (rent, car payment, insurance), your variable expenses (groceries, gas, entertainment), and a space at the bottom to see whether you have money left over or you’re running a deficit. The magic happens when you sit down at the start of each month, fill it in honestly, and actually follow it throughout the month.

What makes this printable so powerful is that it forces you to be intentional. When you write down that you plan to spend $300 on groceries this month, you’ll naturally think twice before throwing extras into your cart. Print one of these at the start of every month, and within 60 days, you’ll feel more in control of your finances than you ever have before.

2. Weekly Expense Tracker — Catch the Small Leaks Before They Drain You

You know that feeling when you check your bank account and you’re somehow $200 shorter than expected — and you have absolutely no idea where it went? That’s what happens when you skip tracking your weekly expenses. The culprit is almost always small, seemingly harmless purchases: a $6 latte here, a $12 lunch there, a quick Amazon add-to-cart moment — it all adds up faster than you think.

A weekly expense tracker is your secret weapon against these sneaky spending leaks. It’s a simple printable where you record every single purchase throughout the week — big and small. At the end of the week, you add it all up and compare it against your monthly budget. Most people are genuinely shocked when they see their weekly totals on paper for the first time.

The beauty of tracking weekly instead of monthly is that you catch problems early. If you’ve blown your dining-out budget by Wednesday, you still have time to correct course for the rest of the month. Print out four of these at the start of each month and keep one on your desk, kitchen counter, or in your purse. The act of writing down each purchase — even a $2 candy bar — builds the awareness that leads to lasting financial change.

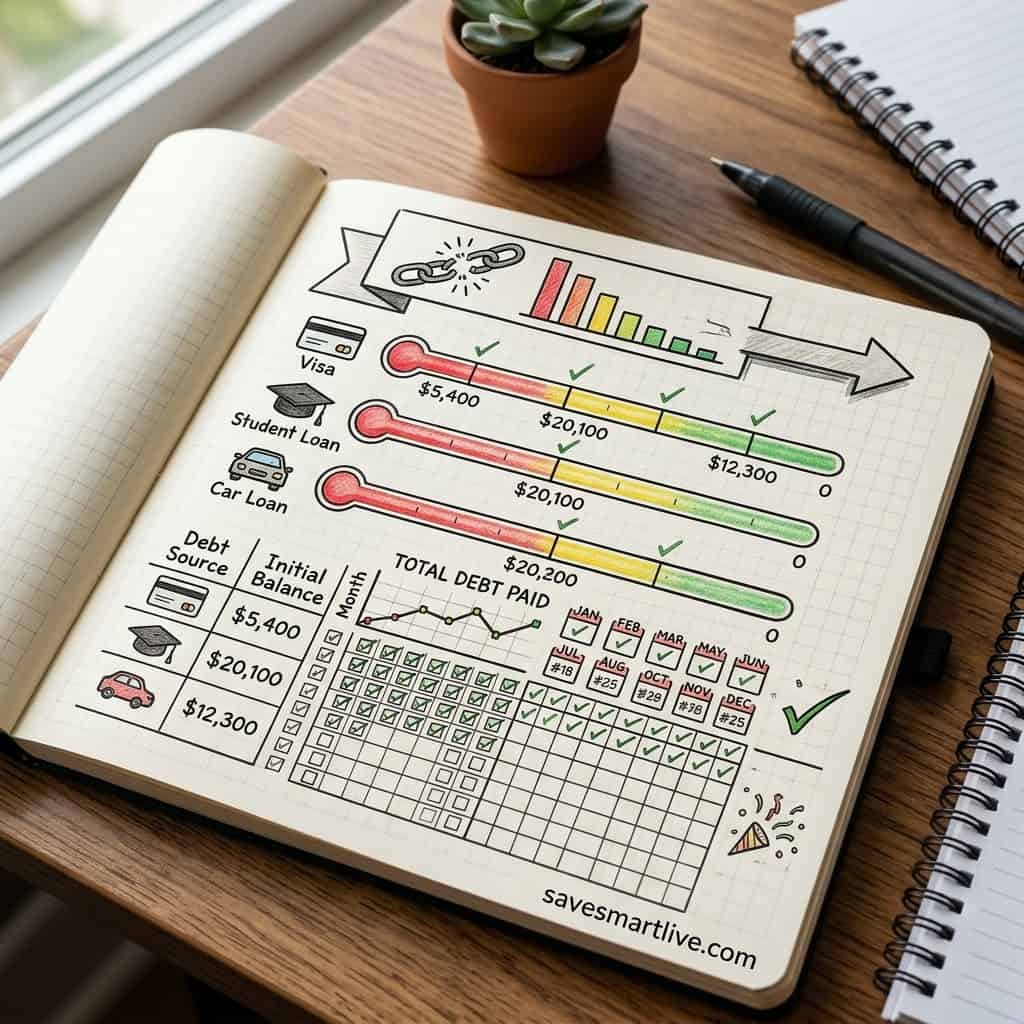

3. Debt Payoff Tracker — Watch Your Debt Disappear in Real Time

Debt is one of the most emotionally heavy burdens a person can carry, and a huge part of that weight comes from not having a clear picture of your progress. When you’re staring at a $15,000 credit card balance, it can feel like you’ll never get out — so you avoid thinking about it altogether. That avoidance is exactly what keeps people stuck in debt for years, sometimes decades.

A debt payoff tracker changes everything. This printable gives you a visual representation of your debt — usually a thermometer, a progress bar, or a grid of boxes — where you color in or cross off sections as you pay down your balance. It sounds simple, but the psychological impact is enormous. Every time you color in a box, your brain gets a little shot of dopamine, reinforcing the behavior of paying down debt. It transforms a painful process into something that actually feels rewarding.

Most debt payoff trackers work beautifully with the debt snowball method — where you pay off your smallest debt first for quick wins — or the debt avalanche method, where you target the highest-interest debt first to save the most money. Either way, having a tracker keeps you motivated on the long, often frustrating journey to becoming debt-free. Print one for each of your debts, hang them somewhere visible, and watch that progress build week by week.

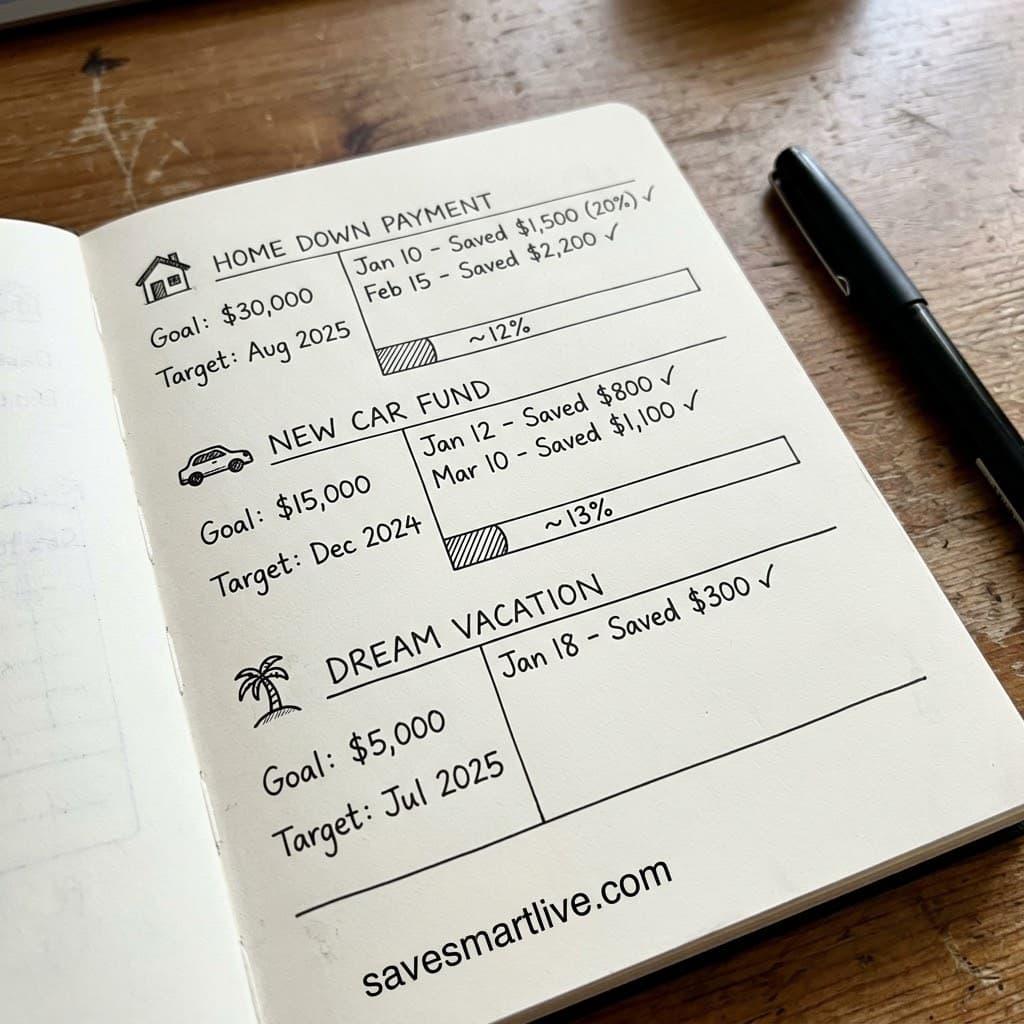

4. Savings Goal Tracker — Make Your Dreams Visual and Achievable

There’s a massive difference between saying “I want to save money” and saying “I am saving $5,000 for a vacation to Bali by December.” The first is a wish. The second is a goal. And a savings goal tracker is how you turn that goal into a daily, visual reminder that keeps you pushing forward even when you’re tempted to splurge.

These printables are often designed as fun, colorful visual charts — a jar you fill up coin by coin, a savings ladder you climb rung by rung, or a honeycomb grid you color in cell by cell. You write your total goal at the top, break it into smaller milestones, and mark your progress every time you make a deposit toward that goal. Some people save these trackers for big goals like an emergency fund or a down payment on a house. Others use them for fun goals like a dream vacation or a new laptop.

The key is specificity. Don’t just write “savings” — write the exact dollar amount, the exact deadline, and what you’re saving for. Then put the tracker somewhere you see it every single day. On the fridge, above your desk, in your planner. The more you look at it, the more motivated you’ll be to make choices that move you closer to that goal instead of further away from it.

5. Bill Payment Checklist — Never Miss a Due Date Again

Late fees are literally the most pointless way to lose money. You’re not buying anything fun. You’re not treating yourself. You’re just paying extra because you forgot. And yet, with busy schedules and a dozen different bills due at different times of the month, it’s incredibly easy for things to slip through the cracks — especially if you’re juggling rent, utilities, internet, streaming subscriptions, insurance, loan payments, and more.

A bill payment checklist is the simplest possible solution to this problem. It’s a printable that lists all your monthly bills along with their due dates, the minimum payment amount, and a checkbox to mark when you’ve paid them. Some versions also have space to note the account number or website login so everything is in one place. At the beginning of each month, you fill it in with the amounts due, and throughout the month you check off each bill as you pay it.

This one printable alone could save you hundreds of dollars a year in late fees, plus protect your credit score from the damage that late payments cause. It takes less than five minutes to set up and is one of those small organizational changes that pays for itself (literally) from the very first month. Tape it inside a kitchen cabinet, on your home office wall, or keep it in a monthly budget binder — wherever you’ll actually see it when bills are due.

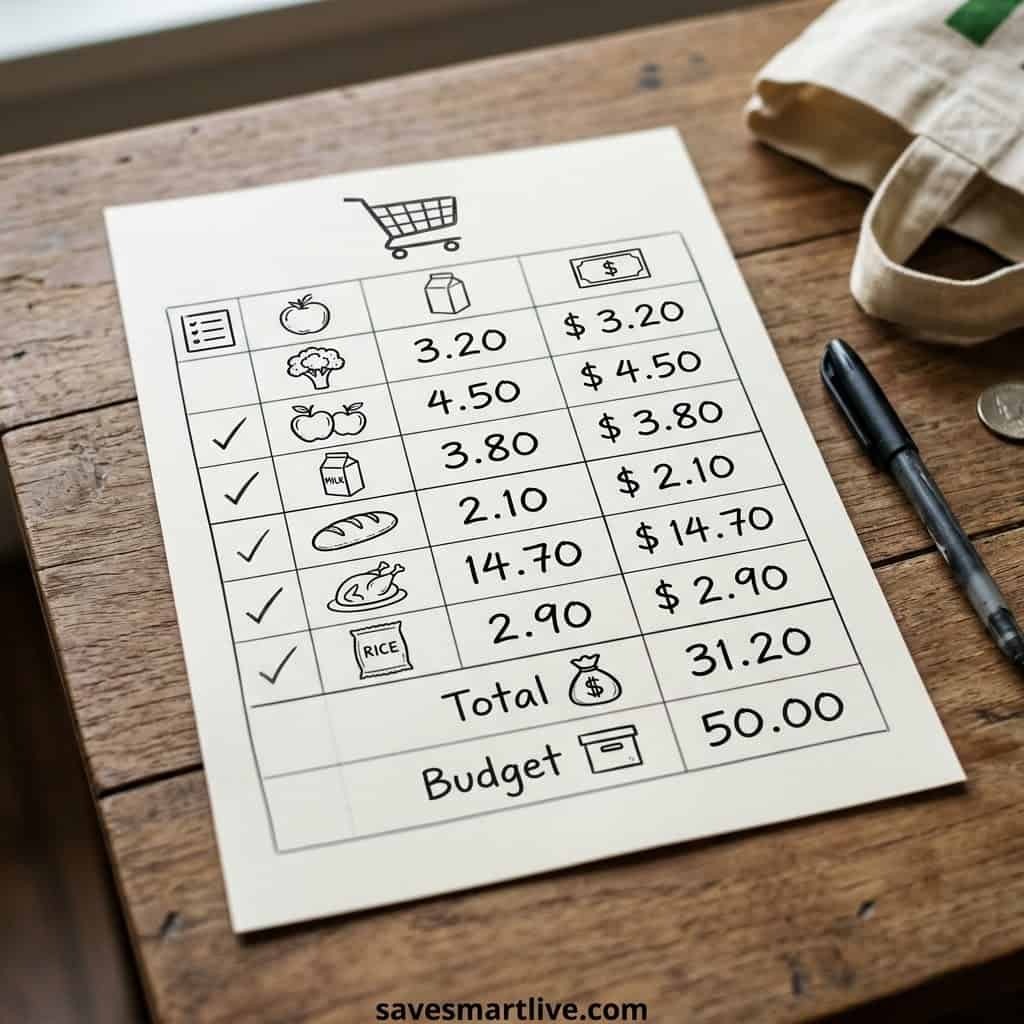

6. Grocery Budget Worksheet — Stop Overspending at the Supermarket

Groceries are one of the most unpredictable spending categories for most households. Unlike rent or a car payment — which stays the same every month — your grocery bill can swing wildly depending on what you buy, where you shop, and whether you go to the store hungry. For many families, the grocery bill is the single biggest variable expense, and it’s also one of the easiest places to cut costs without sacrificing quality of life.

A grocery budget worksheet combines meal planning with budgeting in one printable. You plan out your meals for the week, list the ingredients you need, estimate the cost of each item based on store prices or past receipts, and set a total budget for the trip. When you get to the store, you’re not wandering aimlessly — you know exactly what you need, roughly what it should cost, and you have zero reason to impulse-buy a $14 bottle of fancy olive oil you’ll use once.

Studies consistently show that people who shop with a list spend significantly less than those who go without one. Add a budget column to that list, and the savings get even bigger. Over a year, even trimming $50 a month off your grocery bill adds up to $600 — that’s a solid start on an emergency fund or a weekend getaway. Print a fresh worksheet each week and make it part of your Sunday meal-prep routine.

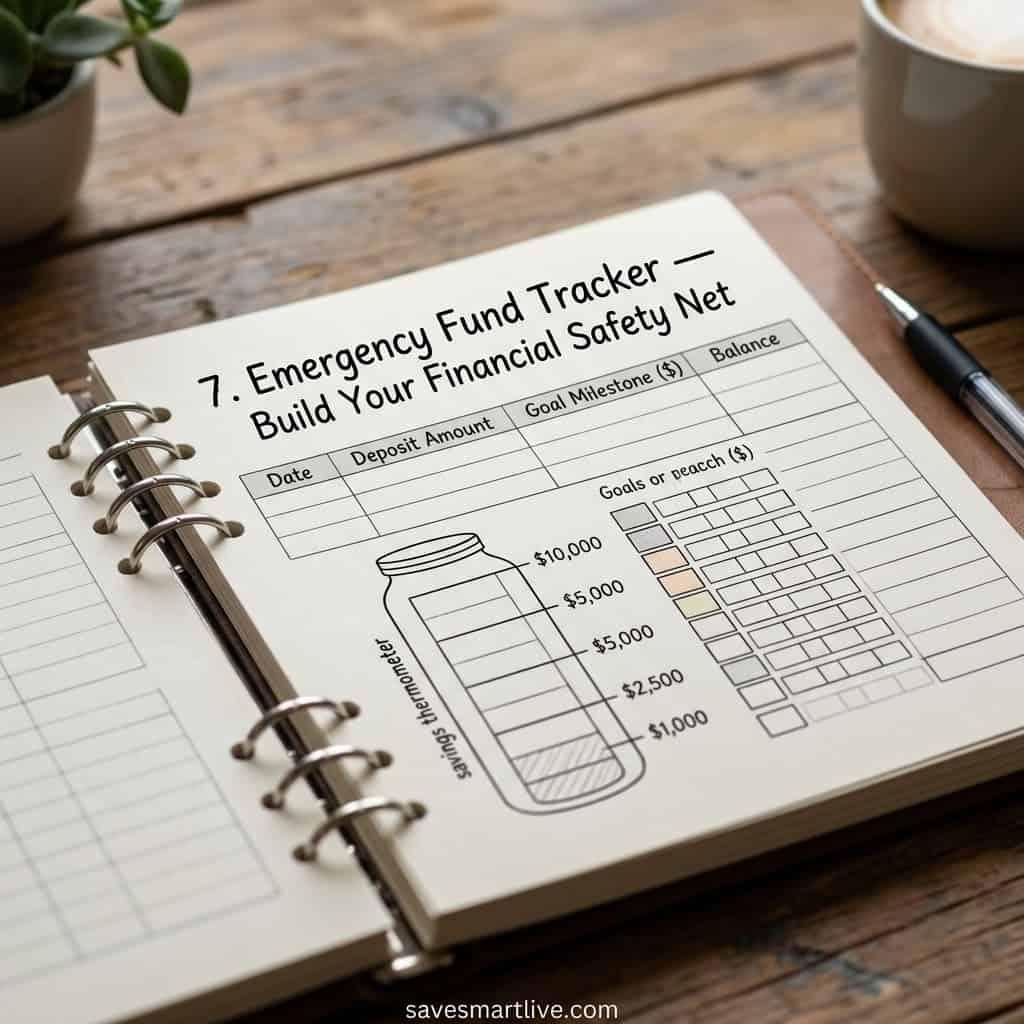

7. Emergency Fund Tracker — Build Your Financial Safety Net

Financial experts universally agree on one thing: you need an emergency fund. Not next year, not when things are more stable — now. An emergency fund is the difference between a flat tire being a minor inconvenience and a financial catastrophe. It’s the cushion that keeps one bad month from turning into a downward spiral of debt. Most experts recommend having 3 to 6 months of living expenses saved — but even $1,000 is enough to protect you from most common emergencies.

The problem is that building an emergency fund feels slow and boring, especially when you’re working with a tight budget. That’s exactly where an emergency fund tracker earns its value. Similar to a savings goal tracker but specifically for your emergency fund, this printable gives you a visual progress chart that makes the slow, steady process of building your safety net feel exciting and rewarding. Every $50 you add gets recorded and celebrated.

Set a realistic milestone — maybe $500 to start, then $1,000, then one month of expenses. Track each deposit on your printable and watch the chart fill up over time. Keep this fund in a separate savings account you don’t touch unless there’s a genuine emergency (vacations and sales do not count as emergencies). The peace of mind that comes from knowing you have a safety net is worth every sacrifice you make to build it.

8. No-Spend Challenge Tracker — Reset Your Spending Habits in 30 Days

If your budget feels completely out of control and you don’t know where to start, a no-spend challenge might be exactly what you need. The concept is beautifully simple: for a set period — usually 7, 14, or 30 days — you commit to spending money only on absolute necessities. No restaurants, no online shopping, no entertainment purchases, no impulse buys. Just rent, utilities, groceries, and anything else that’s truly essential to your daily life.

A no-spend challenge tracker makes this challenge manageable and even fun. It’s a printable calendar or chart where you mark each successful no-spend day with a sticker, a checkmark, or a color. At the end of the challenge, you can clearly see how many days you succeeded, and you’ll also see exactly how much money you saved compared to a typical month. Most people are absolutely stunned by the number.

Beyond the financial savings, a no-spend challenge is a powerful reset for your mindset around money. After 30 days of being intentional about every purchase, you start to question whether you actually need things before you buy them — and that habit tends to stick long after the challenge ends. Start with a weekend challenge if 30 days feels too intimidating, and build up from there. The results are life-changing for many people who’ve tried it.

9. Sinking Funds Planner — Budget for Big Expenses Before They Hit

Here’s a financial concept that sounds complicated but will completely change how you manage money: sinking funds. A sinking fund is money you set aside every month for a large, predictable future expense. Car registration, Christmas gifts, annual insurance premiums, home repairs, back-to-school shopping — these expenses happen every year, yet most people treat them like total surprises and scramble to cover them. Sinking funds eliminate that scramble entirely.

A sinking funds planner printable helps you identify all the irregular expenses coming up in your life, calculate how much you need to save for each one, and divide that total by the number of months until the expense hits. For example, if Christmas typically costs you $600 and it’s six months away, you need to set aside $100 per month in your Christmas sinking fund. When December rolls around, the money is already there — no debt, no stress, no overdraft.

The relief this creates is hard to describe until you’ve experienced it. Imagine knowing that your car’s annual service, your property taxes, and your holiday shopping are all fully funded before the bill even arrives. That’s what sinking funds do for your financial life. Use the printable to list all your upcoming irregular expenses, calculate your monthly savings amounts, and add those amounts to your monthly budget. Future-you will be endlessly grateful.

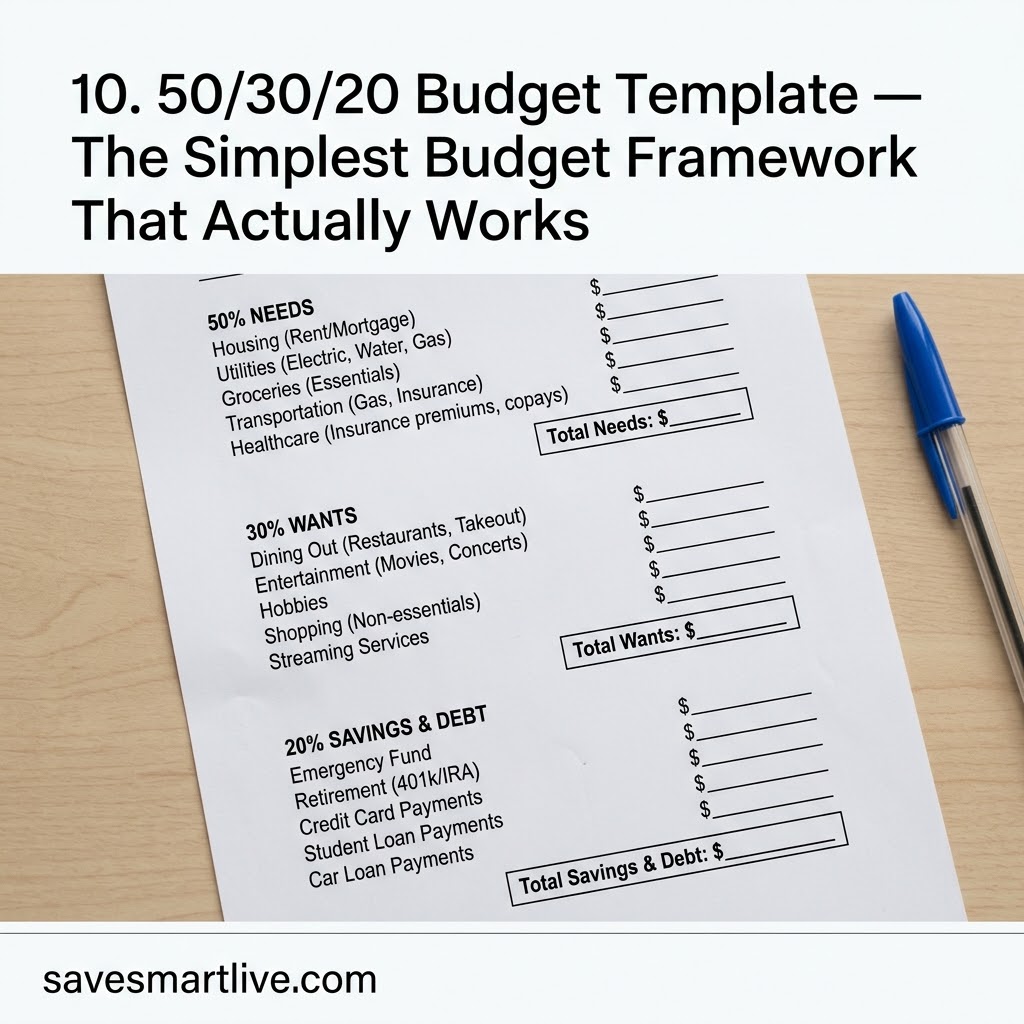

10. 50/30/20 Budget Template — The Simplest Budget Framework That Actually Works

If traditional budgeting feels overwhelming — all those categories and subcategories and spreadsheet formulas — the 50/30/20 rule is the beautiful, simple alternative you’ve been looking for. Popularized by Senator Elizabeth Warren in her book on personal finance, this framework breaks your after-tax income into just three buckets: 50% for needs, 30% for wants, and 20% for savings and debt repayment. That’s it. Three numbers. No complicated spreadsheets required.

A 50/30/20 budget template printable does the math for you. You enter your monthly take-home income, and the sheet automatically shows you how much should go to each category. Needs include rent, utilities, groceries, transportation, and minimum debt payments — things you can’t live without. Wants cover dining out, subscriptions, hobbies, and entertainment — the enjoyable extras. The remaining 20% builds your savings and attacks your debt.

What makes this budget so beginner-friendly is its flexibility. You don’t have to track 20 different spending categories — just three. If you overspend on wants in a given month, you adjust the next month. It’s simple enough to maintain consistently, which is the real secret to budgeting success. Over time, as your income grows, you can increase the savings percentage. But for anyone just starting their budgeting journey, the 50/30/20 template is the perfect first step.

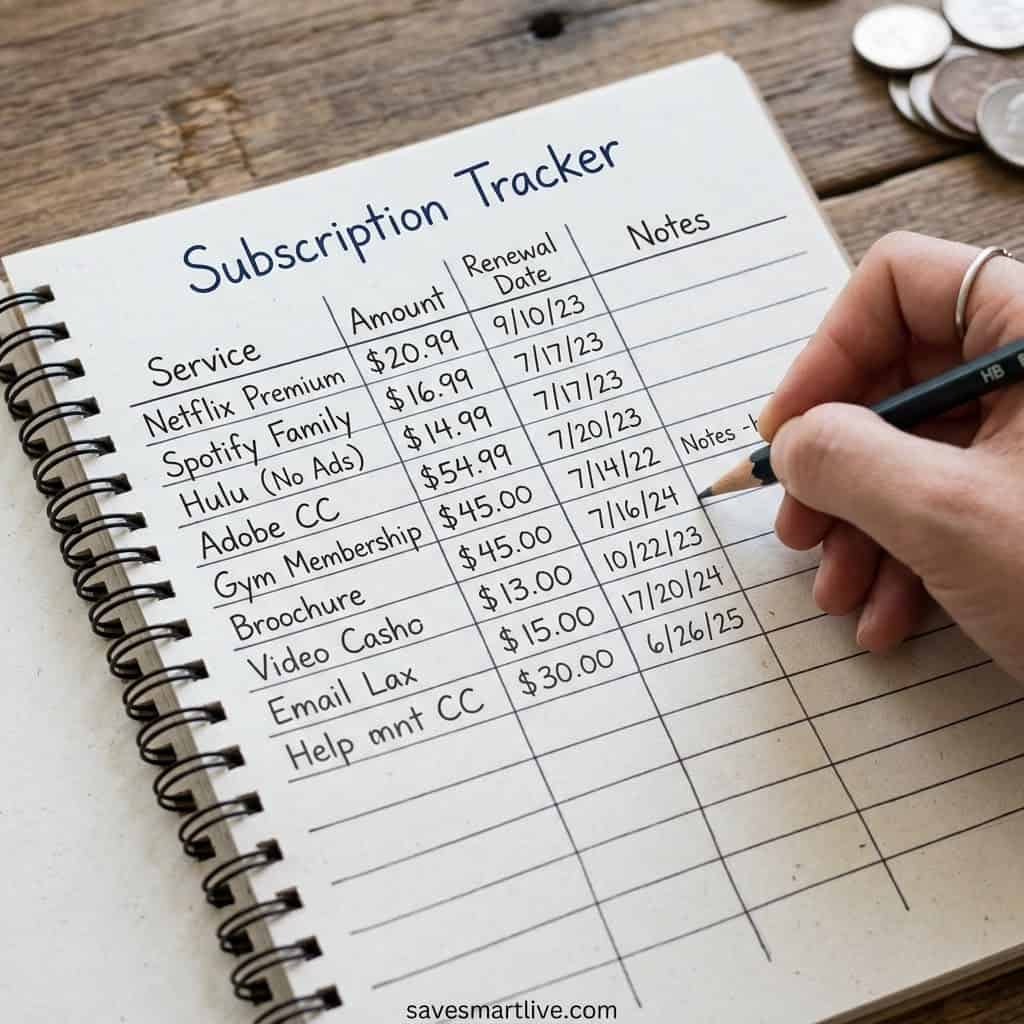

11. Subscription Tracker — Find the Money You’re Wasting Every Month

Quick question: how many subscriptions are you currently paying for? Netflix, Spotify, Hulu, Amazon Prime, Audible, a gym you haven’t visited since January, a meal kit service you paused but forgot to cancel, an app you downloaded for a free trial three years ago… Most people have absolutely no idea how many subscriptions they’re paying for, and the cumulative cost is often jaw-dropping. Research suggests the average American spends over $200 per month on subscriptions — and significantly underestimates that number when asked.

A subscription tracker printable is the intervention your bank account desperately needs. You list every single recurring charge — monthly and annual — along with the cost, the renewal date, and whether it’s worth keeping. Go through your last three months of bank and credit card statements to find them all. You will find at least one or two you completely forgot about. Then for each subscription, ask yourself honestly: do I use this regularly? Does it add genuine value to my life? Is there a cheaper alternative?

Most people who complete this exercise cancel at least two or three subscriptions immediately and save $30–$80 per month without feeling any loss whatsoever. That’s up to $960 per year — found money that was hiding in plain sight in your bank statements. Keep the tracker updated and review it every six months to ensure you’re only paying for things you actively value and use.

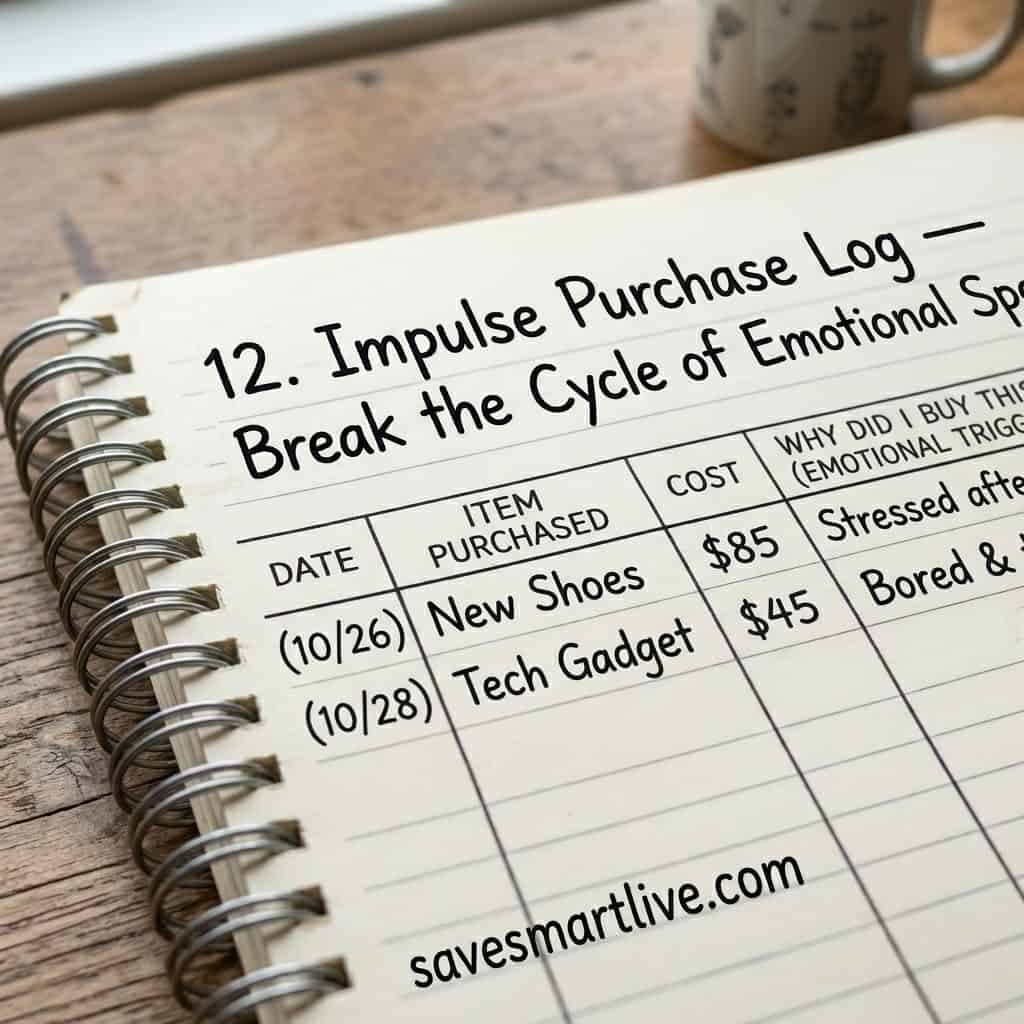

12. Impulse Purchase Log — Break the Cycle of Emotional Spending

We’ve all been there. You’re browsing online at 11 PM, mildly stressed about work, and suddenly you’re convinced that a $75 throw blanket or a $40 kitchen gadget you’ll use once is exactly what your life needs. You buy it. It arrives. You feel momentarily happy, then vaguely guilty, then you forget about it entirely. And yet the money is gone. This is impulse spending, and for many people it’s the single biggest obstacle standing between them and their financial goals.

An impulse purchase log is a powerful behavioral tool that creates a pause between the urge to buy and the actual purchase. The rule is simple: when you feel the urge to buy something that’s not on your shopping list or in your budget, you write it down in the log instead of buying it immediately. You record the item, the price, the date, and — this is the key part — why you want it right now. Bored? Stressed? Saw a social media ad? Peer pressure? Being honest about the emotional trigger behind the purchase is deeply revealing.

Then you wait. Most versions of this system suggest a 48-hour or 30-day waiting period. If you still want the item after that waiting period AND you can genuinely afford it without derailing your budget, then go ahead and buy it guilt-free. What you’ll find is that the majority of impulse urges simply disappear once the emotional moment passes. The log isn’t about deprivation — it’s about making sure your purchases are intentional decisions, not emotional reactions.

13. Paycheck Budget Planner — Budget Every Dollar the Moment You Get Paid

For many people — especially those who are paid biweekly or twice a month — waiting until the end of the month to budget is way too late. The money is already spent. A far more effective approach is to budget each paycheck the moment it hits your account, assigning every dollar a specific job before you have a chance to spend it on something unplanned. This approach, sometimes called zero-based budgeting per paycheck, is one of the most powerful financial habits you can build.

A paycheck budget planner is designed specifically for this purpose. You fill it out each time you get paid, starting with your net paycheck amount at the top. Then you work your way down, allocating amounts for savings, bills due before your next paycheck, groceries for the next two weeks, transportation, and any other spending categories relevant to your life. The goal is for the total allocations to equal your paycheck — zero dollars left unassigned, because unassigned dollars tend to evaporate mysteriously.

This printable works especially well for people who get paid irregular amounts — freelancers, commission-based workers, small business owners — because it forces you to be realistic about what you can afford based on what you actually earned, not what you hope to earn. Over time, this habit creates an extraordinary level of financial awareness and control. You stop wondering where your money went because you decided where it was going before it had a chance to disappear.

14. Holiday & Christmas Budget Planner — Enjoy the Holidays Without the January Regret

Every year, millions of people enter the holiday season with vague intentions of “not overspending this year” — and every year, those same people ring in January with a credit card bill that takes three to four months to pay off. Holiday spending is one of the most predictable financial events of the year, yet it catches people completely unprepared time and time again. The problem isn’t generosity — it’s the lack of a plan.

A holiday and Christmas budget planner changes this cycle permanently. You start by setting a total holiday budget that you can actually afford without going into debt. Then you list every person you plan to buy for, every event you’ll host or attend, travel costs, holiday decorations, food, holiday cards, and any charitable giving you want to do. You assign a specific dollar amount to each line item and add it all up. If the total exceeds your budget, you adjust — not after the shopping is done, but before it starts.

The best time to set up your holiday budget is in the fall — September or October — so you have two to three months to set aside the money before December arrives. But honestly, even if you start this in November, having any budget is dramatically better than having none. People who use a Christmas budget printable report far lower post-holiday financial stress, more meaningful gift choices, and the ability to actually enjoy the holiday season instead of dreading the January credit card statement.

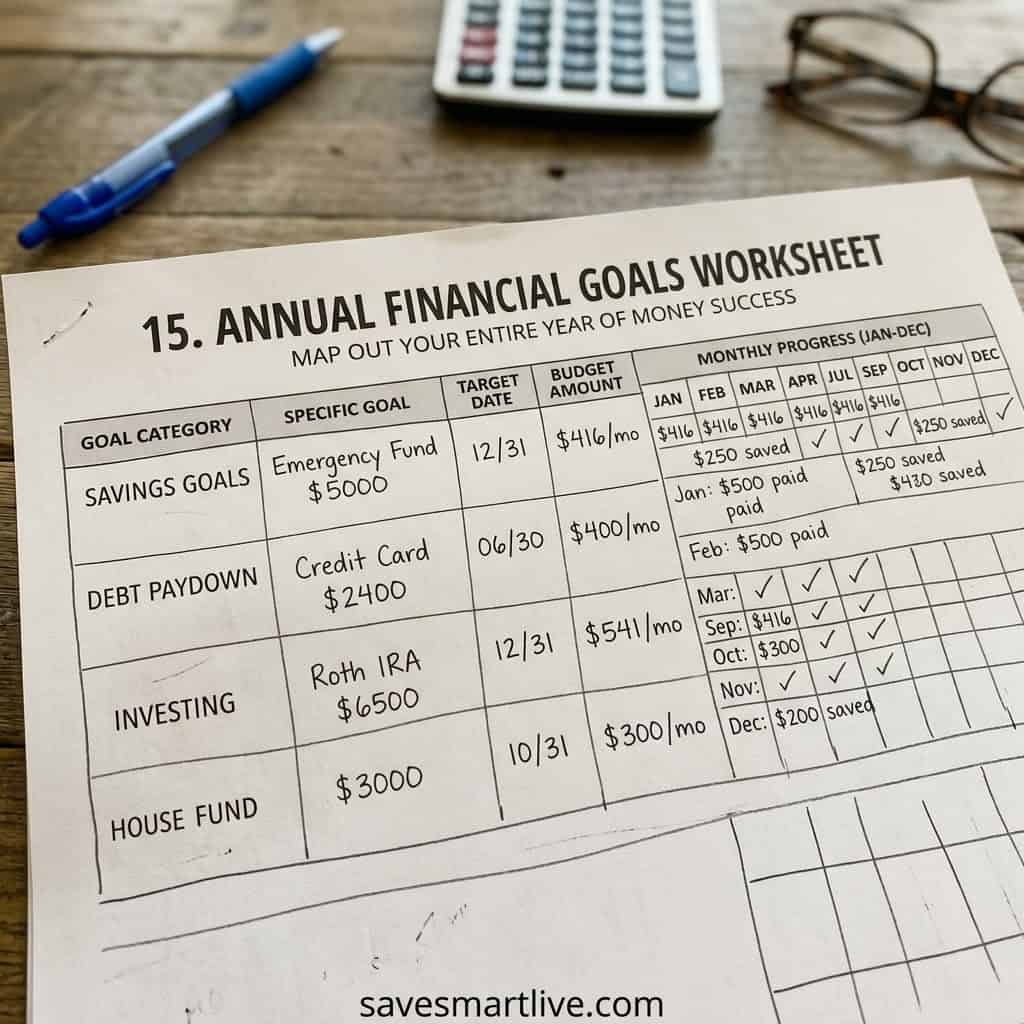

15. Annual Financial Goals Worksheet — Map Out Your Entire Year of Money Success

Monthly budgets are essential, but the most financially successful people also think long-term. They don’t just track expenses — they set clear, specific, measurable financial goals for the year ahead and check in on those goals regularly throughout the year. An annual financial goals worksheet is the tool that makes this kind of big-picture financial planning accessible to absolutely anyone, regardless of how much money they make or how far along they are on their financial journey.

This printable typically starts with a financial assessment — your current income, debts, savings balance, and net worth — so you know exactly where you’re starting from. Then it walks you through setting goals in categories like debt reduction, savings milestones, income goals, investment contributions, and major purchases. For each goal, you write the specific number, the target date, and the monthly action steps you need to take to get there. Breaking a big annual goal into twelve monthly actions is what transforms it from a dream into a reality.

At the end of each month or quarter, you check in with your worksheet — celebrating wins, adjusting anything that’s off track, and recommitting to the goals that matter most. This kind of intentional, structured approach to your finances for an entire year produces results that monthly budgeting alone simply cannot match. One year from now, you could be looking back at a year where you paid off a debt, built a real emergency fund, and saved for something you truly care about — all because you took the time to write it down and make a plan.

Final Thoughts — The Printable You Choose Matters Less Than Using It

Here’s the truth about budgeting tools: the best one is the one you’ll actually use. You could download all 15 of these free budget printables today, but if they sit in a folder on your computer, they won’t change a single thing about your financial life. The magic happens when you print them out, sit down with a pen, and commit to filling them in honestly every week and every month.

Start with just one. If you’ve never budgeted before, start with the monthly budget planner or the 50/30/20 template — something simple that gives you an immediate overview of your finances. If you’re dealing with debt, add the debt payoff tracker. If you’re a habitual impulse spender, try the impulse purchase log for 30 days and prepare to be amazed.

Financial freedom isn’t just for people who make a lot of money — it’s for people who manage their money intentionally. These free budget printables are your tools to do exactly that. Download them, print them, use them — and start building the financial future you actually want, one filled-in line at a time.

How to Start an Emergency Fund From Zero (Even on a Tight Budget)

How to Improve Your Credit Score Fast: 7 Proven Steps That Actually Work

How to Create a Monthly Budget That Actually Works (2026 Guide)

15 Money Saving Challenges to Try in 2026 (That Actually Work)

Read More : How to Create a Monthly Budget That Actually Works (2026 Guide)