Summer Savings Challenge: How to Save $1000 by September 2026 (Week-by-Week Plan)

Michael Carter

April 16, 2026

Updated May 12, 2026

19 min read

Summer Savings Challenge

How to Save $1000 by September 2026 (Week-by-Week Plan)

Last summer I did something I had never done in my entire adult life. I ended the season with more money than I started with.

That probably sounds strange. Summer is supposed to be the spending season — vacations, cookouts, ice cream runs, kids wanting to go everywhere and do everything, the electric bill climbing because the AC runs nonstop. Every summer before last, I started September wondering where all my money went. I would look at my bank account after Labor Day and feel that sinking, hollow frustration of having spent three months spending without thinking.

But last summer was different because I tried something simple. I gave myself a challenge with a specific number and a specific deadline. Save $1000 by September 1st. Not a vague intention to “save more this summer.” Not a hope that I would magically have money left over. A concrete goal with a concrete date and a concrete plan for how to get there.

I hit $1,047 by August 28th. Three days early. And the honest truth is that it was not painful. It was not a summer of deprivation where I sat inside eating ramen while my neighbors had fun. I went to the beach. I had cookouts. My kids went to the pool. We had a wonderful summer. I just made different small choices every week that added up to a thousand dollars by the time the leaves started changing.

This guide is the exact plan I followed — adapted into a week-by-week challenge that anyone can start right now. Whether summer has just begun or you are reading this in July, the math works. The strategies work. And the feeling of starting fall with $1000 you did not have before is worth every small adjustment you make along the way.

Why a Summer Savings Challenge Works Better Than Regular Saving

Before I break down the plan, let me explain why a time-limited savings challenge is psychologically more effective than just telling yourself to save money every month.

The human brain is terrible at responding to open-ended goals. “I should save more money” has no deadline, no measurement, and no finish line. Your brain treats it the same way it treats “I should exercise more” — with a nod of agreement followed by absolutely zero action. The intention is there, but the urgency is not.

A challenge changes the equation. When you say “I am saving $1000 by September 1st,” your brain suddenly has a deadline it can feel. The clock is ticking. Every week that passes is either a win or a miss. Every small decision — do I buy this $5 iced coffee or put $5 in the jar — has weight because it either moves you toward the target or away from it.

There is also something powerful about the seasonal framing. Summer has a natural beginning and end. Memorial Day to Labor Day feels like a contained chapter. You are not committing to a lifetime of sacrifice — you are committing to one season of intentional choices. That is manageable. That is doable. That is something you can actually stick with because you can see the finish line from the starting line.

And when September arrives and you have $1000 that was not there in May, the confidence that builds is extraordinary. You proved to yourself that you can save. Not in theory. In practice. With real money in a real account. That confidence carries forward into fall, winter, and every season after.

The Math: How $1000 in One Summer Actually Breaks Down

Let me kill the intimidation right now. A thousand dollars sounds like a lot. But when you break it into weeks, the number shrinks dramatically.

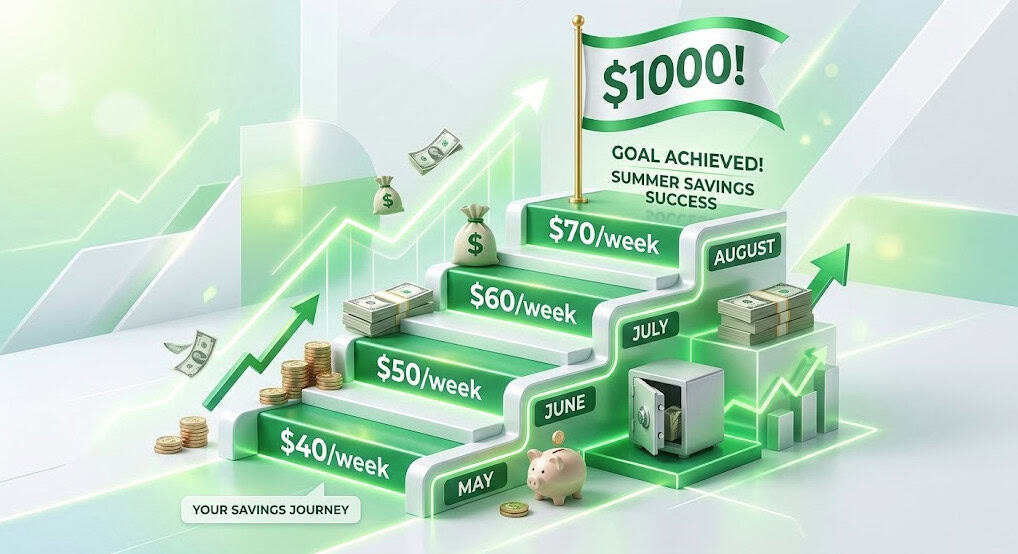

From May 1st to September 1st is approximately 18 weeks. To save $1000 in 18 weeks, you need to save approximately $56 per week. That is $8 per day. Eight dollars. That is the cost of one fast food lunch, one fancy coffee drink, one impulse buy at Target, one Uber ride you could have walked instead.

But here is where the challenge gets interesting. You do not need to save the same amount every week. Some weeks you will save $20 because it is a tight week. Other weeks you will save $100 because you found something to sell, picked up extra hours, or just had fewer expenses. The weekly targets I am about to give you account for this natural fluctuation.

The plan is designed so that early weeks have lower targets (building the habit) and later weeks have slightly higher targets (riding the momentum). You start easy and build confidence. By the time the bigger savings weeks arrive, you are already in the groove and the challenge feels natural rather than forced.

That progression feels manageable because you never jump from easy to hard overnight. You ramp up gradually, and by the time you are saving $65 to $70 per week, you have already built the skills and habits that make those numbers feel normal.

Week-by-Week Summer Savings Plan

Weeks 1-2: The Foundation (Save $80)

Your first two weeks are about building the system, not pushing yourself to the limit. Open a separate savings account if you do not have one — a free online savings account at an institution like Ally, Marcus, or Capital One works perfectly. The key is that this account should be separate from your checking account so you cannot accidentally spend the money. Transfer your weekly savings into this account every Friday like clockwork.

During these first two weeks, focus on one thing: identifying your “leak” spending. These are the small daily purchases you make on autopilot that drain money without delivering real value. For most people, the biggest leaks are daily coffee shop visits, lunch bought at work instead of packed from home, impulse Amazon orders, and convenience store snacks.

You do not need to eliminate all leak spending. Just redirect some of it. If you normally spend $6 on a coffee shop drink every morning, make coffee at home three days this week and buy from the shop twice. That single change saves you $18 in week one. Combine that with packing lunch two days instead of buying ($12 to $15 saved), and you have already hit your $40 weekly target without any dramatic lifestyle changes.

Weeks 3-4: The Pantry Challenge (Save $80)

These two weeks introduce the Pantry Challenge — one of the most effective short-term money saving strategies that exists. The concept is simple: before you buy any groceries this week, eat what you already have in your pantry, freezer, and refrigerator.

Most families have $50 to $100 worth of forgotten food sitting in their kitchen at any given time. The bag of rice in the back of the pantry. The frozen chicken breasts behind the ice cream. The canned goods you bought months ago and never used. The pasta, the beans, the frozen vegetables, the condiments, the spices. There is more food in your kitchen than you realize.

For two weeks, challenge yourself to only buy fresh essentials — milk, eggs, bread, fresh produce — and build every other meal from what you already own. Google “pantry meal recipes” with whatever ingredients you have and you will find dozens of ideas. The meals will not be gourmet, but they will be free.

A typical family saves $60 to $120 during a two-week pantry challenge. That money goes straight into your summer savings account. You are eating food you already paid for, reducing food waste, and cleaning out your kitchen all at the same time. It is the rare money-saving strategy that makes your kitchen look better while making your bank account look better.

Weeks 5-8: The Subscription Audit and Selling Sprint (Save $200)

June is when the challenge starts to feel real. Your weekly target bumps to $50, and to hit it consistently, you need to do two things this month: cut recurring costs and generate some quick cash from things you already own.

The Subscription Audit: Sit down with your bank statement and list every recurring monthly charge. Streaming services, app subscriptions, gym memberships, subscription boxes, cloud storage, premium accounts, and any other auto-renewing charges. Most people discover they are paying for six to twelve subscriptions totaling $80 to $200 per month, and actively using only half of them.

Cancel everything you have not used in the past 30 days. Be ruthless. You can always resubscribe later if you genuinely miss it. Most people cancel three to five subscriptions and never notice they are gone. That is $30 to $75 per month back in your pocket — money that was draining silently every single month.

The Selling Sprint: Spend one Saturday doing a “sell sprint.” Walk through every room in your house and pull out anything you no longer use, need, or love. Old electronics, clothes that do not fit, books you have read, kitchen gadgets collecting dust, kids’ toys they have outgrown, exercise equipment that became a clothes rack.

List everything on Facebook Marketplace, and the items that do not sell within a week, list on OfferUp or take to a consignment shop. Most people generate $100 to $300 from a single sell sprint without losing a single item they actually wanted to keep.

Between cancelled subscriptions and selling unused items, June’s $200 target becomes very achievable. Many people actually exceed it.

Weeks 9-12: The No-Spend Weekends (Save $240)

July is the month where spending temptation peaks. It is hot, the kids are restless, and every weekend presents an opportunity to spend money on entertainment, eating out, activities, and impulse purchases. This is where most summer savings plans die.

The antidote is the No-Spend Weekend. Pick two weekends in July (not all four — that is too aggressive and leads to burnout) and commit to spending absolutely zero dollars from Friday evening to Sunday night.

Before you panic, let me tell you what a no-spend weekend actually looks like in practice. Friday night is a movie at home with popcorn made from kernels and drinks from the fridge. Saturday morning is breakfast at home, then a free activity — a hike, a park, a bike ride, a trip to the library, a community event, a beach day with a packed cooler. Saturday evening is a home-cooked dinner, board games, or a backyard bonfire. Sunday is more of the same — free outdoor time, cooking at home, family projects, relaxation.

The average American family spends $200 to $400 per weekend on dining out, entertainment, shopping, and activities. A no-spend weekend saves $100 to $200 in a single 48-hour period. Two no-spend weekends in July saves $200 to $400 — more than enough to hit your July target of $240 with room to spare.

The secret is planning. A no-spend weekend without a plan feels like punishment. A no-spend weekend with a list of free activities, a stocked pantry, and a positive attitude feels like an adventure. Plan it like you would plan a paid outing — with intention and excitement.

Weeks 13-16: The Utility Reduction Month (Save $260)

August is when you attack your biggest monthly expense after rent or mortgage — utilities. Summer electricity bills are often the highest of the year because air conditioning runs constantly. But there are several adjustments that can reduce your August electric bill by 15 to 30 percent without making your home uncomfortable.

Raise your thermostat by two to three degrees. Going from 72 to 75 degrees saves approximately 6 to 9 percent on cooling costs. You will adjust to the slightly warmer temperature within two days, and the savings show up immediately on your next bill.

Use ceiling fans in every occupied room. Fans create a wind-chill effect that makes 75 degrees feel like 72 degrees. They cost about one cent per hour to run, compared to air conditioning which costs 30 to 50 cents per hour. Run fans in the rooms you are using and turn off the AC in rooms you are not.

Close blinds and curtains during peak sun hours. Direct sunlight through windows can raise a room’s temperature by 10 to 15 degrees. Closing blinds from 10 AM to 4 PM on sun-facing windows dramatically reduces how hard your AC has to work.

Switch to LED bulbs if you have not already. LED bulbs use 75 percent less energy than traditional bulbs and produce less heat, which means your AC does less work cooling the heat that light bulbs generate.

These four changes alone can save $30 to $80 on your August electricity bill. Combined with your weekly savings habits that are now firmly established, hitting the $260 target for August is well within reach.

Weeks 17-18: The Final Sprint (Save $140)

You are so close. Two weeks left. $140 to go. By this point in the challenge, you have built genuine savings habits. You are cooking more at home. You have cancelled subscriptions you do not use. You are aware of your spending in a way you were not four months ago.

The final sprint is about finding every last dollar. Look for one-time savings opportunities. Return any items you bought recently that you do not really need — most stores accept returns within 30 to 90 days. Check for any rebates or cashback you have not claimed. Look for forgotten gift cards in drawers or on apps. Check your state’s unclaimed property website — millions of dollars in unclaimed refunds, deposits, and payments sit in government databases waiting for their owners to claim them.

Also look for one more thing to sell. There is always one more item. That power tool you borrowed the neighbor’s instead. That coat you did not wear all winter. That piece of furniture you have been meaning to replace. One item sold for $50 to $100 closes the gap between where you are and $1000.

On September 1st, open your savings account and look at the number. You earned that. Not through luck. Not through a windfall. Through eighteen weeks of small, consistent, intentional choices that compounded into something significant.

Here are twenty additional ways to find extra dollars throughout the summer. Each one is small on its own, but combined, they add up to hundreds of saved dollars over the season.

At home: Make cold brew coffee instead of buying iced drinks ($4-6 saved daily). Run the dishwasher only when completely full ($15-20 saved monthly). Air-dry clothes on a line instead of using the dryer ($25-40 saved monthly). Use a programmable thermostat to raise the temperature when nobody is home ($20-30 saved monthly).

Food and drinks: Bring a cooler of drinks and snacks to every outdoor activity instead of buying on-site ($10-30 saved per outing). Grill at home instead of eating out — a full BBQ dinner for a family of four costs $12 to $15 versus $50 to $70 at a restaurant. Buy produce at farmers markets late in the day when vendors discount remaining stock. Freeze seasonal fruit when it is cheap in summer to avoid expensive winter prices.

Entertainment: Use your local library for free books, movies, museum passes, and summer programs. Check local event calendars for free outdoor concerts, movie screenings, festivals, and community events. Swim at public pools instead of water parks. Explore free hiking trails, beaches, and parks instead of paid attractions.

Shopping: Implement a 48-hour rule — wait 48 hours before any non-essential purchase over $20. If you still want it after two days, buy it. If you forgot about it, you saved that money. Buy summer clothes at end-of-season sales in August and September at 50 to 70 percent off. Use cashback apps like Ibotta and Fetch on groceries you already buy.

How to Track Your Progress Without Losing Motivation

Tracking is what separates people who finish the challenge from people who quietly abandon it in week four. You need a system that takes less than one minute per day and gives you a visual representation of your progress.

Option 1: The Savings Thermometer. Draw or print a large thermometer with markings from $0 to $1000 in $50 increments. Tape it to your refrigerator or bathroom mirror. Every time you add money to your savings account, color in the thermometer to the new level. Watching the red line climb week after week is surprisingly motivating — it turns an abstract number into a physical, visible achievement.

Option 2: The Weekly Check-In Spreadsheet. Create a simple spreadsheet or use a notebook with columns for the week number, your target amount, your actual savings that week, your running total, and how much remains until $1000. Update it every Friday night. Seeing the “remaining” column shrink from $1000 to $800 to $600 to $400 creates momentum that pushes you forward.

Option 3: A Savings App. Apps like Qapital, Digit, or even a simple note in your phone’s notes app work well for digital trackers. Some apps let you set a goal amount and deadline, then show you a progress bar that fills up as you add money. The visual progress bar is addictive in the best way.

Whatever system you choose, the key is consistency. Check in weekly. Celebrate every milestone — $250, $500, $750 — because celebrating progress reinforces the behavior that created it.

What to Do With Your $1000

You earned it. Now protect it. Here are the smartest things to do with your $1000 summer savings.

If you have no emergency fund: Keep the entire $1000 as the start of your emergency fund. Life’s unexpected expenses — car repair, medical bill, appliance breakdown — are the number one reason people go into debt. A $1000 emergency fund stops that cycle before it starts.

If you have high-interest debt: Use the $1000 to make an extra payment on your highest-interest credit card or loan. A $1000 extra payment on a credit card with 22 percent APR saves you $220 in interest over the next year. That is money that would have gone to the bank that now stays in your pocket.

If you have an emergency fund and no high-interest debt: Invest it. Put the $1000 into a Roth IRA or a brokerage account in a low-cost index fund. At an average market return of 8 percent per year, that $1000 becomes approximately $2,160 in ten years, $4,660 in twenty years, and over $10,000 in thirty years. One summer of intentional savings, growing for decades.

If you want to repeat the challenge: Keep $500 as savings and use $500 to reward yourself. You earned a reward. A weekend trip, a nice dinner, a piece of clothing you have been wanting, an experience you have been putting off. Rewarding yourself after completing a financial challenge reinforces the positive association with saving and makes you more likely to do it again.

Frequently Asked Questions

What if I can’t save $56 every single week?

That is completely normal and expected. Some weeks you will save more, some weeks less. The weekly targets in this plan are averages, not minimums. If you save $30 one week and $80 the next, you are still on track. What matters is the total at the end of each month, not the exact amount each week.

Can I start this challenge mid-summer?

Absolutely. If you start in June instead of May, you have 14 weeks to save $1000, which means approximately $72 per week. Starting in July gives you 10 weeks at $100 per week, which is more aggressive but doable if you combine multiple strategies. The plan adapts to whenever you begin.

Where should I keep my summer savings?

A separate high-yield savings account is ideal because it earns interest while keeping the money accessible but not too easy to spend. Do not keep it in your checking account — the temptation to spend it is too high when it is mixed with your regular money.

What if an emergency comes up and I need to use my savings?

Use it. That is exactly what savings are for. If a genuine emergency happens and you need $300 from your summer savings, take it without guilt. Then adjust your remaining weekly targets to still hit $1000 by September, or adjust your goal to whatever is realistic given the setback.

Should I tell my family about the challenge?

Yes, if they live with you. A savings challenge works best when everyone in the household is aware and contributing. Kids can participate by suggesting free activities. Partners can coordinate on meal planning and spending decisions. Making it a family challenge creates accountability and shared purpose.

How is this different from just budgeting?

A savings challenge has a specific target and deadline that creates urgency. Budgeting tells you where money should go. A challenge tells you how much money to save by when. They work best together — budget your expenses and challenge yourself to save the difference. The combination is more powerful than either strategy alone.

Your $1000 Summer Starts Now

Every big financial win starts with a single small decision. Today, your small decision is this: open a savings account (or designate an existing one), transfer your first $8 into it, and write down “Summer Savings Challenge — $1000 by September” somewhere you will see it every day.

That is it. That is the entire first step. Eight dollars and a written commitment. Tomorrow, you save another $8. And the day after that. And by the time your neighbors are complaining about how summer flew by and their wallets are empty, you will be looking at a savings account with four digits and knowing — truly knowing — that you built that with your own discipline and intention.

Summer is coming. Make it the one you remember as the season everything changed.

Ready to take the challenge? Pin this plan and share it with a friend who wants to save this summer. Visit SaveSmartLive.com for more saving strategies, budget plans, and money challenges.

Related articles:

How to Create a Monthly Budget That Actually Works